Lilly's Secret Growth Engine Unleashed

- Lilly’s Q1 2025 revenue rose 45% YoY to $12.73B, driven by 53% volume growth and strong incretin demand.

- Zepbound commands 74% of U.S. new obesity prescriptions; Mounjaro and Zepbound together generated $6.15B quarterly.

- Gross margin reached 83.5%, while non-GAAP EPS rose 29% YoY to $3.34 despite $1.57B IPR&D charges.

- Forward non-GAAP EPS guidance of $20.78–$22.28 implies a 32x–34x valuation, with long-term optionality supporting $1,125/share.

TradingKey - In contrast with the general assumption that Eli Lilly (LLY) is priced for perfection, the Q1 2025 numbers indicate the company's stock is in the nascent stages of a strategic turning point. Its performance of an astonishing 45% year-over-year growth is not an outcome of some blockbusting instance but an indicator of a multi-pronged pipeline engine roaring in harmony. Most importantly, the runaway growth from Mounjaro and Zepbound, both part of the incretin class of drugs, presage an even deeper strategic shift: Lilly is evolving into an out-and-out platform leader in cardiometabolic and neurodegenerate care.

Institutional investors tend to discount peak hype cycles across obesity and diabetes therapeutics. However, Lilly's execution through share gain capture, pipeline diversity, and price management indicates the durability of this growth is underestimated. Meanwhile, the marketplace continues to fail to fairly value Lilly's upcoming catalysts, such as oral GLP-1 orforglipron and donanemab for Alzheimer's. The consequence is a valuation multiple on the surface that is high but being supported by under-monitization of truly vast optionality.

Lilly's story is moving beyond single-product success. The alignment of a first-mover pipeline, scale of manufacturing, and nascent platform economics presents a compelling asymmetric opportunity: not just to ride the obesity wave, but to shape the future of global chronic disease treatment.

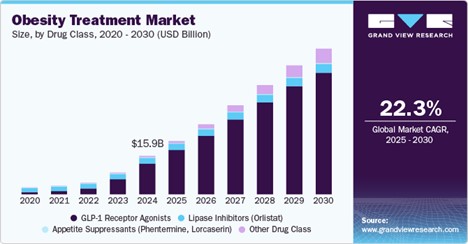

Source: GrandViewResearch

From Product to Platform: Lilly's Business Model Transformation

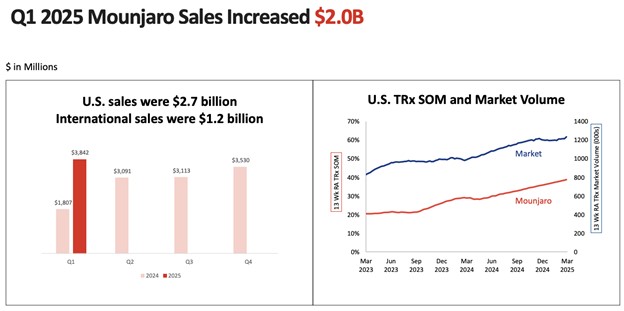

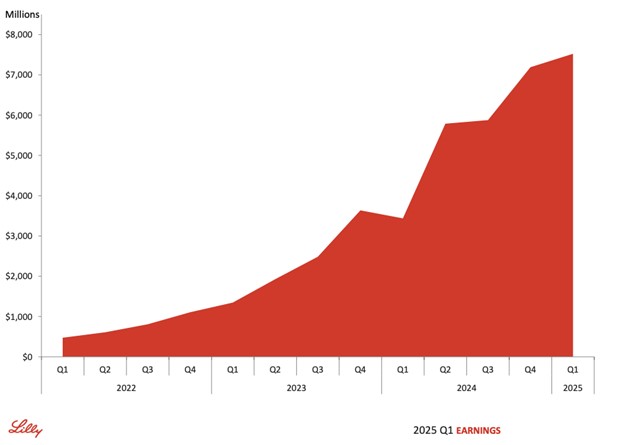

At its essence, Eli Lilly is still a pharma company. But its Q1 2025 performance testifies to a structural shift towards platform economics. The company's $12.73 billion revenue, 45% year-on-year growth, is fueled by volume growth of 53%, cushioned only partially by pricing and FX headwinds. Most importantly, U.S. volume grew 57% with Zepbound and Mounjaro accounting for lion's share of it, while international markets witnessed diversified acceleration with Jardiance and Verzenio picking up momentum.

Source: Eli Lilly and Company, Q1 2025 Earnings Call

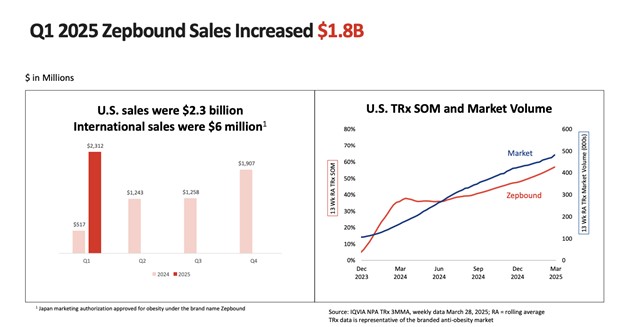

Current key drugs bring in $7.52 billion every quarter, with Mounjaro at $3.84 billion and Zepbound at $2.31 billion. These numbers point to not only demand but monetization depth. In the space for obesity, new prescriptions in the U.S. for Zepbound have a stunning 74% share. Lilly's leadership in the GLP-1 dual agonist class is no longer conjectural, it's in real-world prescriptions.

