Microsoft's $70B Quarter: Valuation or Bargain?

- Azure’s revenue grew 33% YoY in Q3 FY25, with most growth from non-AI workloads, demonstrating resilience beyond GenAI trends and proving the strength of Microsoft’s dual-engine cloud strategy.

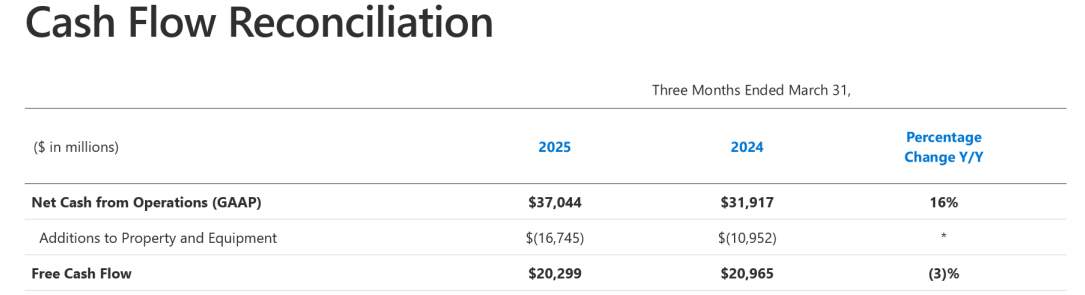

- Microsoft posted $20.3B in free cash flow, with $21B in CapEx, nearly double its recent run-rate, strategically invested in long-duration AI infrastructure with 10–15-year ROI horizons.

- Operating income rose 16% to $32B, while gross margin dollars increased by $4.8B YoY, showing Microsoft’s ability to scale aggressively without compressing overall profitability.

- Despite trading at 32x forward P/E, a blended fair value analysis yields a target of $417–$480 per share, underpinned by 30%+ ROIC and $300B in cloud commitments.

Microsoft's Cloud Supremacy: Maintaining a Moat Powered by AI in Saturated Megatrend Space

TradingKey - Amongst a market awash in AI hype and hyperscaler aspiration, Microsoft (MSFT) is notable not so much by joining the trend but by structurally defining it. Mainstream narratives portray Azure as the firm's lead growth driver, yet closer inspection discloses a more sophisticated thesis: Microsoft's bets on AI are serving as a flywheel to boost monetization, increase operating leverage, and entrench customers deeper in its productivity suite, infrastructure, and enterprise platforms.

The Q3 FY25 report confirms this thesis. Azure increased by 33% year-on-year. Free cash flow reached $20.3 billion. Operating margins widened off the back of a $21 billion CapEx spend, almost all of which is invested in AI infrastructure. Most importantly, most of Azure’s growth came from non-AI workloads, indicating a business model that's not solely reliant on GenAI cycles or GPU economics. Monetizing both AI and traditional cloud demand with this dual-engine approach brings in resilience and separates Microsoft from others pursuing one trendline.

But even with the underlying fundamentals strong, there is skepticism in the market regarding valuation. At more than 11x sales and ~32x earnings on a forward basis, critics will say that Microsoft is priced for perfection. Yet looking closer at the unit economics, margin sustainability, and strategic embedding of AI shows why these multiples are possibly warranted and probably underappreciated on a platform that has Microsoft’s scope and reinvestment effectiveness.

Source: Q3-Deck

From Stack to Stratosphere: Microsoft’s Multi-Layered Business Model

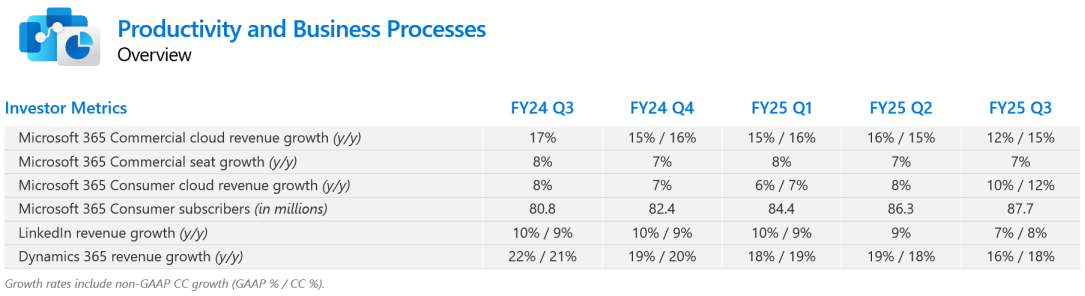

Microsoft's business architecture is one of systematized scalability. Microsoft has three major segments: Productivity and Business Processes, Intelligent Cloud, and More Personal Computing, where all segments are substantively adding to growth and are strategically interconnected.

