Investing in Quantum Computing

- Quantum computing is evolving from a speculative research field into a commercial reality, with applications spanning pharmaceuticals, logistics, finance, and climate modeling.

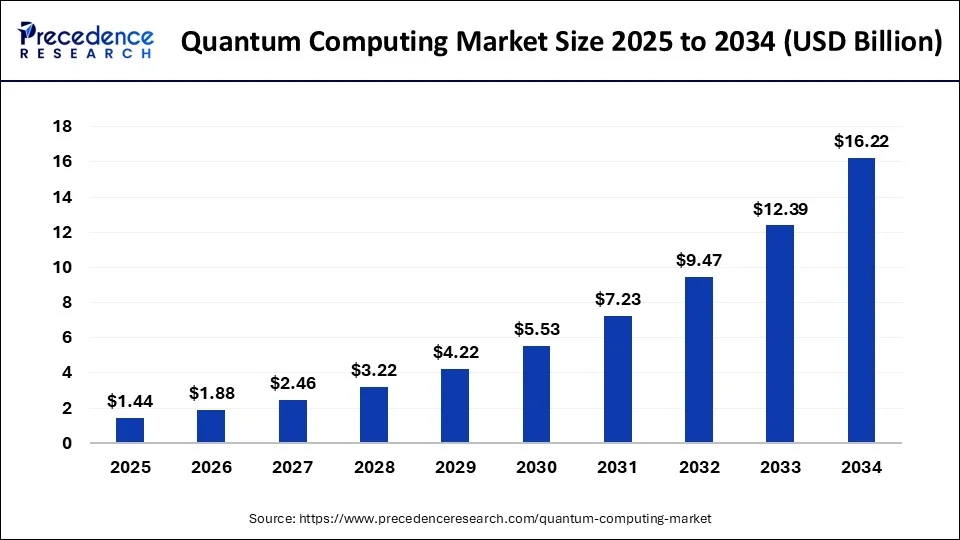

- The global quantum computing market is expected to grow from $1.44 billion in 2025 to $16.22 billion in 2034, driven by hardware, software, and algorithmic breakthroughs.

