SOFI: The Invisible Infrastructure of Modern Banking

- SoFi reported a record Q1 2025 adjusted net revenue of $771 million, up 33% YoY, with EBITDA up 46% to $210 million.

- Fee-based revenue hit $315 million, representing 41% of total revenue and growing 67% YoY, signaling a shift to capital-light income.

- SoFi's Loan Platform Business originated $1.6 billion in third-party loans, part of $7.2 billion total originations, with minimal credit risk.

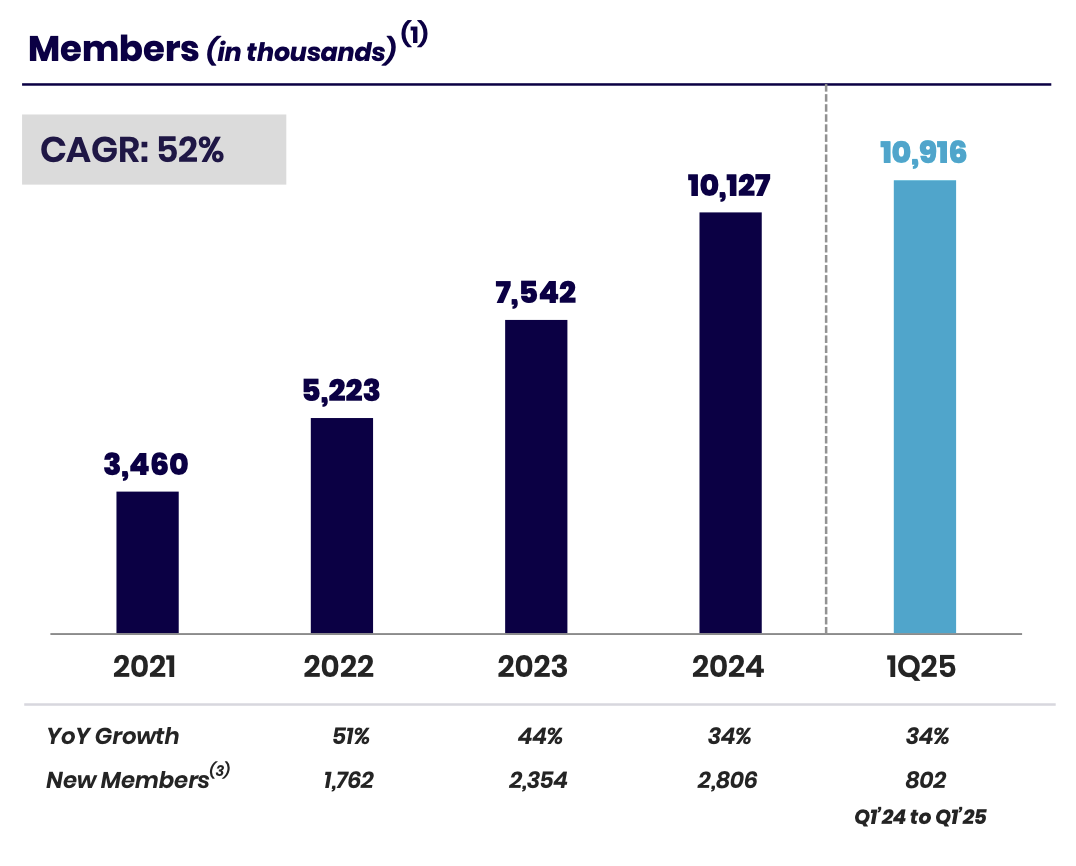

- Member growth reached 10.9 million (+34% YoY) and total products rose to 15.9 million (+35% YoY), reinforcing its cross-buy ecosystem.

TradingKey - On the surface, SoFi (SOFI) is seemingly another finance app competing on superficial user interfaces and reward gimmicks. And in doing so, such a view overlooks the structural transformation in train. Under CEO Anthony Noto's direction, SoFi has designed a vertically integrated, native digital financial platform whose real value lies beneath the surface: capital-light revenue streams, embedded network effects, and self-sustaining cross-buy loop that traditional banks are unable to reproduce.

While critics allude to lofty valuation multiples and periodic profitability, Q1 2025 performance reveals quite the alternative. SoFi is no longer merely growing, it is scaling with operating leverage, generating margin expansion and durable returns while systematically derisking its business model.

The company's record Q1 adjusted net revenue of $771 million posted a year-over-year increase of 33%, and adjusted EBITDA jumped 46% to $210 million, each of these representing five-quarter peaks. Crucially, that expansion is no longer lending-only. Fee-based revenue came in at $315 million, up by 67% year-over-year and now accounting for 41% of total adjusted net revenue. This is indicative of structural movement towards recurring, capital-light income. What lends this transformation credence is not only the top-line metrics but also where they're coming from: diversified monetization across SoFi Money, SoFi Invest, and the growing Loan Platform Business, each supporting a high-velocity system enabled by product integration and cross-utilization.