Source: Eli Lilly and Company, Q1 2025 Earnings Call

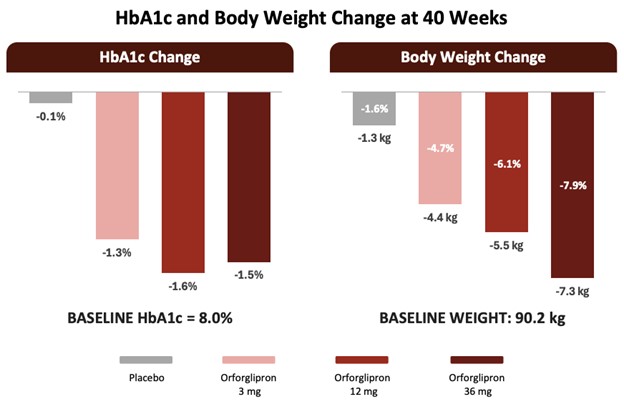

More significant is Lilly's innovation flywheel. The Phase 3 readout success of its oral small-molecule GLP-1, orforglipron, demonstrates that the company is not satisfied with leadership in injectables. Forfglipron cut 7.9% of weight and 1.6% of HbA1c and had tolerability comparable to injectables.

The pipeline growth takes Lilly closer to the defensible platform strategy of biotech blue-chips: repeat innovation, penetration of new markets, and lifecycle management in related diseases. Thus, Lilly is not longer a product-cycle-reliant pharma, it's becoming a powerhouse of a therapeutics platform.

Source: Eli Lilly and Company, Q1 2025 Earnings Call

Competitive Positioning: Something Beyond Beating Novo Nordisk

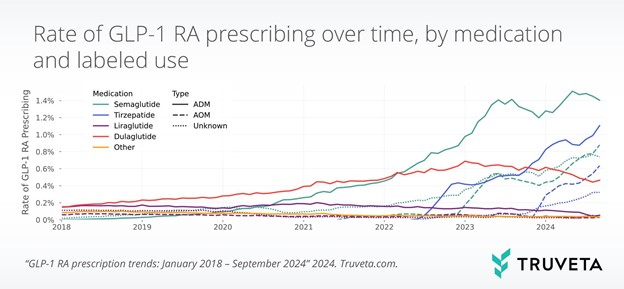

Although Novo Nordisk (NVO) continues to be Lilly's primary challenger in obesity and diabetes, competitive momentum is switching in favor of Lilly. Through the first quarter of 2025, Lilly held 53.3% of combined prescription share in the US incretin analog category at the expense of Novo's 46.1%. This leadership was fueled by the strong take-up of Zepbound, which introduced new vial sizes exclusively via LillyDirect, a vertically integrated distribution platform heightening margin and patient stickiness.

Source: Eli Lilly and Company, Q1 2025 Earnings Call

Lilly's competitive advantage is not just in product performance but in also in strategic reach. In its own channel of distribution, the company has control of patient experience, price dynamics, and real-world feedback loops. Novo Nordisk does not have this direct-to-patient advantage at scale in the U.S.

In addition, Lilly has more diversified pipeline. Novo is tied to GLP-1s while Lilly has on its road-map orforglipron (oral GLP-1), lepodisiran (Lp(a) lowering), donanemab (Alzheimer's), and pirtobrutinib (oncology). This diversification helps in less single-class dependence as pressure on prices of drugs against obesity continues to increase due to competition

In cancer, Jaypirca's EU approval for chronic lymphocytic leukemia and early traction for Kisunla place Lilly in high-margin growth in a differentiated category. In the meantime, the pipeline in Alzheimer's supported by donanemab and remternetug has the potential to become a multi-billion-dollar category. The strategic moat isn't just founded on clinical evidence, it's supported by manufacturing scale, regulatory flexibility, and life-cycle management.

Margin Mechanics and Monetization Depth: Why Growth in EPS Is Just Getting Started

Underneath Lilly's top-line revenue is an even stronger margin story. Gross margin grew to 83.5% on the non-GAAP basis in Q1 2025, rising 100 basis points year on year due to positive product mix (incretins) and manufacturing efficiency. This increase is important, it counters the dilution from price pressure and sets the stage for long-term operating leverage.