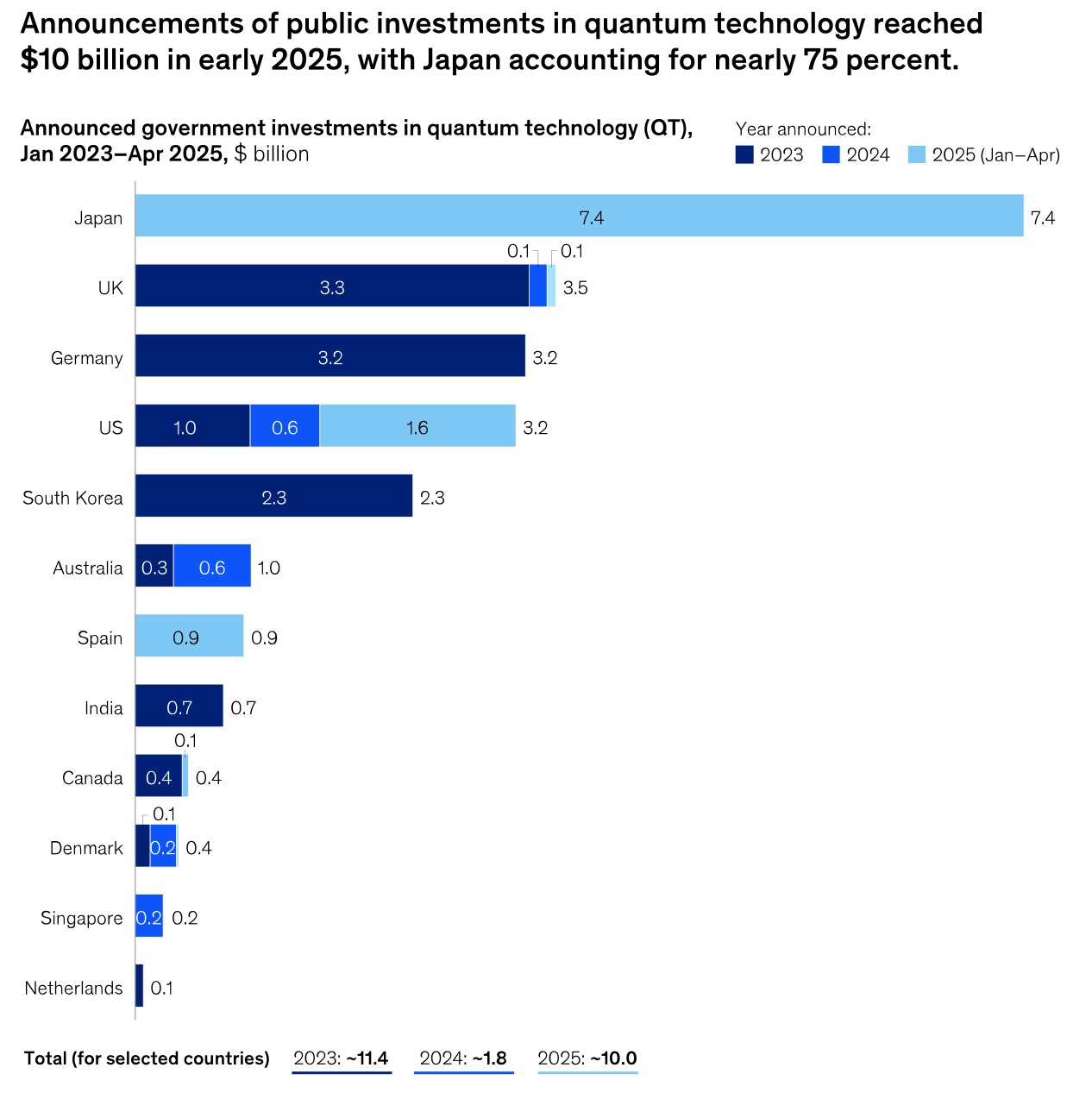

- Public investment surged to $10 billion in early 2025, with Japan contributing nearly 75% of the total, highlighting its strategic and geopolitical importance.

- Investors can gain exposure through a mix of tech giants with quantum divisions, pure-play startups, enabling technologies, and thematic ETFs to balance volatility with long-term potential.

TradingKey - What was once confined to university labs and science fiction books is now becoming one of the most disruptive technologies of the next twenty years, set to transform industries from pharmaceuticals and materials science to finance, logistics, and climate modeling.

Though itself only in early phases of commercialization, hardware and algorithm and fault correction advances are propelling quantum systems into more practical day-to-day application. Investors regard this as the inflection point where an earlier speculative field begins taking form as an identifiable and investible ecosystem.

The global market of quantum computing will expand from $1.44 billion in 2025 to $16.22 billion in 2034, exhibiting rapid adoption fueled through technological developments and increasing commercialization.

Source: https://www.precedenceresearch.com

From Theory to Emerging Commercial Reality

Quantum computing uses quantum mechanics rules of superposition, entanglement, and interference to compute information qualitatively different from classical computing. Qubits (quantum bits), instead of binary binary (0s and 1s), hold more than one state and thus certain computation is calculated exponentially faster.

The technology has made significant advances over the past several years. Early systems with a handful of qubits and short coherence times have evolved into systems with hundreds of physical qubits and greater focus on stability and fault tolerance. Large tech industry players such as IBM, Google, and Microsoft and niche startups such as Rigetti Computing, IonQ, and D-Wave compete to develop architectures scaling into thousands or millions of logical qubits necessary for commercially significant problems.

What's new is that quantum computing has emerged from the ivory tower and into corporate boardrooms. Quantum teams are being built at giant corporations, national governments are investing in quantum programs at historic heights, and initial pilots of commercialization have measurable value. Adoption will be universal years down the road, but the technology is on the trajectory of early cloud computing or AI-underestimated near-term but very disruptive far-term.

Market Size and Driver of Growth

The world market for quantum computing in 2024 stood in the low billions of dollars but is predicted to reach $90–$100 billion in 2040 provided the scaling issues are solved. These drivers are of both technological and demand-related natures.

Technologically, quantum error correction breakthroughs, advanced cryo systems, and hybrid quantum-classical computing architectures are gaining traction. The industry also is trending toward cloud-based quantum access and simplifying experimental barriers for developers and companies.

