Tencent Q1 2025 Earnings Preview: A Critical Inflection Below the Surface

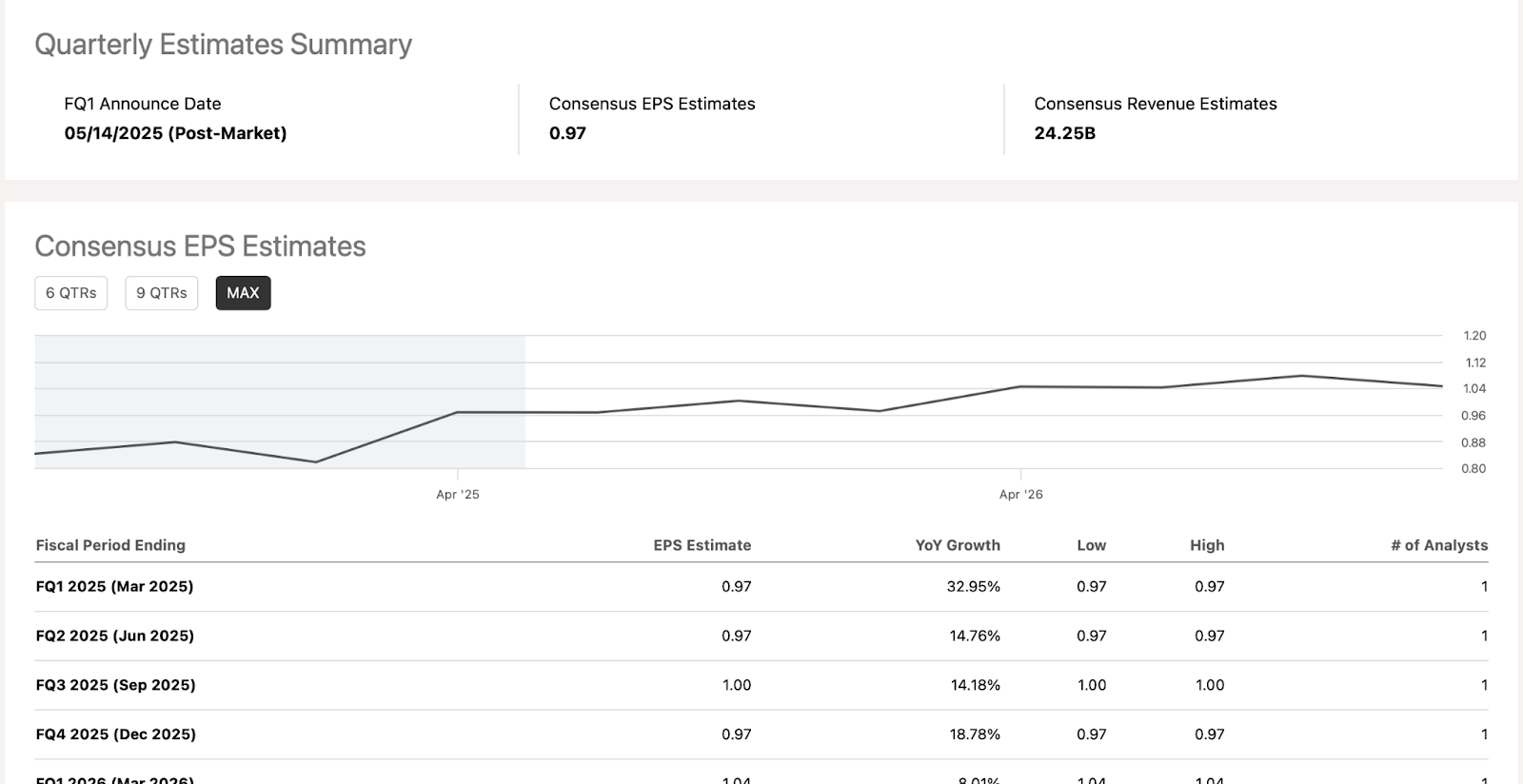

- Q1 EPS estimate is $0.97, implying 33% YoY growth amid easing GPU constraints and AI ramp-up.

