[IN-DEPTH ANALYSIS] Riding the Wave: How Medtronic Capitalizes on the Aging Population

Source: TradingKey

Source: TradingKey

Investment Thesis

TradingKey - Against the backdrop of the global aging trend and the continuous rise in the incidence of chronic diseases, Medtronic's product portfolio precisely meets the growing demand for diagnosis and treatment. Relying on its global supply chain network and years of accumulated technological advantages, the company has firmly held the leading position in the medical device industry. Currently, Medtronic is laying the foundation for achieving a higher valuation by focusing on high-margin businesses and optimizing resource allocation to drive earnings per share (EPS) growth. This strategic transformation injects new impetus into the company's long-term development. Despite certain challenges in the macro environment and within the company, we remain optimistic about Medtronic's long-term prospects based on its core competitiveness and market value.

What Drives the Growth of the Medical Equipment Industry

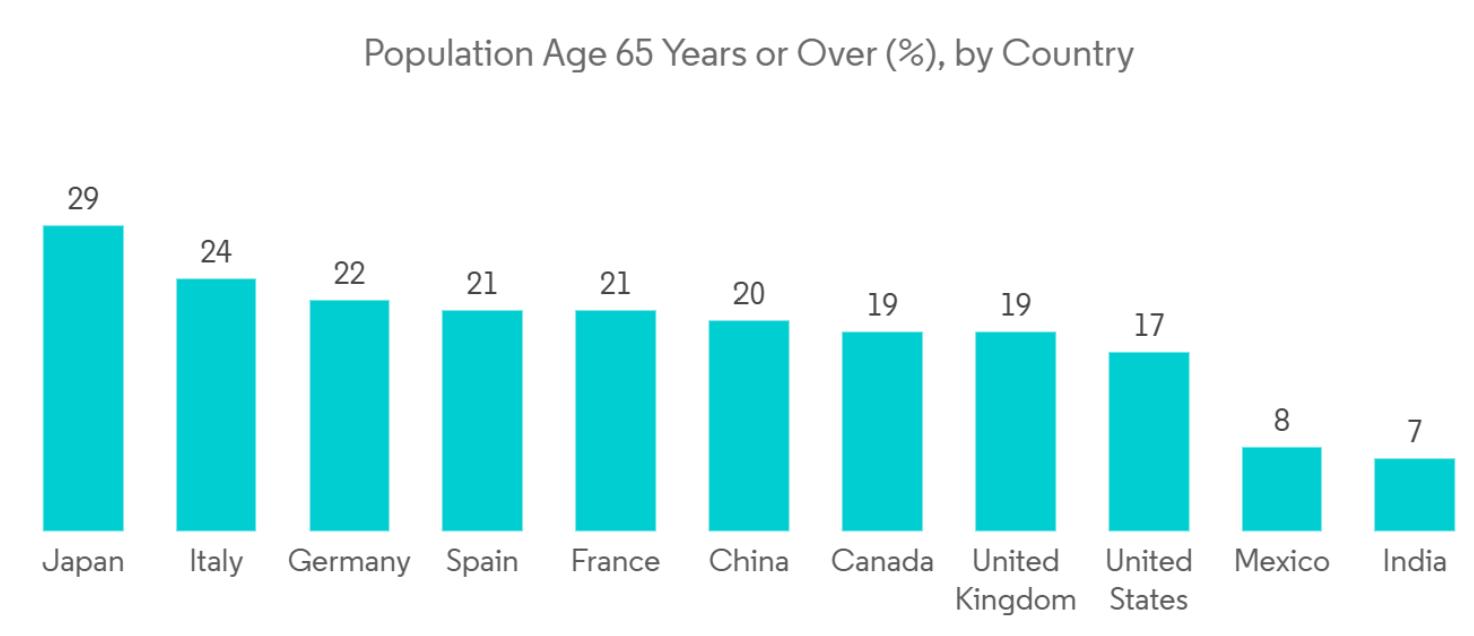

We need to admit that the increase in the aging population and the rise in the number of patients with acute and chronic diseases (such as diabetes, cancer, etc.) caused by unhealthy lifestyles such as obesity, prolonged sitting, smoking, and unhealthy diet have led to a growing demand for diagnosis and surgery. If we take diabetes as an example, according to the data provided by the National Center for Biotechnology Information (NCBI) of the United States in August 2023, approximately 422 million people worldwide have been diagnosed with diabetes, the majority of whom live in low - and middle-income countries. Each year, 1.5 million deaths are directly attributed to diabetes. I believe this figure is even higher now. In addition, the growth trend of the aging population is also obvious to all. According to the World Social Report 2023, the global population aged 65 and above is expected to double, increasing from 761 million in 2021 to 1.6 billion in 2050, among which the growth rate of the population aged 80 and above is even faster. Therefore, as the global demand for diagnosis and treatment increases, it will drive the demand for products, including capital equipment and consumables, and further support the growth of the global medical equipment market.

