Pershing Square 2025Q2 13-F: Even Ackman got hooked into Mag-7

TradingKey - Bill Ackman is undoubtedly one of the household names on Wall Street. His bottom-up value investing style combined with a solid amount of activism within his holdings has always attracted a lot of attention from the rest of the investing community. No wonder, the 13-F filings of his Pershing Square are among the most anticipated, because being part of Ackman’s portfolio, largely means that the stock is poised for long-term gains.

For example, earlier this year, the share price of Uber jumped 7% right after Ackman disclosed his stake in the company.

So, what happened to Pershing Square in Q2?

Pershing Square registered $13.7 billion of assets under management (AUM) as of June 30th, this is 15.1% more than the beginning of the quarter. This excludes the position of United Music Group (UMG), listed in the Netherlands and not disclosed in the 13-F. Out of these 15.1%, 12.6% is the actual fund performance, and the rest is from fund inflows. 12.6% is not a bad performance if we compare it to the 10.57% return of S&P500 during the same period.

The solid performance was mainly driven by the impressive rally of Uber (+28% in Q2) as well as the other tech holdings – Amazon and Google.

However, we know quarterly return is of a little importance to Ackman, as his investment time horizon can span 10 years and beyond.

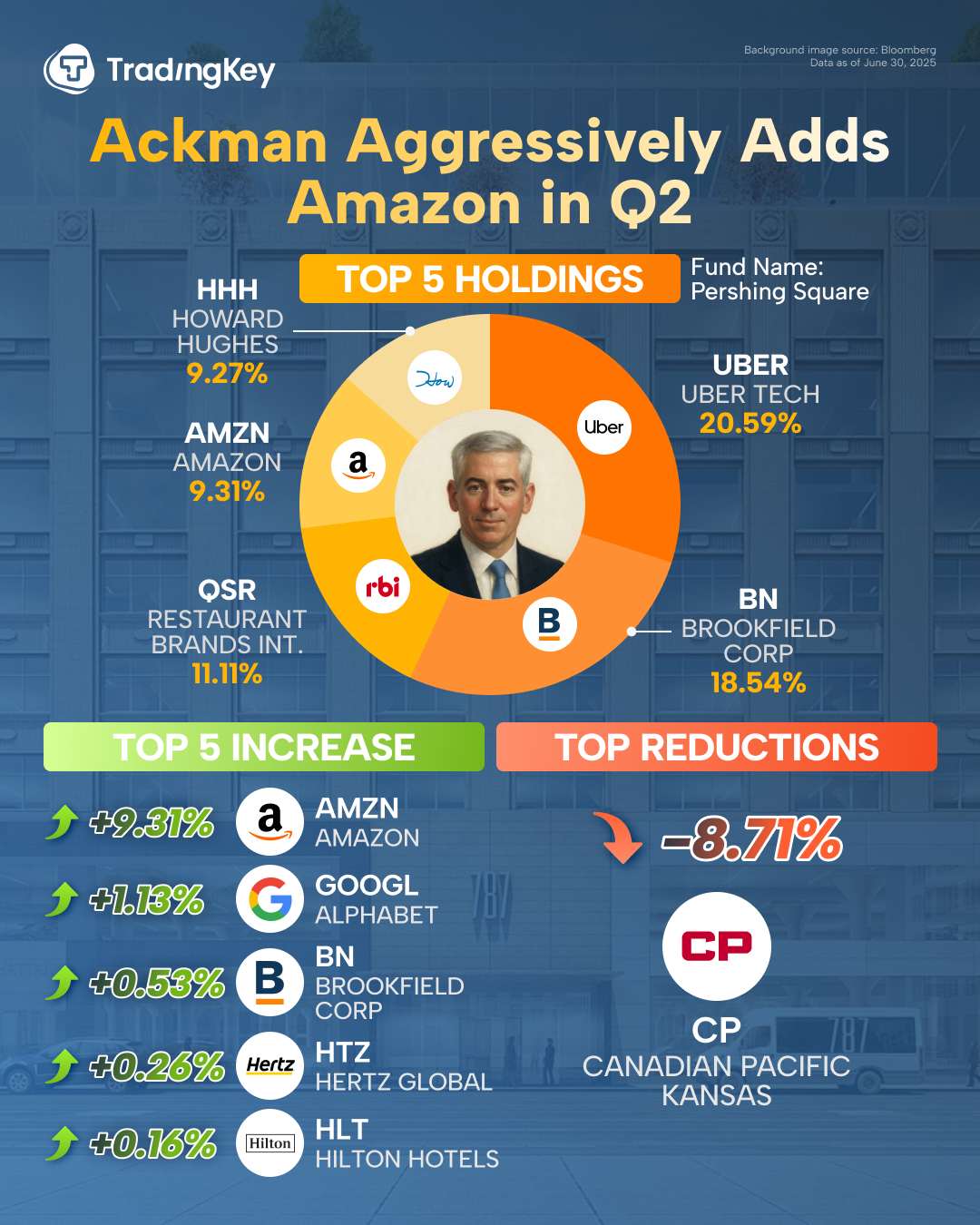

Top Holdings and Trades

Ackman is a high-conviction investor, which means he has stakes in very few companies – 11 only (with UMG it will be 12).

In Q2, Pershing Square added one company, increased the stakes in four, and exited another.

The current top five holdings are:

Among the top five holdings, there were no changes at all, except for a slight increase in Brookfield (BN). Ackman likes BN due to 1) its well diversified real estate portfolio of infrastructure and renewable power assets; and 2) strong trust in the CEO Bruce Flat, who is often dubbed as “Warren Buffet of Canada” due to his superior capital-allocation skills.

As for Uber, the strong growth in profitability due to improved operational efficiencies, combined with attractive valuation of 15x PE, totally justifies it being the top holding in Pershing Square.

Dip into Mag7

The top two biggest buys of Ackman in Q2 were the tech giants Amazon (AMZN) and Google (GOOGL):

.jpg)

Ackman announced his newly built stake in Amazon in late May, at the average price of $219.19, taking advantage of the tariff chaos that made the stock price sink. For him, Amazon has everything he needs – dominant market share, long-term growth potential and capable management.