- Marketing services revenue rose 20% in 2024, with AI-powered Video Accounts growing over 60% YoY in Q4.

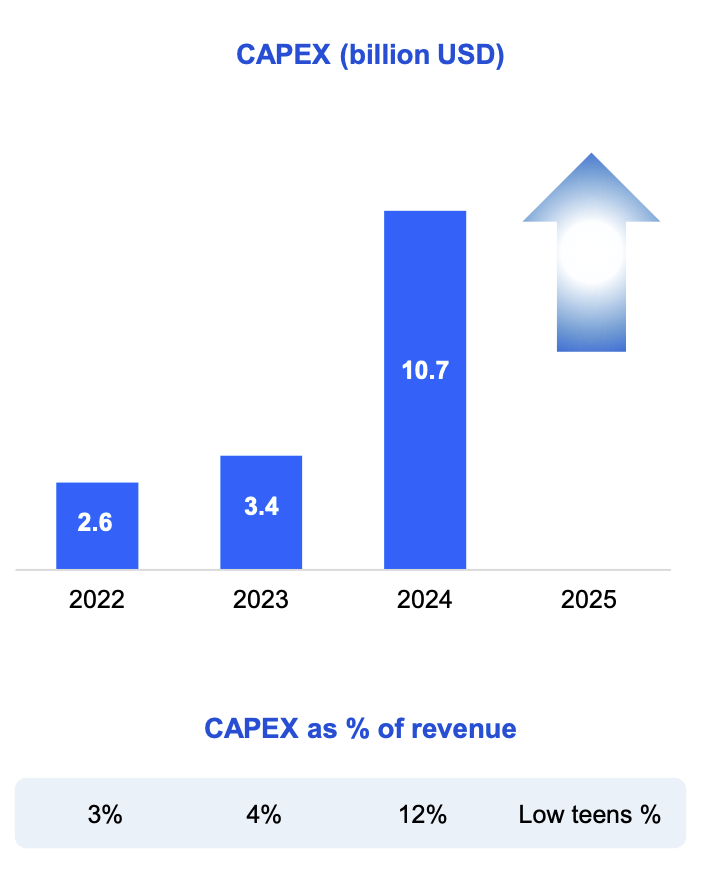

- CAPEX surged 387% YoY in Q4, yet gross margins expanded to 52.9%—a rare capital efficiency signal.

- Yuanbao DAUs grew 20x in two months, positioning Tencent as China’s leading consumer-facing AI platform.