Source: Population Division of the Department of Economic and Social Affairs of the United Nations Secretariat, World Population Prospects: The 2006 Revision and World Urbanization Prospects: The 2005 Revision

Overview of the Medical Equipment Industry

According to the data of 2024, the global medical equipment market size reached 542.21 billion US dollars, among which North America dominated with a market share of 38.17% (approximately 188.68 billion US dollars). Looking ahead, the global medical equipment market is expected to grow steadily from 572.31 billion US dollars in 2025, at a compound annual growth rate (CAGR) of 6.5%, reaching 886.68 billion US dollars by 2032. The North American market will continue to lead and is expected to grow at a CAGR of 6.8% starting from 199.04 billion US dollars in 2025, reaching 314.96 billion US dollars by 2032.

Source: Fortunebusinessinsights

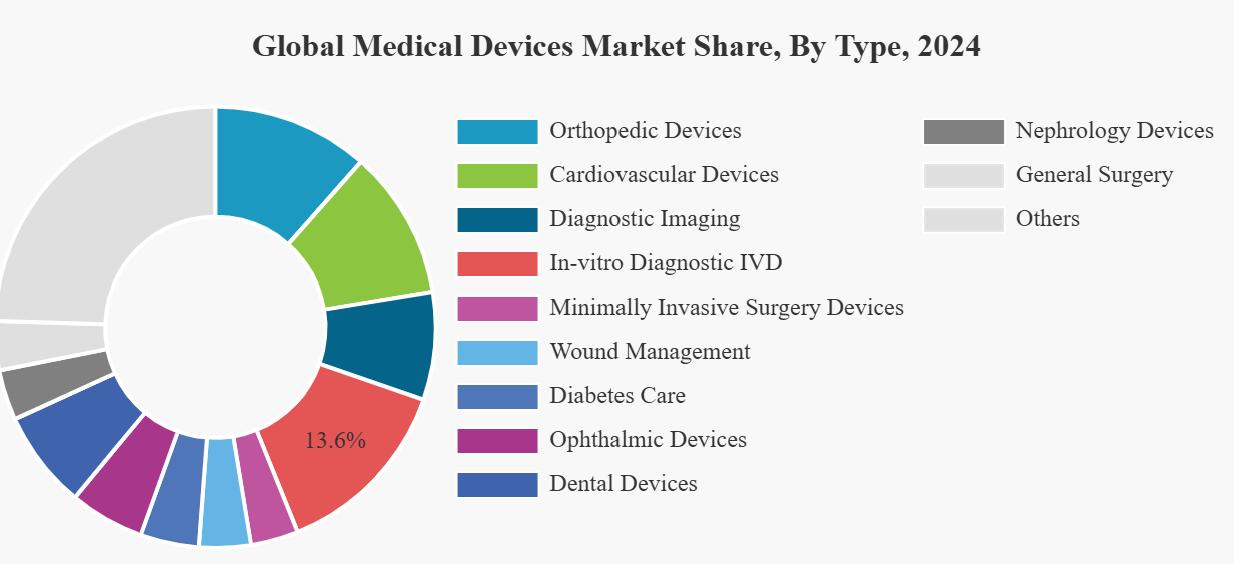

There are various types of medical devices. According to the definition of the FDA, they can be further classified into orthopedic devices, cardiovascular devices, diagnostic imaging devices, in vitro diagnostic devices, minimally invasive surgical devices, wound care devices, diabetes care devices, ophthalmic devices, nephrology devices, dental devices, general surgery devices, drug delivery devices, respiratory devices, and others. Doesn't it sound a little complicated? Don't worry. Let me simplify it for you to understand more easily.