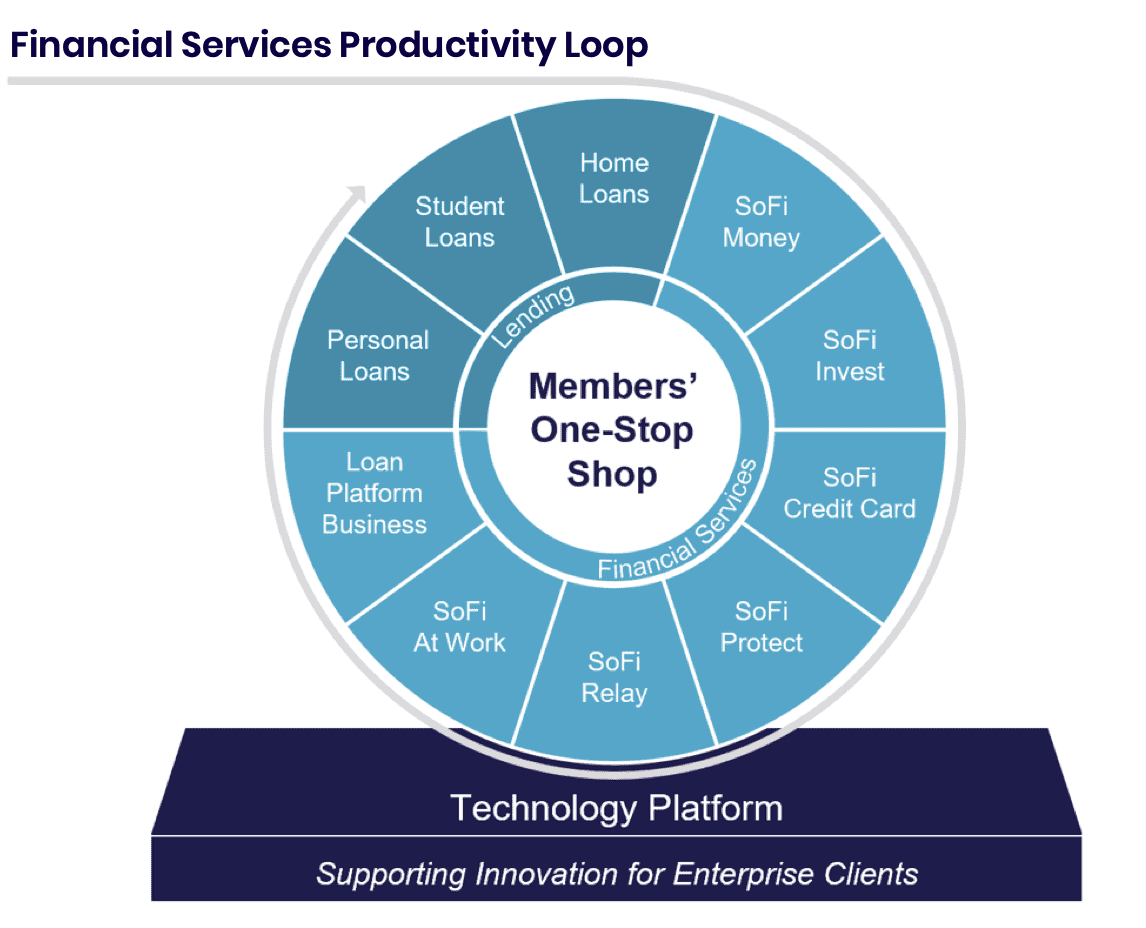

SoFi's Financial Services Productivity Loop (FSPL) is more than a marketing phrase. With nearly 90% of new subscribers to SoFi Plus already existing members, and more than 75% of new subscribers taking on two or more additional products, density in the network is growing organically. This is reducing customer acquisition expense and increasing customer lifetime value. At a time when all but the strongest fintechs are looking to raise capital or beg for mercy from regulators, SoFi is compounding strength in operations and expanding its moat.

Source: SoFi Q1 2025 Presentation

The Flywheel of Financial Fortress

SoFi's business model is actually quite simple but deeply scalable: capture members cheaply with brand-led, integrated marketing, offer several financial products in one interface, and take greater margins by owning the entire stack from deposits through loan origination to payments infrastructure. What sets SoFi apart from incumbent banks and unbundled fintechs is the ownership of each rung of the customer and revenue stack.

