Microsoft 4Q25 Earnings Comment: Azure is Leading the Parade

TradingKey - Microsoft will release its earnings for the second quarter of the fiscal 2025 on July 30th after the market closed:

- 4Q25 Earnings per share: $3.65 vs $3.37 estimate (+24% y/y)

- 4Q25 Revenue: $76.44 vs $73.93bn estimate (+19% y/y)

The two main business lines – 1) Productivity and Business Processes and 2) Intelligent Cloud performed very well.

The Productivity and Business Processes, which represent the company’s software products, was up 16% driven by Copilot adoption improving the revenue per user, while 365 products were driven by the E3 and E5 suites. We should also note that the process of moving from on-premises to cloud subscriptions is attracting a lot of SMEs too, area which is yet to be explored by Microsoft.

The revenue growth of the Intelligent Cloud segment (Azure, Windows Server, SQL Server, GitHub) was even higher, at 26%, and within this, the Azure grew 39%. In terms of revenue, Cloud is already almost as big as the Productivity business, and Azure itself already represents 27% of the total company revenue. Of course, AI is behind this solid growth, as over 80% of the Fortune 500 companies are using Azure AI right now.

As of this quarter, Microsoft is spending a lot on capex - $30 billion vs previously estimated $20 billion. However, during the earnings call, the CFO, Amy Hood, gave indicators that the pace of capex spending will slow down in the coming fiscal 2026, which will surely be welcomed by the market.

As the stock price is up 8% after the bell, Microsoft is traded at 42x PE, a premium valuation compared to Meta or Alphabet.

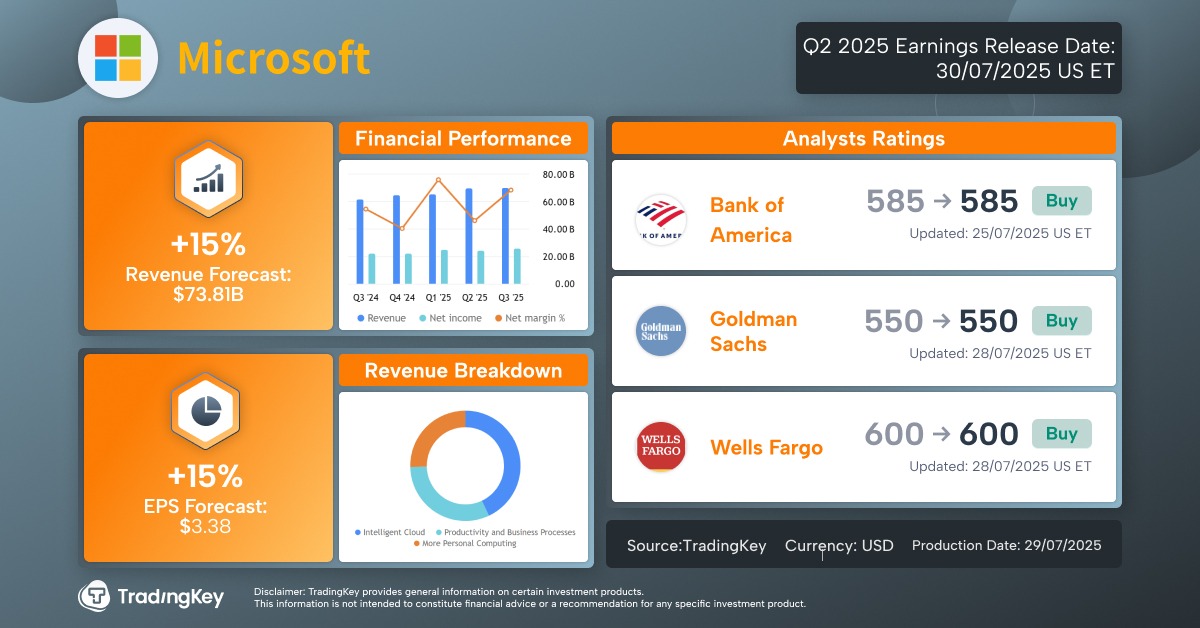

TradingKey - Microsoft will release its earnings for the fourth quarter of the fiscal 2025 on July 30th after the market closes:

- 4Q25 Earnings per share: $3.38 estimate vs. 4Q24 actual of $2.95 (+15% y/y)

- 4Q25 Revenue: $73.81bn estimate vs. 4Q24 actual of $64.38bn (+15% y/y)

Software Business: We do expect the Productivity & Business Process segment to remain resilient despite tariffs and macro slowdown with low teen top-line growth. The growth there will come mainly from increased revenue per user, driven by the increasing adoption of the current hot products of Microsoft, namely - E5 and Copilot.

Cloud Momentum: In the last few quarters Azure was able to grab market share from the other two major cloud competitors – Google and AWS. Both the AI and non-AI aspects of the cloud are in a very strong shape.

Cost Control: As one of the major AI scalers, Microsoft is spending a fortune on AI infrastructure. We already saw Alphabet revising upwards its estimates for capex for the year, and we won’t be surprised MSFT to follow. For reference, the current guidance for the quarter is expected to be close to $17.8 billion. Also, we do expect the intensified AI talent war and the infrastructure-related operational costs to limit the margin expansion, keeping it around 42%. Also, the fact that Cloud business is growing faster and it usually has lower margin than the software business, we might see further dilution of the profitability.

Competition with Grok: We can also view MSFT as a proxy to OpenAI (and ChatGPT), which is not listed. The company’s partnership with OpenAI will be in the spotlight, as we recently saw Grok and Gemini gained traction.

Conclusion

Microsoft is traded at 39x PE, a premium valuation compared to Meta or Alphabet. This combined with the high expectations regarding the business performance makes it more difficult to see a sudden surge in the share price.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.