Source: Fortunebusinessinsights

From the perspective of the definition of medical equipment, it refers to instruments and devices used for disease prevention, diagnosis and treatment. Imagine a complete patient treatment process: First, determine the type of disease through diagnostic equipment; Then, intervention treatment for the disease is carried out using therapeutic or surgical equipment; After the treatment, the recovery progress of the patients was tracked with the help of monitoring equipment. Finally, use health management equipment to prevent the recurrence of diseases. This process forms a closed loop. Therefore, medical devices can usually be simply classified into the following five categories:

· Diagnostic equipment: This includes all devices used for detecting diseases and health conditions, such as in vitro diagnostic (IVD) and imaging equipment.

· Therapeutic and surgical equipment: It covers equipment used for treating diseases and performing surgeries, including cardiovascular equipment, orthopedic equipment, endoscopic equipment and surgical instruments.

· Monitoring and support equipment: Equipment used for continuous or regular monitoring of patients' health conditions, including patient monitoring equipment, diabetes management equipment and respiratory equipment.

· Consumer and home health devices: Devices for personal use at home or for daily health care, such as blood pressure monitors, thermometers and fitness trackers.

· Advanced and specialized equipment: This includes cutting-edge technologies and equipment for specific fields, such as surgical robots, AI-driven diagnostic tools, and genetic testing devices.

Among them, the market size of therapeutic and surgical equipment currently ranks first in the medical equipment industry, covering multiple key fields such as cardiovascular, orthopedic, and general surgery. It has a wide range of applications and stable demand. Although the consumer and home health device market is currently relatively small in scale, it is expected to have the fastest growth rate among the five categories in the future, benefits to technological progress, the enhanced awareness of health management among consumers, and the increasing demand for telemedicine. The compound annual growth rate (CAGR) over the next five years is projected to reach high double digits. Under the current development trend of the medical equipment industry, Medtronic, the industry leader, undoubtedly attracts much attention. Whether in terms of product coverage or market layout, it demonstrates Medtronic's forward-looking strategic vision.

Who is Medtronic?

Medtronic is a world-leading medical technology company, founded in 1949. The company's products can meet a wide range of healthcare needs, covering key areas such as cardiovascular, neuroscience, surgery and diabetes. Its business covers more than 150 countries and has over 95,000 employees. It is one of the largest medical device companies in the world.

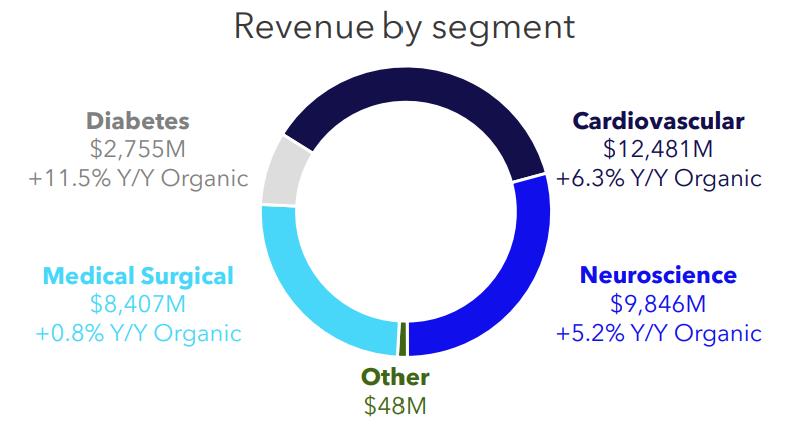

Medtronic's products mainly fall into the category of therapeutic and surgical devices, directly benefiting from the growth trends of chronic diseases and an aging population. Its revenue mainly comes from four core products: cardiovascular products, neuroscience products, medical surgical products and diabetes products, closely following the core development needs of the market in the future.

Source: Medtronic

· Cardiovascular products: The products mainly include pacemakers (to help the heart keep beating normally), defibrillators (to correct abnormal heart rhythms), artificial heart valves (to replace damaged valves), vascular stents and balloons (to unblock blocked blood vessels), which are used for the diagnosis, treatment and management of cardiovascular diseases such as heart rhythm disorders, heart failure and coronary heart disease. In fiscal year 2025, the revenue from this part of the business grew organically by more than 6% to 12.5 US billion dollars, making it Medtronic's largest source of income, accounting for more than 37%.