Central to this framework is a product suite that impacts every financial need. SoFi Money enables a feeless, high-yielding banking platform supported by $27.3 billion in deposits, driving a low-cost funding pool that’s 189 basis points lower than warehouse financing. SoFi Invest brings ultra-wealthy tools to the masses, and SoFi Relay is a no-revenue on-ramp with robust downstream monetization opportunities. Relay, with 5 million users today, converts at high velocity: one-third of new Relay-first customers adopt three or more additional products. This journey of users from awareness to multi-product engagement is the heart of FSPL.

Loan Platform Business (LPB) introduces a high-margin, capital-light layer. Originating loans on behalf of third parties and earning referral, origination, and platform fees, LPB originated $1.6 billion in loans this quarter alone. Third-party capital from Blue Owl, Fortress, and Edge Focus enabled combined originations to reach an all-time high of $7.2 billion. LPB is fully fee-based with minimal credit risk, enabling SoFi to grow revenue without growing its balance sheet. Meanwhile, the Tech Platform segment, supporting 158 million accounts, enhances operating efficiency by distributing infrastructure costs between internal and external monetization layers.

SoFi’s advantage is not only one of product breadth, but of sequencing. The company takes customers from financial milestones, Relay to Money to Invest to Loans, in a sequence that drives retention and share of wallet. This approach has fueled growth in members to 10.9 million (+34% YoY) and number of products to 15.9 million (+35% YoY), resulting in revenue-per-user expansion and margin leverage that surpass rivals.

Source: SoFi Q1 2025 Presentation

A Redefiner of Category in a Competitive Fintech Market

SoFi’s multi-vertical strategy positions it at the intersection of several significant financial verticals: lending, wealth, banking, and embedded finance. The fact that it is able to aggregate these services on one integrated platform is a powerful challenge to both traditional institutions and pure-fintech players. While alternative banks like Chime or Revolut are dependent on partner banks, SoFi has its own nationally chartered bank and is 90% funded by deposits. This structural strength not only enhances unit economics but also brings greater regulatory clarity and funding stability.

Traditional banks, bound by old infrastructure, are not able to match SoFi's agility. Incumbents are able to deliver individual products but not the integrated product or pace of innovation that SoFi is able to offer. Fintech competitors such as LendingClub or Affirm will deliver strong lending in niches or verticals but are not able to match cross-sell mechanisms and depth of engagement required to capture long-term lifetime value. Robinhood's brokerage platform, to take one example, has compelling engagement but not SoFi's lending stack or banking rails. Even Square's Cash App platform, while extensive, is weighted towards SMBs and P2P payments with less momentum in regulated credit products.

Significantly, SoFi is not only scaling for consumers, it’s institutionalizing trust. Brand extensions through partnerships with the NBA, the CMA Fest, and the TGL Golf League push the name into mainstream culture and translate into actual momentum. The 7% unaided brand recognition metric, while appearing low, is impressive for a digital-only financial brand and represents long-term equity building. Combining with the technology-powered model of user acquisition and fast product rollout pace, SoFi is in a rare hybrid space as a consumer-facing financial utility with infrastructure-level capabilities.

Margins Meet Multiples: Breaking Down the Valuation Premium

SoFi's valuation multiples, though high, are commensurate with its premium fintech positioning. At a Non-GAAP P/E (TTM) of 73x and Non-GAAP P/E (Forward) of 44.9x, both are trading 3x–5x sector median, investors are accounting for SoFi's move toward fee-based, capital-light, high-margin revenue. The company's 41% fee-based revenue mix and increasing cross-product participation warrant this premium, highlighted by its amazing YoY revenue growth and EBITDA growth in Q1 2025. At GAAP P/E (FWD) of 45.8x, the difference in valuation is warranted due to non-cash expenses such as SBC.

Its price-to-sales (4.4 compared to sector median 2.64) and price-to-book (2.07 compared to sector median 1.17) are high but declining as tangible book value increases to $4.58/share and accretive EPS accelerates. Forward price-to-cash flow of 13x implies a more realistic multiple with normalized free cash flow considered. SoFi is growing with operating leverage, and its vertically integrated model supports customer retention, lowers CAC, and sustains structural margin growth.

Although legacy valuation models may indicate overvaluation, SoFi's platform economics, diversification, and ramping monetization justify the multiples, particularly versus legacy banks or single-product fintechs. Ultimately, the premium has more to do with tomorrow's compounding machine than today's earnings.