The productivity segment, led by Microsoft 365, is continuing to yield strong profits. Commercial cloud services in this segment grew in double digits, fueled by seat growth and tiering, specifically to E5 licenses. Integration of Copilot is already serving as a significant monetization lever. This is not a superficial value-add, it increases the stickiness of workflows, lifts average revenue per user, and establishes a repeatable up-sell paradigm that scales with SMBs and enterprise accounts.

The Intelligent Cloud segment, comprising Azure and server products, contributes most of the revenue and operating income these days. The key thing is that Azure's growth is bifurcated. Artificial intelligence services are growing fast, but most of the growth is still coming from traditional workloads. This two-track evolution lessens the susceptibility of Microsoft to AI demand fluctuation and provides more steady returns from infrastructure investments.

In the meanwhile, the More Personal Computing segment, traditionally considered to be cyclical, has been the stealth outperformer. Search and ads revenue increased more than 20%, with AI-powered search experiences driving the boost. Xbox services and Windows OEM recovered modestly, supported by new product cycles and synergies from the ecosystem. Far from serving as a drag on margins, this segment became a significant contributor to bottom-line growth during the quarter.

In general, Microsoft's model illustrates how profound platform integration across cloud, devices, AI, and software not only converts into growth in the top line but also into monetization accuracy. While competitors have siloed products, Microsoft monetizes along the value chain, from cloud computing to productivity tools to operating systems, with AI serving as the connective tissue.

