AMD Q2 FY2025 Earnings Review: Impressive Growth Stumbles on Export Control Hurdles

AMD Q2 FY2025 Earnings Review

TradingKey - Advanced Micro Devices, Inc. (NASDAQ: AMD) released its Q2 FY2025 earnings on August 5, 2025, after market close, delivering robust results driven by record sales in its Data Center and Client segments. Despite a 32% YoY revenue increase, surpassing expectations, the stock dipped around 6% in aftermarket, reflecting investor concerns over export control impacts and decline in gross margin. The results highlight AMD’s strong positioning in AI and high-performance computing, tempered by regulatory headwinds affecting its Instinct GPU sales to China.

Source: TradingKey

Key Financial Results

Metric | Q2 FY2025 | Q2 FY2024 | Beat/Miss | Change |

Revenue | $7.69B | $5.84B | Beat | +32% |

Adjusted EPS | $0.48 | $0.69 | Meet | -30% |

Non-GAAP Gross Margin | 43% | 53% | Miss | -10pp |

Non-GAAP Operating Income | $897M | $1.26B | N/A | -29% |

Data Center Revenue | $3.2B | $2.83B | Miss | +14% |

Client & Gaming Revenue | $3.6B | $2.14B | Beat | +69% |

Embedded Revenue | $824M | $861M | N/A | -4% |

Free Cash Flow | $1.2B | $439M | N/A | +173% |

Source: AMD, TradingKey

Guidance & Conference Call

Q3 2025 Guidance: AMD expects Q3 revenue to be around $8.7 billion (±$300 million), up 28% YoY and 13% sequentially. Non-GAAP gross margin is projected near 54%, rebounding from Q2’s export-control-related inventory charges. Operating expenses are forecasted at $2.55 billion, with a non-GAAP tax rate of around 13%. Guidance excludes revenue from Instinct MI308 shipments to China due to ongoing U.S. export license reviews.

Data Center Segment: Q2 revenue grew 14% YoY to $3.24 billion, led by record EPYC CPU sales. However, shipments of MI308 GPUs to China were blocked by U.S. export restrictions, resulting in an $800 million inventory write-down and reducing the overall non-GAAP gross margin to 43% (54% excluding the charge). CEO Lisa Su highlighted sustained EPYC market share gains, over 100 new cloud deployments, and AI infrastructure wins with Google, Oracle, and others, showcasing the upcoming MI350 GPU ramp in H2 2025, which offers cost-efficient AI inference performance compared to Nvidia. Risks remain from write-down and ongoing export controls, with Q3 guidance conservatively excluding MI308 revenue, strong competition from Nvidia and Intel.

Client & Gaming Segment: Revenue surged 69% YoY to $3.62 billion, driven by Ryzen 9000 series CPUs and strong Gaming revenue from Radeon GPUs and console SoCs. Operating income rose sharply to $767 million, supported by a premium product mix and new launches like Threadripper 9000WX and Radeon AI PRO. Margin stability benefits from commercial PC and server growth, balancing GPU ramp costs.

Embedded Segment: Revenue declined 4% to $824 million amid mixed demand, with operating income down 20% to $275 million. Strategic projects include FPGA shipments and collaborations on robotaxi AI solutions, indicating future growth potential despite near-term softness.

AI and Strategic Investments: AMD’s AI roadmap features the MI350 GPU series (in volume since June) and the upcoming MI400/Helios platform in 2026 targeting 40 petaflops FP4 performance. The ZT Systems manufacturing unit will be sold to Sanmina for $3 billion, sharpening AMD’s focus on AI infrastructure. Partnerships for large-scale AI compute (e.g., HUMAIN’s 500 MW plan) and sovereign AI initiatives underpin AMD’s aim for “tens of billions” in AI revenue. However, 8–9-month lead times for GPUs risk supply bottlenecks. Heavy AI investment and lower-margin GPU sales may pressure margins despite efficiency gains.

Financial Position: AMD generated record free cash flow of $1.2 billion, driven by $1.46 billion operating cash flow. The company repurchased $478 million in stock and reduced debt by $950 million to $3.2 billion. Cash and short-term investments totaled $5.87 billion, down 20% mainly due to acquisitions. CFO Jean Hu emphasized disciplined capital allocation balancing AI investment and shareholder returns. The 30% decline in non-GAAP EPS largely reflects the inventory charge and increased AI-related expenses.

