Dollar Slumps to Four-Year Low, Trump Still Says ‘Dollar Is Doing Great’?

AI Podcast

The U.S. dollar is experiencing its most significant sell-off in years, amplified by President Trump's comments suggesting approval of a weaker dollar, which he claims to influence. This, combined with policy uncertainty, Fed independence concerns, rising deficits, and political polarization, fuels dollar depreciation. Speculation of U.S.-Japan currency intervention, indicated by Fed inquiries, has further pressured the dollar and strengthened the yen. Consequently, major currencies like the euro, pound, and franc have seen significant gains, driven by perceived "anti-dollar" sentiment and concerns over U.S. fiscal sustainability and policy unpredictability.

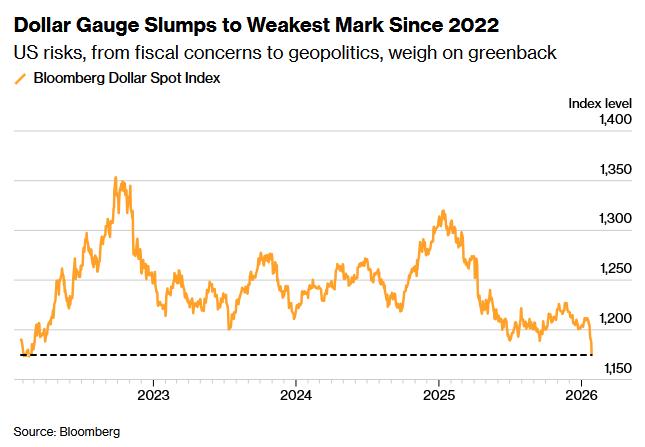

TradingKey - The U.S. dollar is facing its most aggressive sell-off in nearly four years, with the Bloomberg Dollar Spot Index dropping Tuesday to its lowest level since March 2022.

Despite this, President Donald Trump struck an unusually optimistic tone during an event in Iowa. When asked about his concerns regarding a weakening dollar, “No, I think it’s great,” Trump said. “I mean, the value of the dollar. Look at the business we’re doing. No, the dollar’s doing great.”

He even suggested he has the power to influence the dollar's exchange rate, claiming, "I can make it go up and down like a yoyo."

The market generally believes that President Trump's remarks sent a clear signal that the U.S. government is condoning or even encouraging a weaker dollar, further prompting traders to ramp up selling pressure.

Win Thin, chief economist at Nassau Bank, said Trump's comments triggered a new round of dollar selling and could lead to further depreciation.

He noted that many officials within the Trump administration want to enhance the international competitiveness of U.S. exports by pushing down the dollar's exchange rate. However, he also warned that this is a risky choice. While a moderate devaluation can provide temporary economic stimulus, currency depreciation could trigger more severe financial instability once market confidence is lost.

In fact, market concerns over the continued weakening of the dollar stem not only from the president's remarks but also from a series of deep-seated, structural worries—high uncertainty in U.S. policy direction (such as the shocking plan to "take over Greenland"), potential risks of interference with Federal Reserve independence, expanding fiscal deficits and debt sustainability issues, and intensifying political polarization in the U.S.

James Lord, head of emerging market currency strategy at Morgan Stanley, stated that "unconventional catalysts are driving the dollar weaker" and that policy uncertainty is dampening investor interest in U.S. assets.

Expectations for Yen Intervention Heat Up; Global Currencies Strengthen Collectively

The recent sharp rise in the yen has become one of the key factors weighing on the dollar.

Last Friday, traders revealed that the Federal Reserve Bank of New York contacted several financial institutions to inquire about USD/JPY quotes. This move is typically seen as a preparatory step for intervention, sparking market speculation that the U.S. and Japan might conduct joint intervention in the currency market.

George Catrambone, head of fixed income at DWS Americas, pointed out that inquiries by Fed officials regarding the USD/JPY ( USD/JPY) exchange rate "pushed the dollar further down." Against this backdrop, the yen rebounded quickly, climbing as high as 152.43 against the dollar, a near three-month peak.

Japanese Finance Minister Satsuki Katayama stated after a Group of Seven (G7) meeting that the Japanese government will cooperate closely with the U.S. to take appropriate measures against exchange rate volatility if necessary. Her remarks further strengthened market expectations for joint intervention, supporting the yen's strong performance.

Meanwhile, continued dollar weakness is driving a broad rally in major global currencies.