From a demand side, quantum computing is attractive for tackling optimization, simulation, and crypto problems that cannot be solved on traditional machines. In pharmaceuticals, quantum algorithms could significantly compress drug discovery timescales through simulation of molecular interactions with previously unimaginable accuracy. In logistics, they could untangle complicated supply chains in real time. In finance, they could have opportunities for innovation in portfolio optimization and risk modeling.

The government also has a determining role in the industry's evolution. U.S., EU, Chinese governments and governments everywhere all spend heavily on quantum research as all of them race for technological dominance and also consider the economics and the national security aspects of it. From a geopolitical point of view, this adds another dimension to the industry's strategic importance. Lastly, public investment in quantum technology surged to $10 billion in early 2025, with Japan contributing nearly three-quarters of the total.

Source: https://www.mckinsey.com

Key Players and Ecosystem Hierarchy

The investable quantum computing landscape covers multiple segments:

Hardware Developers: IBM and Google lead in this category as well, with IBM aiming at 1,000+ qubit systems in 2026 and Google on track for fault tolerance for quantum computing. IonQ and Rigetti are publicly traded pure plays but very early-stage and low revenue. D-Wave has a niche interest in quantum annealing as opposed to universal quantum computing and aims at concentrating on problems of optimization.

Software and Middleware Vendors: These comprise firms such as Zapata AI, QC Ware, and Cambridge Quantum (formerly part of Quantinuum), which develop layers of software that push the bounds of quantum computing within corporate users' and developers' reach. This category potentially has quicker near-term monetization than hardware.

Quantum-Enabling Services: Cloud service providers like Amazon Web Services (Braket), Microsoft Azure Quantum, and Google Cloud offer users access to quantum hardware via pay-as-you-go models and thereby generate early revenue and developer communities.

Component Providers: Cryogenics, advanced materials, and precision electronic control offer the primary supply chain. Typically flying under the radar, these component providers might witness increasing orders as scaling of the hardware gains traction.

Volatility and Risk Profile

Despite the euphoria, quantum computing is a risky investment theme. Timelines on technicalities are always risky, scaling hundreds of qubits all the way up into millions and fault-tolerant is a big problem. Pre-profit market players on average have cash-burn rates that require ongoing raises of capital.

Public valuations of markets fluctuate unpredictably on the strength of one announcement, research advance, or shift in investor sentiment. In addition, the industry has the possible competitive threat of classical computing breakthroughs like dedicated AI accelerators that might relax the pressure for quantum answers in certain applications.

Regulatory and geopolitical considerations also create uncertainty. Export controls on quantum technologies are increasing between China and the U.S., and could affect market access and cooperation.

Strategic Investment Methodologies

Due to the industry’s nascent stage, a diversified and staged allocation framework is justified. Investors can balance exposure to mature tech behemoths with quantum projects (Microsoft, Alphabet, IBM) with lesser pure plays that have significant upside such as IonQ or Rigetti. This method combines the stability of businesses through broader revenue streams and the optionality of specialization innovators.

Venture mentality is needed, position sizing must also provide for high volatility and extended development times. Quantum and next-generation computing thematic ETFs provide one type of exposure with diversified breadth through several companies and layers of the supply chain.

Another way is indirect investment through facilitating technologies: cryogenic equipment manufacturers, advanced semiconductor specialists, and cloud services with quantum access platforms. Such businesses might achieve revenue boost through quantum adoption while not being completely reliant on the latter's timescale.

Outlook: A Decade of Gradual but Accelerating Impact

The next five years will see quantum computing still in the early adoption phase and the bulk of all the commercial activity devoted to hybrid quantum-classical application application cases. But during the early 2030s fault tolerance should bring out apps of great economic value and spark an adoption spurt in those sectors whose computational demands are highest. The horizon to widespread profitability for pure-play quantum startups remains opaque, but historical precedent is that once practical utility has been demonstrated, adoption has been demonstrated as rising very rapidly, as it has with cloud and AI.

For patient capital, the payoff potential is significant, especially if investments are timed to coincide with technical milestones and market validation events. Essentially, quantum computing is where long-term innovation and short-term volatility meet. For investors willing to brave the risk tolerance, it is not simply another emergent tech theme, but rather a paradigm shift in the manner the world processes information.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.