Conclusion

AMD’s Q2 results prove that its AI and Data Center strategy is working, despite earnings pressure from export controls. The company’s bet on MI350 GPUs and next-gen products is already driving momentum, but further upside comes down to three things: winning big AI deployments, navigating regulatory roadblocks, and showing clear improvement in margins. The pace of MI350 adoption and the timing of U.S. license decisions will directly shape near-term growth. If AMD starts to stabilize gross margins even as it scales in AI, confidence in the company’s execution and long-term vision goes up. On the other hand, persistent supply issues or slow regulatory progress could keep a lid on upside. Right now, AMD’s biggest lever is capturing demand for new AI workloads as the landscape rapidly shifts, turning product leadership into real, scalable growth.

.png)

AMD Q2 FY2025 Earnings Preview

TradingKey - Advanced Micro Devices, Inc. (NASDAQ: AMD) is scheduled to report its Q2 FY2025 earnings on Tuesday, August 5, 2025, after the U.S. market closes. The earnings call will begin at 5:00 p.m. Eastern Time.

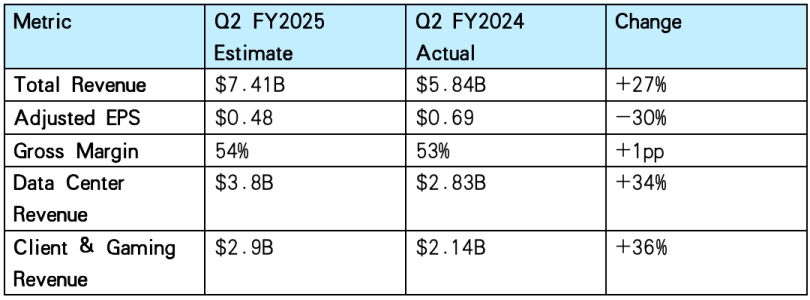

Market Forecast

Source: AMD, Seeking Alpha, TradingKey

Where Investors Should Watch

Data Center and AI Growth: AMD’s Data Center segment is expected to remain the primary engine of growth, driven by fifth-generation EPYC Turin processors and Instinct GPU accelerators. Attention should be given to updates regarding the rollout of the Instinct MI350 series and the strategic impact of the pending ZT Systems acquisition on AMD’s AI infrastructure. With hyperscalers such as AWS, Google Cloud, and Oracle scaling AI workloads, commentary on market share gains against Nvidia and potential supply chain bottlenecks for GPUs or server components will be particularly important.

Revenue Growth vs. Profitability: Revenue is forecasted to increase by approximately 27% YoY, while adjusted EPS is expected to decline. This divergence is likely due to higher investments in AI technologies, increased operating expenses, and shifts in product mix toward emerging AI accelerators like the MI355. Understanding how AMD manages the balance between growth investments and margin pressures will be key, especially in light of prior trends showing growing operating leverage alongside compressed near-term earnings.

Client & Gaming Segments: The Client and Gaming divisions, historically significant contributors, are anticipated to sustain positive revenue trends, supported by high-end Ryzen CPUs and new client products. Close observation of any signs of demand softness or weakness in these segments is warranted, as they influence AMD’s overall margin profile and business diversification.

R&D and Capital Allocation: Continued elevated spending on research, development, and strategic AI initiatives is shaping AMD’s long-term growth potential but may exert pressure on near-term margins. Guidance on how these investments are expected to translate into new products, pipeline strength, and profitability outlooks remains a critical area to monitor.

Conclusion

For AMD’s Q2 FY2025 earnings, investors should prioritize management’s guidance on Data Center growth, AI accelerator adoption, and strategies to navigate export controls. Strong Data Center performance and positive updates on MI350 series production could bolster confidence. However, risks include margin compression from the inventory charge and competitive pressures from Nvidia and Intel. Maintaining exposure into earnings is reasonable, but investors should be cautious of guidance indicating prolonged export control impacts or Data Center growth below expectations. Conversely, signals of accelerated AI partnerships or easing regulatory headwinds could support a bullish outlook, reinforcing AMD’s position in the AI and high-performance computing markets.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.