Source: Q3-Deck

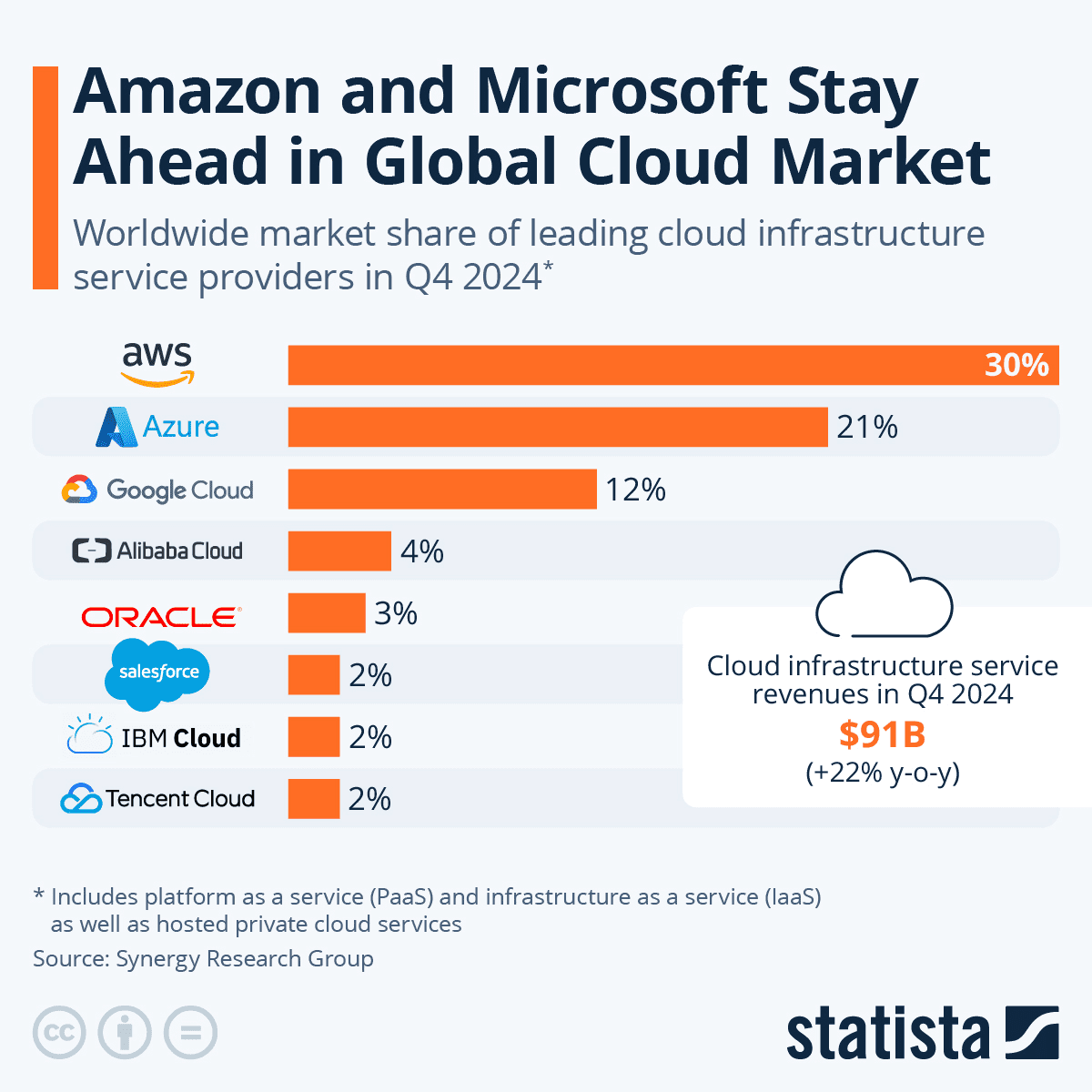

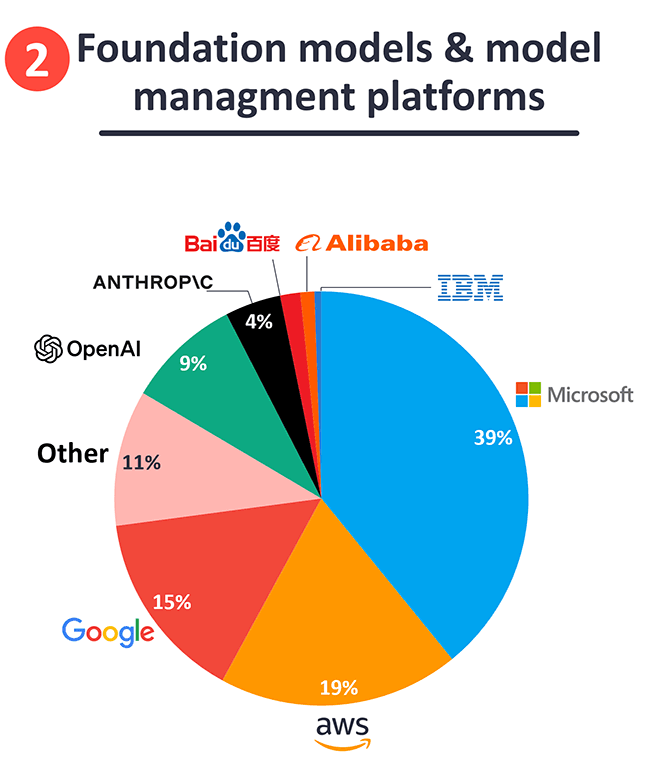

Battling the Giants, Growing Even Quicker: Competitive Environment in Turmoil

Microsoft’s advantage in the hyperscaler competition is not in model or computing capacity but in end-to-end platform utility. Amazon Web Services is still in the number one spot in absolute share in the cloud but falls behind in enterprise productivity penetration and hybrid cloud flexibility. Azure, an integral part of Microsoft’s software environment, is the default option among enterprises looking for vertical integration, from Office to Azure to Dynamics.

Google Cloud, while technologically sophisticated, is afflicted by fragmentation. Its AI products are strong in concept but don’t always translate into commercial success at scale. Microsoft’s strategic partnership with OpenAI, on the other hand, allows it to dominate enterprise-ready AI applications’ time-to-market. Its head-start advantage with tools such as Copilot is driving adoption across industries, from finance to education.

Newcomers like Oracle or cost disruptors like CoreWeave and Nebius may bring niche benefits, specifically in AI-specific infrastructure pricing. They don’t have Microsoft’s software-native differentiation or long-term customer relationships, though. Microsoft’s approach is not merely to rent computing capacity, it is to provide quantifiable productivity benefits layered across its platforms. This bundling power is particularly effective in enterprise deals, where AI improvements can command greater contract values without competing solely on infrastructure price.

Microsoft's moat is not established on any one AI model or GPU cluster, though. It's the architectural gravity it has created, where AI, cloud, security, and productivity all meet, and switching costs are prohibitively expensive.

Source: Statista

Efficiency as Leverage: Growth, Profitability, and Strategic Scaling

Microsoft’s Q3 results highlight a company firing on all cylinders. Revenue climbed 13% to $70.1 billion. Operating income grew 16% to $32 billion, and EPS surged 18% to $3.46. What stands out, however, is the margin performance in the face of aggressive CapEx. Gross margin dollars rose over $4.8 billion year-over-year, while operating margin held steady despite $21 billion in capital expenditures, nearly 2x the run-rate from just two years ago.

CapEx has been front-loaded to fund AI infrastructure buildout, but management noted that almost half of those investments were in long-duration assets with 10-15-year horizons to break even. Microsoft has condensed the timeframe from deployment to monetization of GPUs, a transformation facilitated by software-level optimizations and customer commitment pipelines already more than $300 billion in multi-year commitments in the cloud.