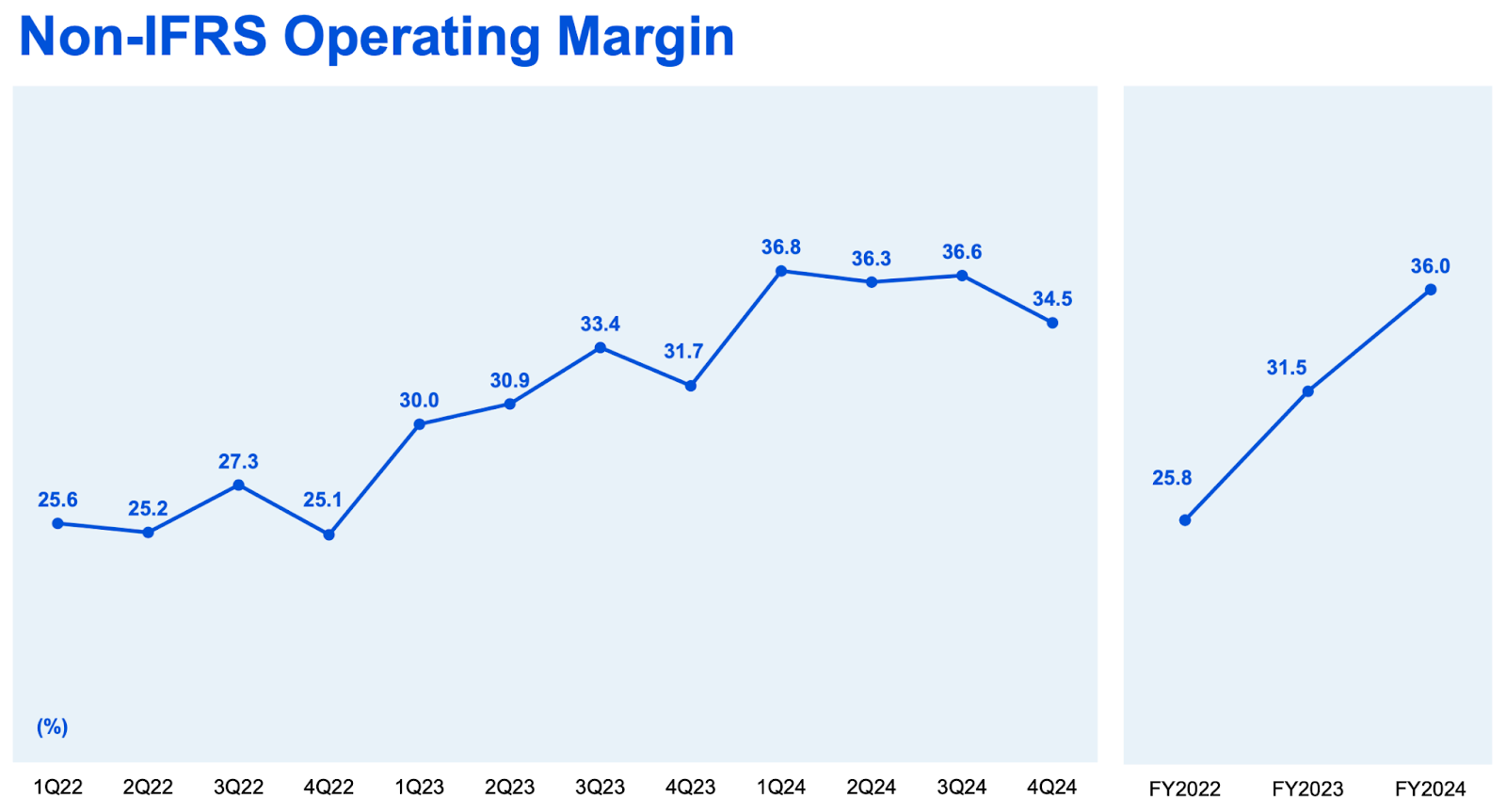

TradingKey - As Tencent (TCEHY) is set to report Q1 2025 earnings today after the market close, the market's eyes remain on macro headwinds-China's slow-moving consumer recovery, regulation overhangs, and the unfolding AI race. But the more compelling fundamental narrative below the surface is that Tencent is evolving from a traditional internet conglomerate into a vertically integrated monetization platform native to AI. With Q4 2024 already providing non-IFRS net income growth of 30% YoY and gross margins reaching 52.9%-despite a 387% spike in CAPEX-the upcoming report gives investors a glimpse into Tencent's operational leverage, cadence of AI commercialization, and capital allocation rigor.

The Q1 configuration is compelling. Street estimates continue to be anchored around high-single-digit revenue growth and flattish operating margins based on a defensive view of cloud bottlenecks and gaming comps. However, a few high-frequency indications imply a beat-and-raise quarter. Specifically, GPU supply constraints that impacted external cloud revenue in Q4 have started easing up with Tencent accelerating GPU purchases and deployment. This should accelerate revenue recognition across Tencent Cloud and enterprise-oriented SaaS tools like WeCom and Knowledge Engine. Furthermore, ad monetization through AI-powered Video Accounts and Mini Programs saw breakout growth in Q4 (+60% YoY for Video Accounts), setting up Q1 for double-digit growth in marketing services.