Ackman’s position in Alphabet is not new. In Q1 he actually trimmed its stake there, but now we see 21% increase – obviously, the trim last quarter was more of a tactical move rather than losing conviction on Alphabet. What is worth noting is, Pershing Square holds both classes of Alphabet shares – GOOGL (with voting rights) and GOOG (without voting rights). However, he only increased the voting class of shares, which somehow aligns with his activist nature of trying to be more involved in the company’s strategic decisions as he accumulates more voting rights.

Only one trim in Q2

The only selling that happened in Pershing Square last quarter was the liquidation of the Canadian Pacific Railway (CP) position. Actually, he announced this back in May. Ackman started piling up its position in 2021Q4 and the total amount of capital gains and dividend received during these roughly three years is around $110-140 million.

Ultimately, he did not see any specific issues with the business model or the management of the firm, however a portfolio manager should maximize the profits of his partners by moving funds to opportunities with a higher potential return.

Trends

In summary, from his recent investment decisions, we can assume Ackman is bullish on the development of US tech. He probably sees very solid business moat and ability to growth profits. Ackman also appears to trust the management of these firms.

He also cares about timing. In Q1 he bought Uber when the company was largely dismissed by investors as not being able to survive the robotaxi revolution. In Q2, he bought Amazon when everyone was anxious about the tariff turmoil.

What can also be observed is he is slowly moving away from the typical activist investment he has been doing in the last twenty years (buying companies with a lot of inherited problems and relying on management-driven operational improvements) towards investing in well-established business models with already-good management, thus, the transition from restaurant chain stocks to big tech.

Takeaways

For retail investors like us, we simply cannot buy a huge share in a firm and start activist campaign. However, what we can adopt from Ackman’s investment style is to always look for high quality businesses with growth potential and highly capable management. Oftentimes such companies will face macro turmoil events like tariffs that can bring the stocks to attractive valuations, this opening up great opportunities.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.