Cash is still a stronghold. Free cash flow in the quarter was $20.3 billion, and it returned $9.7 billion through dividends and share repurchases. Notably, Microsoft has strategic optionality remaining, trading off shareholder returns against high-ROI reinvestment. Its AI ramp is not speculative; it's monetizing through current enterprise avenues and building long-term optionality in resale infrastructure, security, and analytics.

Business unit margins are still healthy. Productivity contributed 58% operating margin, Intelligent Cloud 41%, and More Personal Computing 26%. Significantly, the cloud segment’s gross margin did suffer slightly due to AI infrastructure drag, but this was offset by efficiency in non-AI workloads and software orchestration improvements. This margin dance supports Microsoft’s advantage in navigating CapEx-intense transitions without sacrificing profitability.

Source: Q3-Deck

Discounted Dominance? Target Price Range and Valuation Insights

Despite its leadership role, Microsoft is suffering from a market-level perception of its valuation. Microsoft is trading with the current price of 32x forward P/E, 21x forward EV/EBITDA, and 12x forward EV/Sales. These are above the industry median by significant margins, P/E by about ~61%, and EV/Sales by more than 300%, but don’t reflect Microsoft’s capital efficiency, margin resilience, and AI leverage.

Legacy PEG ratios indicate a premium, with PEG (GAAP) standing at 2.76 compared with a sector median of 0.74. This difference closes significantly, though, if one normalizes for Microsoft’s return on invested capital of 30%+, long-duration revenue visibility, and value embedded in its AI platform. Meanwhile, several "cheaper" tech competitors struggle with greater customer churn, diminished pricing power, and softer operating leverage.

Compared with its peers Amazon and Google, Microsoft's premium is very justified. Amazon has similar multiples with lower margins and greater retail exposure. Google is still attractive, but without the software monetizing layers of Microsoft. Nvidia, while accelerating on AI GPU demand, is trading at an EV/Sales of 34x and has cyclical headwinds that Microsoft can avoid due to its subscription SaaS model.

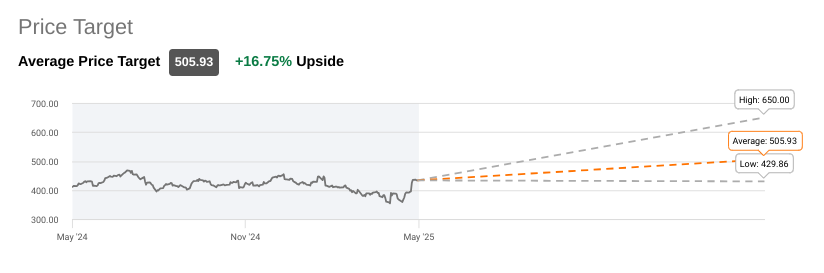

A blended fair value approach utilizing a 24x FY26E EBITDA multiple (around ~$130B annualized), pro forma adjusting for ~$80B in net cash, yields a fair value of approximately $417 per share. A more optimistic scenario, where Microsoft successfully ramps up Copilot penetration, continues momentum on AI monetization, and stabilizes cloud margins, will support a price target of between $460–$480 per share in the next 12–18 months near analysts’ price target.

The stock is priced at $435 per share, and it is trading towards the high point of historical valuations but below what may be justified by its long-term earnings strength and infrastructure compounding potential.

Source: SeekingAlpha

Risks: Regulatory Scrutiny, Monetization Lag, and AI Saturation

Microsoft's fundamental threats are predominantly macro-structural. Regulatory pressure regarding AI, data usage, and platform dominance is rising across the world. Any antitrust push or forced unbundling, particularly around Azure and Microsoft 365, may compress margins and delay adoption. There is also timing risk: while Copilot and Azure AI are scaling, monetization may lag behind infrastructure expenditures, compressing margins in the near term.

Over-reliance by customers on third-party AI models like those constructed on OpenAI may dilute Microsoft's proprietary moat if not balanced with in-house innovation. Also, saturation in corporate AI spending or variation with productivity benefits from LLMs may slow down the uplift in ARPU, particularly in tail-end adoption curves. Finally, there is an execution risk that is not inconsequential. Microsoft is pursuing AI, gaming, infrastructure, and core software, all concurrently. A misalignment in these vectors may result in margin disparity or strategic dilution.

Source: IOT-analytics

Conclusion:

Microsoft is not only scaling quicker, it’s scaling better. With an AI-fueled flywheel across SaaS, infrastructure, and productivity, it provides monetization depth and strategic resilience few rivals match. Overvaluation concerns apart, Microsoft is a structurally advantaged compound built with the capacity to deliver long-duration returns.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.