Source: Tencent

On the consumer side, Yuanbao, the company’s AI-native assistant, is a soundly performing top-3 DAU AI app in China that more than 20 times increased DAUs within February and March. Though not yet a substantial revenue contributor yet, it signifies Tencent’s deep embedding of basis models across the Weixin, video, and content domains. The strategic significance? Tencent’s investments in AI are starting to turn R&D cost centers into monetizable experiences.

Financially, Q1 should show if Tencent is able to sustain or widen its gross margin base over 50% despite digesting record AI-related capex. The key swing driver continues to be free cash flow, which evaporated in Q4 as a result of front-end loaded infrastructure spend but should start normalizing as AI monetization ramps up and operational discipline remains.

In total, this quarter is not solely focused on headline EPS, but rather proof of Tencent’s emerging infrastructure of AI maturing into a monetization machine. If the company guides towards ramping up revenue streams from AI and shows early rewards from Yuanbao and GPU cloud, the valuation reset that Tencent has not achieved since 2021 might finally get underway.

Q1 2025 consensus normalized EPS is $0.97, a 32.95% year-over-year growth versus Q1 2024. This comes on the heels of a solid Q4 2024 beat when Tencent reported $0.82 EPS that surprised the consensus by $0.01 and took in $23.85 billion of revenue, $649 million more than consensus.

In the context of the broader picture, Tencent's forward EPS is expected to advance from $3.77 in 2025 to $4.16 in 2026 with a 10.3% forward growth rate. This trajectory puts its forward P/E at 17.39 and is conservative given the company's Rule-of-40-like growth trajectory (30%+ EPS growth coupled with margin expansion) and increased monetization leverage off of AI. Crucially, analysts have increased the 2025 EPS estimate once within the last 90 days with no downward revisions, demonstrating a high degree of conviction prior to the report.

QoQ Tencent has topped the bottom line in four of the last five quarters with a small miss of $0.02 in Q3 2024. This beat streak, together with the resolution of the headwinds in the cloud business, the adtech resilience and favorable seasonability in the games business, is a high-odds bet for a Q1 2025 positive surprise.