Risks: Growth on the Edge of Complexity

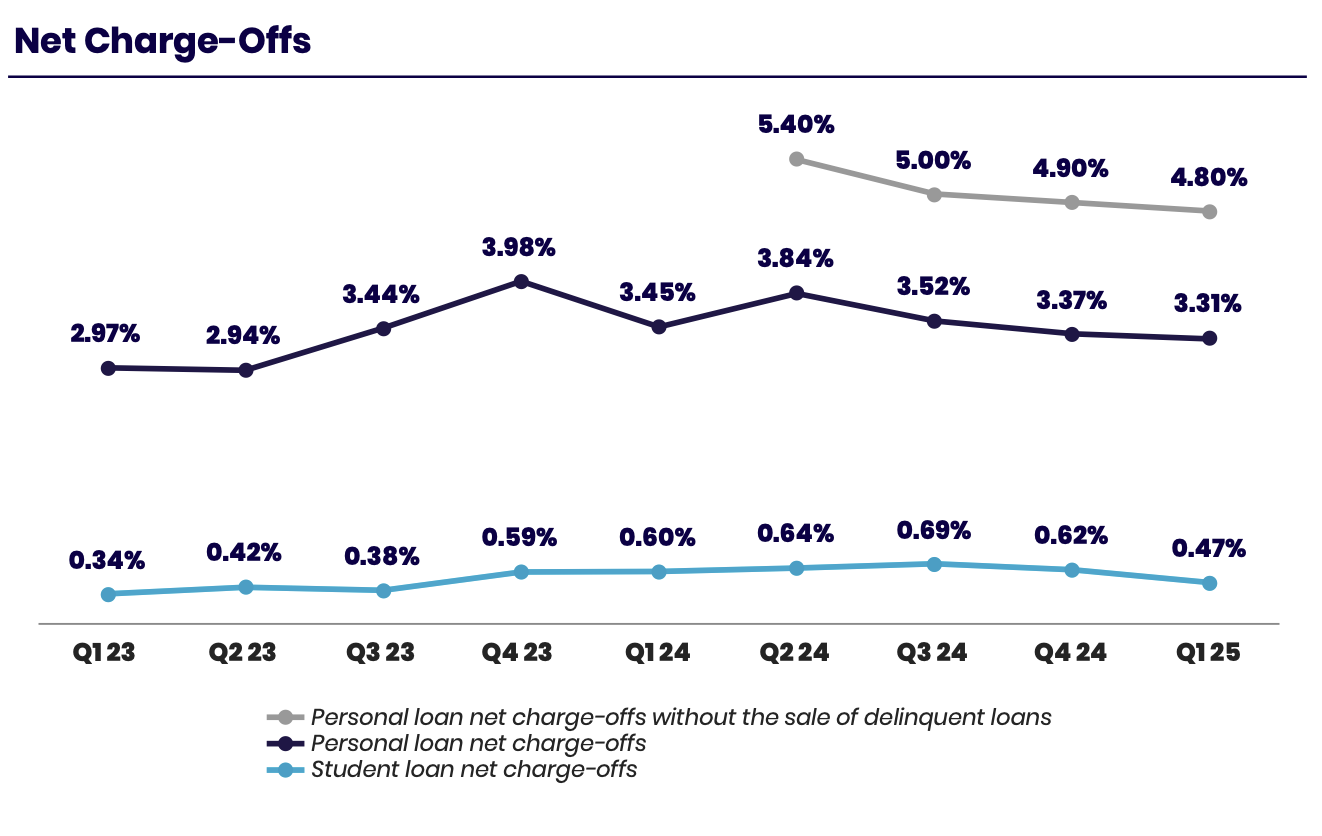

Although strong, the momentum of SoFi is not unproblematic. Among structural threats are regulatory volatility. As both lender and licensed bank, SoFi is subject to increased scrutiny, most specifically with new product introductions such as SmartStart or subscription fees for SoFi Plus. Missteps in regulation may interfere with product momentum or require revenue model adjustments. A second threat is credit cycle timing. Although delinquencies and 90-day delinquencies on consumer loans are headed in the right direction (currently standing at 3.31% and 0.46%, respectively), a macro shock or lending-rate spike may degrade credit quality and necessitate more stringent lending policies, affecting revenue growth.

Source: SoFi Q1 2025 Presentation

In addition, SoFi’s cross-buy loop is not infallible, though strong. It relies on product innovation and maintaining relevance by the company. Cross-buy rates may drop if competitors lower prices or offer better benefits in key products such as SoFi Money or Invest. The company’s rich valuation also heightens sensitivity to execution failures, as with other rapid growth fintechs that fell after growth decelerated or monetization trailed expectations. SoFi's size also brings with it infrastructure and cybersecurity issues. With more than 158 million platform accounts with increasing deposit balances, the operational load increases. A major data breach or service downtime is likely to undermine trust, and along with it, the foundation of the FSPL.

Conclusion

Platform economics compounding into structural alpha SoFi is not so much a fintech growth narrative, but a platform business in the making that sits at the intersection of finance, infrastructure, and consumer loyalty. Its cross-product loop, capital-light scaling model, and strong margin revenue transformation support a compelling argument for sustained value creation. There are risks, but the company is executing with discipline and pace. For institutional investors, SoFi is not only providing optionality, but a plausible route to margin-anchored, multi-segment leadership in digital finance.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.