· Neuroscience products: The products mainly include those related to the brain and spine, covering spinal surgical implants (such as screws and stents for spinal repair), brain stimulators, and vascular catheters for treating stroke. They help treat chronic pain, Parkinson's disease, epilepsy, spinal injuries or stroke, etc., enabling patients to regain mobility or alleviate the symptoms of related diseases. This part of the products is more often used in complex surgeries and is also Medtronic's second-largest source of revenue (accounting for 29.2%), with revenue reaching 9.8 billion US dollars in fiscal year 2025, representing an organic growth of over 5%.

· Medical surgical products: Mainly include surgical tools that doctors need to use when performing minimally invasive surgeries and monitoring devices for detecting patients' postoperative conditions (such as instruments for measuring heart rate and blood oxygen), basically covering most of the tool products required for minimally invasive surgeries from diagnosis to rehabilitation. This part of the revenue accounts for approximately 25%, reaching 8.4 billion US dollars in the fiscal year 2025. The organic growth is relatively slow, only 0.8%.

· Diabetes products: Medtronic's diabetes product line is rather unique. Its products mainly fall into the category of consumer and home health devices, including insulin pumps (automatically injecting insulin into diabetic patients), blood glucose monitors (real-time blood glucose level checks), and smart insulin pens (recording dosage), which help patients manage and control diabetes, automatically monitor blood glucose levels, and precisely infuse insulin. Although this product category currently accounts for less than 10% of Medtronic's total revenue, the revenue growth rate of Medtronic's diabetes products is the fastest among the four categories, benefiting from the high growth rate of consumer and home health devices in recent years. The organic revenue growth in fiscal year 2025 is close to 12%, reaching nearly 2.8 billion US dollars.

Short-term Challenges Still Exist, but the Long-term Prospects are Promising

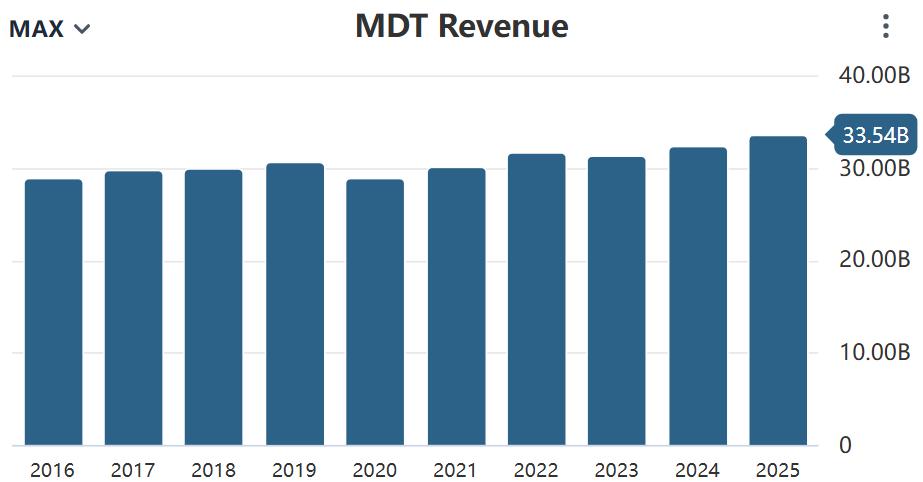

Medtronic's revenue growth has been sluggish in recent years, mainly due to industry and external factors. The pandemic has led to the postponement or cancellation of elective surgeries, and supply chain issues have further dragged down the sales of surgery-related instruments. Currently, the company is in the recovery stage. Meanwhile, specific market factors, such as China's centralized procurement policy for high-value medical consumables, which accounts for a relatively high proportion of revenue, significantly depresses prices, such as cardiac stents and orthopedic implants. Coupled with exchange rate fluctuations, this poses a headwind to its overseas revenue (accounting for half of the total revenue). In addition, the aging of the company's internal product line and the lack of innovation, especially in business segments such as surgical robots, where market share has been seized, have become one of the key reasons for the stagnation of revenue.