Source: Seeking Alpha

Behind the Moat: Tencent’s Platform Flywheel Enters A New Era

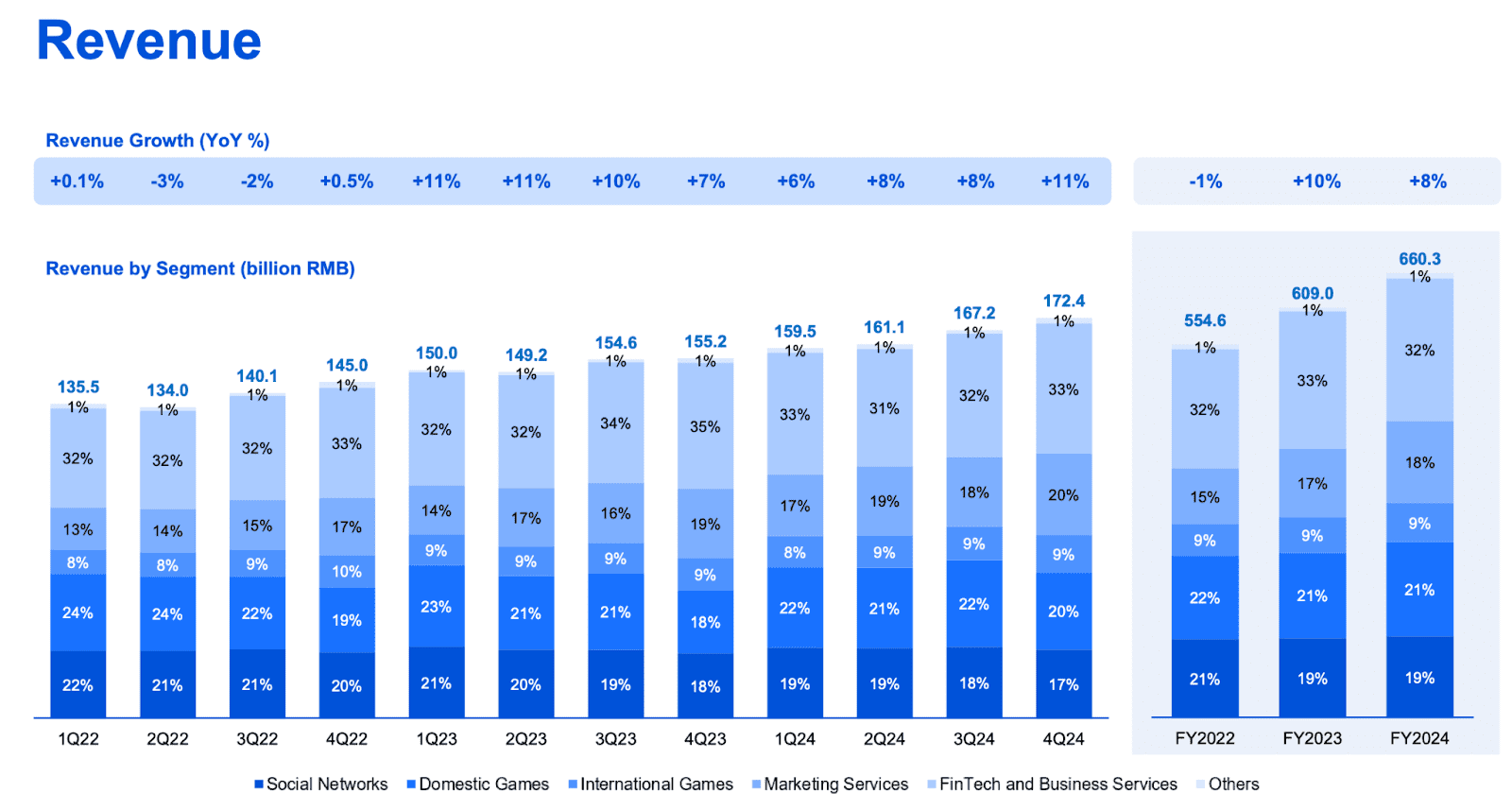

Its business model is one of the most defensible in Asia with the three-engine platform of value-added services (VAS), FinTech and business services (FBS), and marketing services. The VAS division that comprises games and social networks continued to make up 48% of 2024 revenues, with the game business earning RMB 197.7 billion in both the local and international markets. A highlight is that older titles such as Honor of Kings and Peacekeeper Elite continue to achieve double-digit growth, but new IPs such as Delta Force earned RMB 1 billion+ in Q4 alone. It testifies to Tencent’s expertise in creating evergreen games that have a low rate of monetization decay in an otherwise churn-prone industry.

The FBS business division consisting of payments, cloud, and productivity offerings such as WeCom and Tencent Meeting accounts for 32% of overall revenue but punches well above its weight in margin growth. While the externally oriented cloud business has been restricted by the allocation of GPUs towards internal consumption, AI-native enterprise software solutions such as the Hyper Application Inventor (HAI) and Knowledge Engine are developing incremental demand across high-value verticals such as e-commerce and financial technology. Management has indicated that the bottleneck in GPUs is easing out with new buys in Q4 expected to make their way into commercial applications by mid-2025, which will allow for greater margin capture.

In the meantime, the marketing services business is quietly establishing itself as Tencent’s monetization driver. With RMB 121.4 billion of 2024 revenue (+20% YoY), the business is growing faster than any other with deep LLM embedding into its adtech platform. The AI-powered re-ranking and ad generation functionality not only increases ROI for marketers but is materially driving click-through rates. This reinforces the overarching thesis: Tencent is converting its engagement graph and self-owned data into margin accretive infrastructure, a characteristic of few comparable global peers.

Source: Tencent

The Monetization Engine: Turning AI into a Growth Multiplier and Not a Cost Center

Tencent's AI strategy is increasingly turning into a full-stack monetization flywheel. Tencent's HunYuan Foundation Model has ranked best-in-class in image, video, and 3D generation on benchmarks such as FlagEval and Hugging Face. The real breakthrough is in application-layer traction. Yuanbao, Tencent’s native app that combines LLMs with Tencent’s internal data (Weixin, QQ, Docs), has grown DAUs 20-fold post-launch. This consumer-grade uptake is monetizable on Weixin Pay, mini-program transactions, as well as AI-generated digital goods, enabling a new revenue stream fully decoupled from advertising.

