U.S. October ADP Nonfarm: For U.S. Stocks, Employment Data Should Be Read in Reverse

1. Introduction

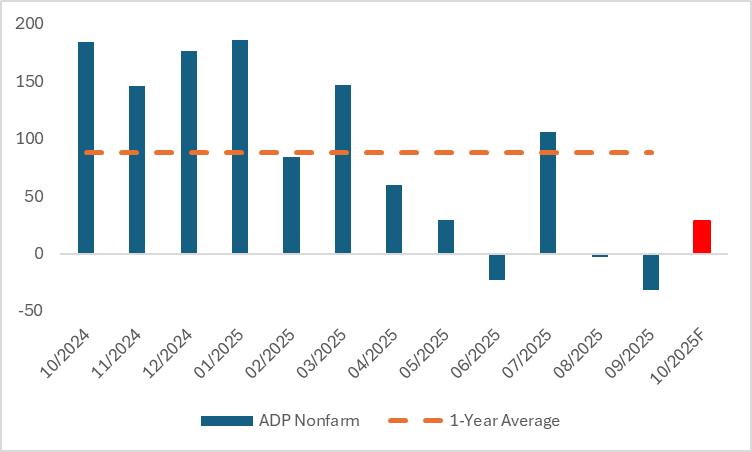

Due to the U.S. government shutdown delaying the release of the nonfarm payrolls report, the ADP employment data—commonly known as the “small nonfarm”—set for release on 5 November may emerge as the key indicator shaping the near-term direction of U.S. stocks. Consensus forecasts October ADP nonfarm payrolls at 28,000 (Figure 1), which, if met, would mark the first positive reading after negative prints in August and September. Even at that level, however, the figure would remain far below the 12-month average of 88,000, underscoring that the U.S. labour market is still cooling.

U.S. stocks are currently in a classic rate-cut trade, with the magnitude and pace of Federal Reserve easing directly determining their path ahead. At last week’s policy meeting, Chair Powell struck a hawkish tone, pushing the implied probability of a December rate cut from 90% down to around 60%. Looking forward, the October ADP report—due 5 November—stands as the near-term pivotal data point for Fed policy, but it must be interpreted inversely: a weaker-than-expected print would bolster the case for continued easing and act as a tailwind for equities; a stronger-than-expected reading could prompt the Fed to slow the cutting cycle, sparking volatility in stocks. In our view, the underlying softness in the U.S. labour market is unlikely to reverse soon, raising the odds of sustained Fed easing and leaving room for further equity upside.

From an investment strategy perspective, passive investors can allocate to broad-market ETFs such as SPY or QQQ, while active investors may target leading stocks in technology, real estate, and precious metals—including Nvidia (NVDA) and Microsoft (MSFT) in tech, homebuilder Lennar (LEN) and warehouse REIT leader Prologis (PLD) in real estate, and gold mining giant Newmont (NEM) in precious metals.

Figure 1: U.S. ADP Nonfarm (000)

Source: Refinitiv, TradingKey

2. Labour Market Weakness Fuels Ongoing Fed Rate Cuts

The softness in the U.S. labour market has become the primary driver of Federal Reserve easing because employment is deeply intertwined with the Fed’s dual mandate and the broader economic cycle. The analysis below examines this dynamic through policy objectives, economic logic, and empirical data.

First, labour market weakness directly threatens the Fed’s core mandates. The Federal Reserve is statutorily tasked with balancing price stability and maximum employment. When the jobs market cools markedly, policy tilts toward employment support. Fed officials have explicitly stated that labour weakness is the top consideration in current policy formulation—a stance that underscores employment’s primacy in the monetary framework. This priority is reinforced by September CPI coming in at 3.0%, below the expected 3.1%, giving policymakers ample room to continue cutting rates to counter downside risks to employment.

Second, labour market weakness undermines the foundation of economic growth. U.S. consumer spending accounts for more than two-thirds of GDP, and employment is the bedrock of consumer purchasing power. Even if October ADP payrolls meet consensus expectations, the print would still fall far below the 12-month average. This softness transmits through income expectations to the consumption channel, creating a self-reinforcing contractionary loop.

Finally, rate cuts serve as an effective hedge against labour market deterioration. Lower interest rates reduce corporate borrowing costs, incentivising hiring and investment, while easing household debt burdens and bolstering consumer demand. The Fed’s 25-basis-point cuts in September and October 2025 were grounded in a preventive support rationale—using monetary accommodation to arrest the downward momentum in employment and prevent the labour market from sliding from softness into a crash. Though this carries the risk of reinflation, policymakers have concluded that downside employment risks now outweigh sticky inflation pressures, forming the core justification for continued easing.

3. Rate Cuts Provide a Clear Boost to U.S. Equities

The bullish impact of Fed easing on broad stock indices flows through four key channels. First, lower funding costs directly benefit corporates: reduced borrowing rates cut interest expenses and free up capital for R&D, M&A, and share buybacks, all of which enhance earnings outlooks. Second, the discount rate falls in tandem with yields, markedly lifting the present value of future cash flows—especially for growth stocks—and drawing capital into equities.

Third, declining yields on bonds and other fixed-income assets push capital out of low-risk markets and into equities; historical data show that U.S. stocks typically see substantial inflows after rate cuts. Finally, preventive easing sends a strong policy backstop signal, boosting investor confidence, compressing risk premiums, and lifting the valuation ceiling—evidenced by the S&P 500’s positive returns following all three preventive cutting cycles since 1995.

4. Favoured Sectors and Stocks

During a Fed easing cycle, technology, real estate, and precious metals stand out as the primary beneficiaries among U.S. equity sectors. Technology is the most sensitive to liquidity conditions: Nvidia (NVDA), with its dominant position in AI chips, sees its valuation premium expand markedly in a low-rate environment; Microsoft (MSFT) benefits from accelerating cloud investment and lower financing costs, driving a clear dual tailwind to earnings and multiples.

Real estate enjoys a dual boost from resurgent demand and cheaper financing: homebuilder Lennar (LEN) stands to gain from falling mortgage rates that lift order volumes, while warehouse REIT leader Prologis (PLD) eases expansion costs and draws income-focused capital with its stable dividends. Precious metals benefit from a weaker dollar and lower real yields, with gold mining giant Newmont (NEM) directly capturing rising gold prices and offering standout defensive qualities.

5. Conclusion

In summary, the October ADP Nonfarm Employment Data released on 5 November requires an inverse interpretation: if the data is lower than expected, it will support the Federal Reserve in continuing interest rate cuts and be beneficial to U.S. stocks; if the data exceeds expectations, the Fed may slow down the pace of rate cuts, which could trigger volatility in the U.S. stock market. We believe that the weakening trend of the U.S. job market is difficult to reverse in the short term, the probability of the Fed maintaining consecutive interest rate cuts may increase, and U.S. stocks still have upside potential.

From an investment strategy perspective, passive investors can choose ETFs such as SPY and QQQ for investment. Active investors, on the other hand, can allocate to leading listed stocks in the technology, real estate, and precious metals sectors. Specific examples include NVIDIA (NVDA) and Microsoft (MSFT) in the technology sector; Lennar (LEN), a residential builder, and Prologis (PLD), a leader in warehouse REITs, in the real estate sector; and Newmont (NEM), a leading gold mining company, in the precious metals sector.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.