Source: Stockanalysis

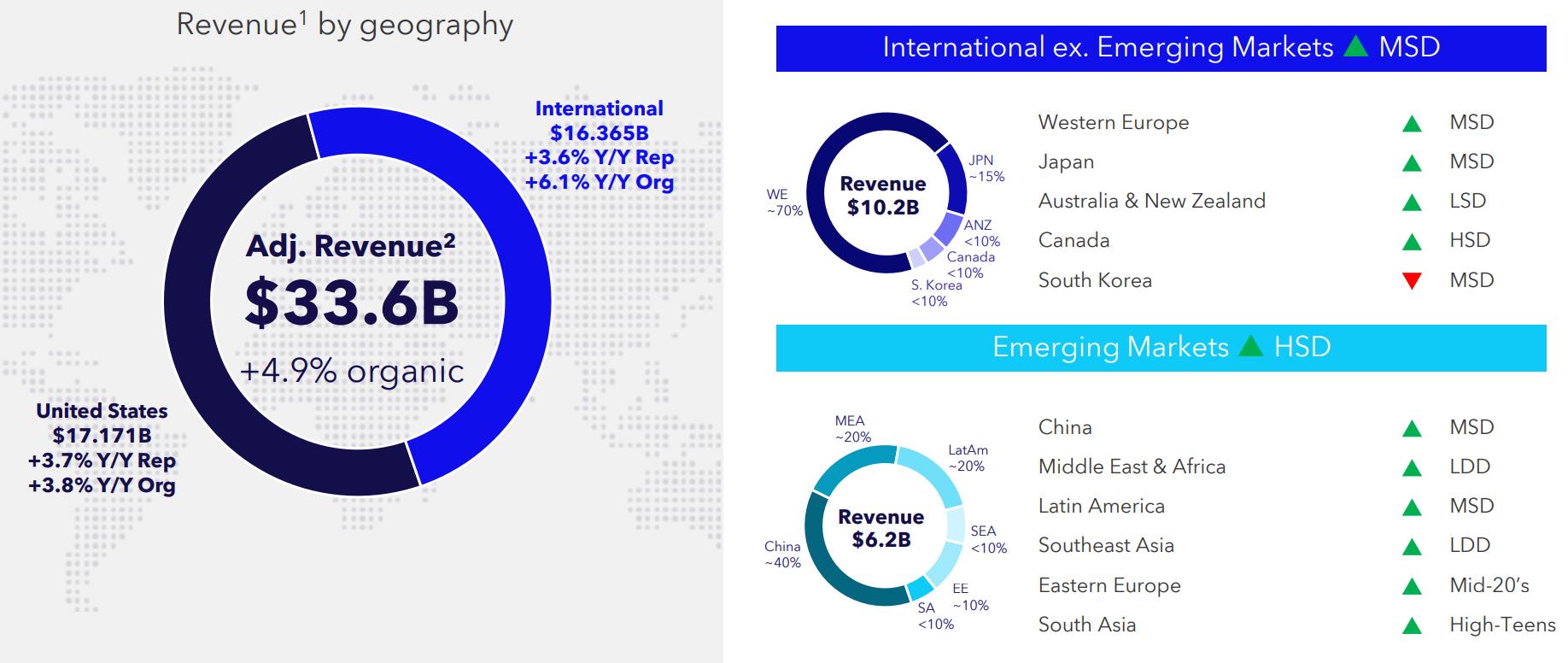

Despite facing numerous challenges in the short term, Medtronic's extensive global market presence provides a solid foundation for its long-term development. The company's products are sold to over 150 countries, and core markets such as the United States, Europe, Japan and China have all maintained stable growth. The North American market continues to hold a dominant position which benefits from its mature medical system and Medicare's generous reimbursement policy for medical devices. The European market, benefiting from stable growth in healthcare spending and well-developed infrastructure, is expected to achieve a robust compound annual growth rate (CAGR). The Asia-Pacific region shows the fastest growth potential. Especially in China, due to the rising incidence of chronic diseases such as cardiovascular diseases and diabetes, as well as the rapid expansion of medical demand, the market prospects are particularly broad.

Source: Medtronic

In the future, the global aging trend will bring significant growth opportunities to Medtronic. The United Nations predicts that by 2050, the global population aged 65 and above will reach 1.5 billion, accounting for 16% of the total population. Among them, the proportion of the elderly population in Japan, Europe, China and the United States is expected to average as high as 26.9%. Aging will drive up the prevalence of chronic diseases such as diabetes, cardiovascular diseases and cancer, thereby significantly increasing the demand for advanced medical devices in diagnosis, treatment and monitoring. Medtronic's product portfolio and global distribution network are highly consistent with this demand. If the company can accelerate innovation, optimize its product line and seize the growth opportunities in emerging markets, it is expected to achieve long-term growth in the wave of medical demand driven by aging.