In addition, Tencent is applying its AI stack horizontally across games (in-game messaging bots, automated 3D), entertainment (editing and distribution of content), and enterprise SaaS. Adtech is a beneficiary in a huge way: video account ad revenue increased more than 60% YoY in Q4, thanks in part to generative creatives and precision targeting. This is an underappreciated driver: being able to automate and personalize delivery of advertising has the potential greatly to grow ARPU without raising CAC, an echo of what Meta saw with Advantage+.

Financially speaking, Tencent's CAPEX profile speaks for itself. Operating CAPEX increased 421% YoY last Q4 to RMB 34.9 billion. R&D expenditure increased 11% in 2024 and accelerated 21% YoY last Q4. These investments have kept FCF in check temporarily (down 87% last Q4), but gross margins continue raising the bar, from 47.5% to 52.9% in the last one year, reflecting cost absorption discipline. Tencent’s capacity to scale up on AI without losing margin is a key proof of concept for capital efficiency in the era of LLMs.

Source: Tencent

Valuation: Market Anchored in Legacy Multiples with Unpriced AI Optionality

Currently, Tencent is priced at a forward P/E of 17.55 and a trailing non-GAAP P/E of 20.28, both of which are premiums of 38.5% and 63.7% against the Communication Services median. Although the raw premium might seem high on the surface, it masks a more fundamental misclassification: that the market is valuing Tencent against legacy telco and digital advertising peers instead of full-stack infrastructure builders of AI such as Meta (META) or Alphabet (GOOG). Even when we adjust the PEG for growth and monetization quality factors, Tencent’s PEG of 0.33 is far below the sector median of 0.49, implying the stock is cheaper against its earning growth trajectory.

The EV/Sales (forward) multiple of 6.16 looks rich against the 1.86 median for the sector (+230% premium), but the distortion is primarily fed by Tencent’s better margin business mix. Gross margins reached 52.9% in FY2024 from 47.5% in FY2023, both reflecting operating leverage and premium monetization of AI-augmented services. The 17.08 Price/Cash Flow multiple, high against the 7.48 median, needs to be put into context against Tencent’s strategic spending on CapEx for building a long-term flywheel of revenue in cloud, advertising, and consumer-oriented AI tools such as Yuanbao.

Tencent's 4.55 Price-to-Book is 131% over the peer group average, again, misleading when excluding the RMB 570 billion of public equity holdings and RMB 336 billion of private investments parked on the balance sheet. Eliminating these non-core investments leaves a platform business valued more in the 2.2–2.5x book range on an operating basis, more comparable to asset-light software peers rather than capital-heavy telcos.

Lastly, the dividend yield of 0.88% is weak against a median of 3.95% for the sector, but Tencent’s shareholder performance is fueled mainly by buybacks. Tencent returned more than HKD 112 billion of stock in FY2024 (127% YoY), a more tax-effective and more flexible type of capital returned that increases per-share value with no long-term payout inflexibility.

In summary, headline valuation multiples look extended on legacy benchmarks but conceal the evolution from a conglomerate framework towards an AI-levered platform with rich monetization optionality. One is likely to rerate when investors start valuing Tencent on an infrastructure and software-as-a-service basis instead of legacy advertising and game multiples. A reasonable valuation range applying 20–22x non-GAAP FY2025 EPS (~RMB 27) gives a fair value estimate of $85–$93 per ADR with 30–40% potential upside.

Conclusion

Tencent's Q1 2025 figures might finally turn the narrative around. Legacy businesses compounding and AI investments ripening into monetizable offerings, Tencent is not simply a social or a gaming firm anymore , it is silently building China’s consumer and enterprise backbone of AI. The market is still undervaluing this pivot.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.