On Tuesday, the euro ( EUR/USD) rose to $1.1990, its highest level since 2021; the British pound ( GBP/USD) rose 0.8% to $1.3791, also hitting a near three-year high; the Swiss franc ( USD/CHF) surged 1.4% to 0.7660 per dollar, a record of strength since 2015.

Analysts at Mitsubishi UFJ Financial Group (MUFG) said the euro is "benefiting from its role as the 'anti-dollar currency'" amid growing market concerns over U.S. policy prospects.

Policy Contradictions and Political Uncertainty Fuel Dollar Depreciation Expectations

Currently, market confidence in the U.S. policy environment continues to decline. Factors including rising skepticism over the Federal Reserve's independence, a widening federal budget deficit, lack of restraint in government spending, and growing domestic political polarization are collectively undermining market confidence in the stability of the dollar.

At the same time, Trump’s unpredictable decision-making style has further exacerbated these concerns. He has not only adopted an aggressive diplomatic stance toward overseas allies but has also made surprising statements regarding domestic fiscal, tax, and monetary policies. For instance, his remarks about "taking over" Greenland, though not implemented, highlighted the randomness and unpredictability of his diplomatic and economic strategy deployments.

Trump is set to decide on the next Federal Reserve chair, and there are widespread market fears that the new chair might adopt a more dovish stance, posing a challenge to currency stability.

Furthermore, domestic political instability in the U.S. continues to heat up, with the government facing the risk of another partial shutdown. Following the developments surrounding immigration enforcement in Minnesota, Senate Democrats have threatened to block funding bills unless an agreement is reached on funding for ICE (Immigration and Customs Enforcement). If a temporary funding deal is not extended by this Friday, the federal government could face a partial shutdown.

Kit Juckes, head of FX strategy at Societe Generale, pointed out that dollar bulls still face many risk factors, including the possibility of a government shutdown. "U.S. economic growth may still determine the extent of Fed easing, and thus whether the dollar will weaken significantly from current levels."

"Structural headwinds facing the dollar—declining confidence in U.S. trade and security policy, the politicization of the Fed, and deteriorating U.S. fiscal credibility—could offset a more neutral cyclical dollar backdrop and lead to further declines," said Elias Haddad, head of global markets strategy at Brown Brothers Harriman.

Debt Risks Dampen Market Confidence

Although U.S. Treasury yields have risen recently and the market widely expects the Federal Reserve to keep interest rates unchanged at its upcoming policy meeting—two factors usually seen as supporting a stronger dollar—the dollar has continued to weaken lately.

Max Wasserman, co-founder and senior portfolio manager at Miramar Capital, noted that current contradictory U.S. policies are worrying markets. He said the U.S. wants to stimulate the economy with significant rate cuts on one hand, while the fiscal deficit grows larger on the other. "We’re talking about a government that wants to cut rates substantially, while at the same time, the deficit is increasing."

He further pointed out that, contrary to U.S. fiscal expansion, other troubled nations also facing high debt are now becoming more cautious. They may avoid rate cuts and pivot toward improving fiscal and monetary policy structures to maintain long-term economic stability.

The current U.S. federal debt has exceeded $38 trillion, a record high, driven by long-term fiscal deficits, previous tax cuts, and massive emergency spending required for various crises. Since Trump's return to the political stage last year, he has repeatedly called for the Fed to cut interest rates to lower borrowing costs and drive economic expansion.

However, long-term U.S. rates remain high, particularly the 30-year Treasury yield, reflecting unabated investor concerns over persistent inflation and fiscal sustainability. Wasserman stated bluntly: "We’re not showing any real fiscal responsibility in the world markets. In fact, we’re doing the exact opposite."

Meanwhile, options market data further confirms that expectations for future dollar weakness are intensifying. According to Bloomberg data, the premium on short-term option contracts betting on dollar depreciation has risen to its highest level since records began in 2011, and bullish bets on other major currencies have also hit multi-month highs, close to market conditions seen after Trump introduced tariffs last April.

Bloomberg strategist Mark Cranfield stated that a significant increase in options trading volume for G10 currencies this week indicates that the theme of dollar depreciation is gaining traction among more investors. He noted: "Huge volumes in G-10 currency options this week support the view that the dollar-depreciation theme is gaining momentum among investors. Regardless of whether the Fed's exchange rate inquiries mark the beginning of a so-called 'Mar-a-Lago Agreement,' macro traders are making their own judgment that the dollar is on a downward path."

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.