Source: United Nations Population Fund

The Financial Performance

Medtronic's gross profit margin of 66% exceeds the industry average, aligning closely with Stryker (65%) and Boston Scientific (68%). However, it trails Edwards Lifesciences (80%) while surpassing Becton Dickinson (46%) and Abbott Laboratories (56%). The difference in gross profit margin mainly stems from the characteristics of the product portfolio. Medtronic focuses on fields such as cardiovascular, neuroscience, medical surgery, and diabetes. Among them, products like pacemakers and neuroregulators have high technical barriers and large added value, which support strong pricing power and high gross profit margins. In contrast, Becton Dickinson's product portfolio contains more low-value-added consumables (such as syringes and blood collection equipment), resulting in a lower gross profit margin. Edwards Lifesciences focuses on high-profit transcatheter heart valves. With economies of scale and low-cost production, it has maintained a higher gross profit margin. Although Medtronic's diversified product line has enhanced revenue stability, it has also brought about higher production and supply chain management costs.

Source: Company Reports, TradingKey

Medtronic adopts a multi-business development strategy, ensuring the stability of its revenue sources, but the operational complexity increases accordingly. Its total operating expenses accounted for 46%, which was higher than Stryker (42%) and Abbott (38%). Among them, as Medtronic's products cover more than 150 countries, the global distribution network and marketing promotion costs are relatively high, and the SG&A expenses account for 32%, which puts pressure on the operating profit margin. In contrast, Abbott's SG&A accounted for only 26%, possibly thanks to its more focused product line. In addition, Medtronic invests a large amount of R&D expenses every year to promote the development of new products and innovation in multiple fields, maintaining the richness of its product line and market competitiveness. Although R&D investment exerts certain pressure on the short-term operating profit margin, it lays the foundation for long-term sustainable revenue and competitive advantage.

How Divestiture of Diabetes Business Affects Valuation and EPS

Medtronic's diabetes business mainly targets consumers (B2C), which is significantly different from the company's core business model that targets medical institutions (B2B), resulting in the gross profit margin and operating profit margin of the diabetes business being lower than the company's overall level. This is also one of the important reasons why the market gives Medtronic a valuation lower than the industry average. Despite this, the diabetes business has achieved double-digit growth over the past six years and is Medtronic's fastest-growing revenue-generating business. With a solid product line, it has the ability to operate independently. Therefore, the management plans to divest the diabetes business in phases over the next 18 months: first, list up to 20% of the diabetes business shares, then complete the split and exchange the remaining new diabetes company shares for Medtronic shares held by shareholders willing to participate.

Source: Company Reports, TradingKey

After the split, Medtronic will streamline its business portfolio, focusing on high-margin areas such as cardiovascular and neuroscience, and reduce operational complexity. The management expects that the split will drive the gross profit margin and operating profit margin to increase by approximately 50 basis points and 100 basis points respectively, thereby significantly improving the overall profitability and is expected to enhance the valuation level. If the split is successfully completed and the market recognizes Medtronic's strategy of focusing on high-profit businesses, its valuation multiple may approach the industry average or even surpass that of its peers. Based on a 20 times price-earnings ratio (PE) valuation, it is expected that earnings per share (EPS) will increase at a high single-digit growth rate to $6.1 in fiscal year 2027, and the target share price will be approximately $122 at that time.

However, Medtronic's development is not without challenges. The spin-off of the diabetes business may be delayed or fail due to regulatory approval, market conditions or other factors. Meanwhile, intensified market competition may erode the market share of related businesses. In addition, regulatory and legal risks may also have an adverse impact on the company's operation.

Conclusion

Overall, population aging is like an irreversible wave, and Medtronic, as a "surfboard manufacturer", has accurately grasped the long-term trend of aging and the increase in chronic disease patients. With continuous technological innovation, a diversified product portfolio and a global sales network, Medtronic is able to continue to benefit from this wave. In addition, the spin-off of its diabetes business is expected to further optimize the strategic layout, focus on high-profit areas, and enhance financial performance. In the long term, if Medtronic can continue to launch innovative products and efficiently capture market opportunities through its global network, its core competitiveness will be further consolidated, providing a solid support for the increase in valuation and the growth of earnings per share (EPS).

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.