What to Expect From the U.S. July CPI Report: Stalled Tariff Repricing Eases Inflation Fears and Supports Equities in August

TradingKey - On Tuesday, August 12, the U.S. Bureau of Labor Statistics will release the July Consumer Price Index (CPI) report — a key data point that could shape Federal Reserve policy and influence the trajectory of U.S. equities during what Wall Street calls the historically weak “dangerous August.”

Analysts expect the report to show that Trump’s tariffs are feeding into inflation, but slowing wage growth and softening demand may limit pricing power, potentially reducing the severity of a seasonal market correction.

CPI Forecasts

According to FactSet, consensus estimates are:

- Headline CPI MoM: +0.2%, down from +0.3% in June

- CPI YoY: +2.8%, up from +2.7%

- Core CPI (ex-food and energy) MoM: +0.3%, the highest since February 2025, up from +0.2%

- Core CPI YoY: +3.0%, up from +2.9%

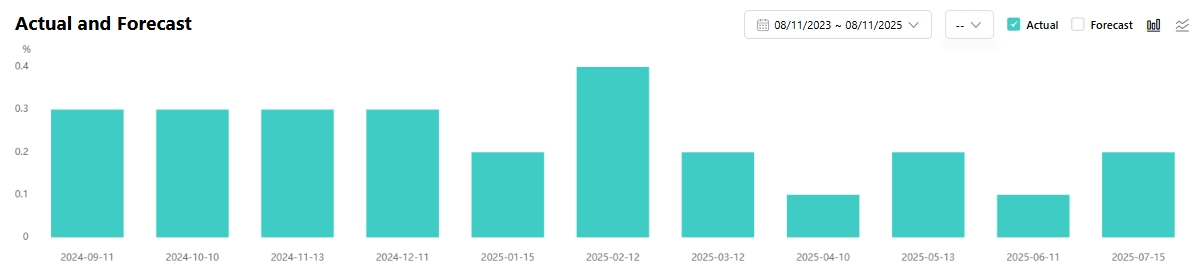

U.S. Core CPI Monthly Change, Source: TradingKey

Tariff Impact: Gradual

June’s CPI already showed early signs of tariff pass-through in goods like toys, furniture, and appliances. For July, the focus is on whether companies can continue to raise prices.

Goldman Sachs projects:

- New vehicle prices: -0.2%

- Used vehicles: +0.75%, adding 0.02 points to core CPI

- Household and recreational goods: Due to tariffs, these categories could add 0.12 points to core CPI

Most economists agree the full impact will be gradual. The U.S. now has an average goods tariff rate of 15%, but the effective rate (based on import data) is only 9–10%. JPMorgan thus expects year-end CPI inflation to reach 3.0–3.5%, with core CPI at 3.5–4.0%, as inventory cycles amplify tariff effects.

UBS economists believe the July report could mark the start of a multi-month inflation uptick, with core CPI rising to 3.5% by year-end.

But Economic Slowdown May Cap Inflation

Despite rising costs, weaker demand could limit companies’ ability to pass on higher prices.

Jason Tang, Senior Economist at TradingKey, said:

“Despite signs of inflation picking up recently, reduced economic growth should limit demand-driven inflation increases. As a result, we anticipate inflation will steadily decrease in the coming months.”

Key inflation drivers for July:

- Food prices: Rising due to supply chain pressures

- Transportation Goods: Used car auction prices are rebounding

- Housing: Rent inflation remains sticky

- Energy: Falling oil prices will offset some gains

Bloomberg analysts highlight a critical factor: household disposable income growth has slowed sharply — now just one-third of its pandemic peak.

Combined with the 258,000 downward revision in nonfarm payrolls, real income likely contracted in June.

Even if July retail sales come in strong, analysts warn against overinterpreting it as resilient consumer demand.

While goods inflation rises, services inflation continues to decline — a positive sign for the Fed. JPMorgan emphasizes this divergence: services sector inflation has been slowing, but if services inflation starts rising, however, this could be a sign that inflation is a stickier problem.

Fed Poised for Dovish Shift?

Last week, President Trump nominated Stephen Miran, Chair of the White House Council of Economic Advisers, to fill a vacant Fed governor seat. Miran, a key architect of the Mar-a-Lago Accord, believes tariffs have limited impact on inflation and views Trump’s economic policies as “disinflationary”.

His appointment could tilt the Fed toward earlier and more aggressive rate cuts.

JPMorgan updated its forecast last week, now expecting four consecutive 25-basis-point cuts starting in September.

Will the “Dangerous August” Be Less Dangerous?

Historically, August and September are the worst months for the S&P 500. Over the past 35 years, the index has averaged a 0.6% loss in August and 0.8% in September.

Morgan Stanley and Deutsche Bank have warned of a 5–10% pullback in Q3. But several factors may soften the blow, including rising odds of Fed rate cuts, solid corporate earnings, greater clarity on trade policy and easing inflation pressures.

Edward Jones strategists said:

“If the CPI suggests that the market got a little ahead of itself, that can create volatility. But if it's not worse than feared ... that can further reinforce that we are now in an inflection point for the Fed.”

Alexis Deladerrière, Analyst at Goldman Sachs Asset Management, noted that we are now in a situation where not everything is clear, but enough is clear for businesses to make decisions around hiring, investing and repositioning their supply chains to help protect their profit margins.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.