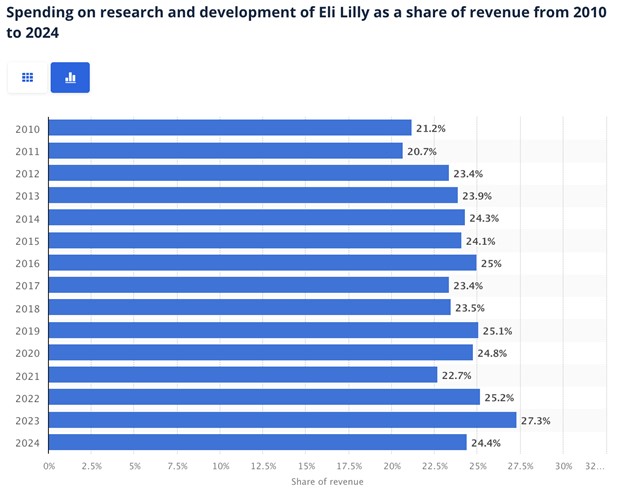

R&D expenditures grew 8% to $2.73 billion, 21.5% of revenue, as Lilly continued to reinvest in its pipeline. SG&A was 26% higher at $2.47 billion, primarily related to promotional support for new launches such as Zepbound and Omvoh. Still, Lilly was able to achieve a non-GAAP operating margin of 30.3% and performance margin (adjusted operating profit as a percentage of revenue) of 42.6%.

Source: Statista

These numbers display scalability. In spite of IPR&D fees of $1.57 billion due to the Scorpion Therapeutics deal, Lilly posted strong EPS growth. Non-GAAP EPS was 29% higher year-over-year at $3.34. This positions the full-year EPS at $20.78–$22.28, showing strong back-half leverage.

Significantly, Lilly is maintaining volume at the expense of price. Its price decreased 6% worldwide, yet volume expanded 53%. In Europe, where volume improved by 79%, FX and price dragged topline growth to 66% but margin growth remained intact. This model of volume is unusual in pharma and is becoming more akin to SaaS economics where unit compression of cost enhances sustainability of profitability.

In simple words, Lilly's profitability formula is gaining momentum, with the magnitude of future operational compounding underestimated by the markets.

Valuation Reset: A Deserved Premium with Optionality

LLY trades at a forward GAAP P/E of 35.63x and 54.88x non-GAAP P/E (TTM). These numbers are high compared to the sector median of P/E GAAP FWD of 23.82 but are reflective of a fundamentally different earnings profile. The company is forecasting full-year non-GAAP EPS of $20.78 to $22.28, which would imply a valuation range of ~32x to 34x on current levels, which is less than its premium history.

Source: Eli Lilly and Company, Q1 2025 Earnings Call

A more suitable valuation range employing scenario-based multiples commensurate with Lilly's innovation tempo and scalability yields:

- Base case (35x on $21.53 midpoint EPS): $753/share

- Bull case (40x): $861/share

- Optionality case (45x CY26 $25 EPS): $1,125

These estimates capture Lilly's leadership in incretin therapies, upside from orforglipron, Alzheimer's candidates such as donanemab, and long-term leverage of cardiometabolic and autoimmune portfolios. Double-digit revenue growth combined with 83%+ gross margins and 40%+ performance margins justify premium on execution rather than speculation despite valuation friction.

Even its enterprise value to sales ratio (FWD EV/S: 11.96) and price to cash flow (TTM: 72.75x) are high, but more supported by compounding operating income and forward visibility. The valuation is not cheap, but it's reasonable in the context of what Lilly is transforming into.

Risk Factors: Valuation Friction, Pricing Pressure, and Pipeline Execution

In spite of its run, Lilly is at risk. Number one is valuation compression. At almost 36x forward earnings, anything wrong, be it clinical failure, regulatory setback, or price reset, can trigger steep multiple compression. That vulnerability is compounding due to high hedge fund concentration and momentum flows.

Second, prices of obesity drugs come under heightened scrutiny. At more than $1,000 a month in list prices, reimbursement friction is likely to increase as demand for GLP-1s scales worldwide. The US election cycle and CMS policy reviews introduce headline risk. Also, competition from Novo Nordisk, Amgen (oral GLP-1 entrants), and Pfizer (early-stage assets) should squeeze margins in the future. Third, Lilly's pipeline is large but also complicated. Orforglipron and donanemab are still awaiting regulatory milestone moments.

Donanemab's risk-benefit profile is still being assessed by the FDA, and the success of orforglipron's launch will ride on real-world tolerability and adherence. Execution across 40+ active late-stage trials takes uncommon coordination. Investors need to watch for foreign exchange fluctuations, which trimmed 2% from Q1 topline, and ongoing IPR&D write-offs or litigation potentially negatively influencing quarterly earnings perceptions. Although Lilly's margins are strong, at such scale small cracks can get emphasized in perception.

Source: Truveta

Conclusion: Lilly’s Growth Engine Is Running Ahead of the Market

Eli Lilly is not just a high-growth pharma stock, it is creating a model for therapeutics on the same scale as leaders in biotech and technology. Supported by embedded operating leverage, multi-asset momentum, and optionality in the clinic, LLY is poised to redefine scale and innovation in curing chronic disease. Its premium valuation is not due to hype but rather an ever-more defensible growth engine. If Lilly can successfully execute on foroglipron and Alzheimer's, the ceiling on valuation increases. For institutions, the most central issue isn't whether the stock is pricey, but whether the market is fully aware of the monetization runway built into its model.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.