China July Inflation Commentary: CPI Exceeds Expectations

TradingKey - On 9 August 2025, China's National Bureau of Statistics released inflation data for July. The Consumer Price Index (CPI) rose by 0.4% month-on-month, reversing the previous month's 0.1% decline, while remaining unchanged year-on-year. Core CPI increased by 0.8% year-on-year. The Producer Price Index (PPI) fell by 0.2% month-on-month, with the decline narrowing by 0.2 percentage points compared to the previous month, and decreased by 3.6% year-on-year, consistent with the previous month's decline.

The improvement in China's inflation situation is primarily driven by the sustained effectiveness of policies aimed at expanding domestic demand and promoting consumption, coupled with the continued deepening of the national unified market and intensified efforts to address "involution" among enterprises. Regarding CPI components, food prices showed a downward trend, with eggs, pork, and vegetables being the main factors dragging prices down. Influenced by earlier increases in international oil prices, domestic energy prices in China rose in July. Since the beginning of the year, core CPI has continued to recover, driven primarily by rising service prices and industrial consumer goods prices excluding energy. With the ongoing strengthening of "anti-involution" policies, the year-on-year decline in PPI did not widen in July, and the month-on-month decline also narrowed.

Looking forward, we anticipate that the intensifying impact of "anti-involution" measures will gradually lead to a recovery in PPI prices. As this unfolds, the upward trend in PPI prices will gradually transfer to CPI, aiding China in addressing the risk of low inflation.

Main Body

On 9 August 2025, China's National Bureau of Statistics released inflation data for July. The Consumer Price Index (CPI) increased by 0.4% month-on-month, rebounding from a 0.1% decline the previous month, while remaining unchanged year-on-year. Core CPI rose by 0.8% year-on-year. The Producer Price Index (PPI) fell by 0.2% month-on-month, with the decline narrowing by 0.2 percentage points compared to the prior month, and dropped by 3.6% year-on-year, consistent with the previous month's decline (Figure 1). Overall, the improvement in China's inflation environment is largely due to the sustained impact of policies promoting domestic demand and consumption, alongside the continued deepening of the national unified market and intensified efforts to address "involution" among enterprises.

Figure 1: Market Consensus Forecasts vs. Actual Data

Source: Refinitiv, TradingKey

Analysing CPI components, food prices exhibited a downward trend, with eggs, pork, and vegetables being the primary factors contributing to the decline. Specifically, egg prices fell month-on-month due to high inventory levels and ample market supply. For pork, although prices rose month-on-month, driven by the Ministry of Agriculture and Rural Affairs guiding leading enterprises to rationally reduce production capacity and adjust slaughter schedules, they remained significantly below historical averages for the same period. Vegetable prices, affected by high temperatures and heavy rainfall, which constrained growth and increased preservation costs, saw a month-on-month increase; however, like pork, they were also well below historical averages for the same period.

The primary driver of rising energy prices was the increase in oil prices. Due to earlier gains in international oil prices, domestic refined oil prices were adjusted upward on 1 July. Although a slight downward adjustment occurred on 15 July, the reduction was minimal, and overall, oil prices maintained an upward trend in July.

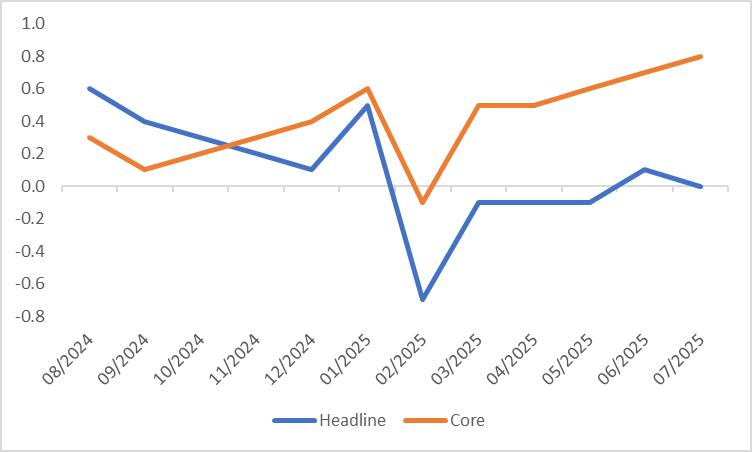

Since the beginning of 2025, core CPI has shown a steady upward trend (Figure 2). This increase is primarily driven by rising service prices and non-energy industrial consumer goods prices. In the service sector, the arrival of the summer vacation period has boosted consumer demand for travel, entertainment, and related services, leading to significant price increases for airfares, tourism, hotel accommodations, and vehicle rental fees. In the non-energy industrial consumer goods sector, the end of the "618" promotional event led to a rebound in durable goods prices, with notable increases in the prices of household appliances, communication devices, and vehicles.

Figure 2: China CPI (%, y-o-y)

Source: Refinitiv, TradingKey

The sixth meeting of the Central Financial and Economic Affairs Commission on 1 July and the Political Bureau meeting held at the end of July both highlighted "anti-involution" as a key agenda item. The related measures focused on three main areas: "curbing disorderly competition among enterprises", "regulating production capacity in key industries", and "standardising local government investment attraction practices".

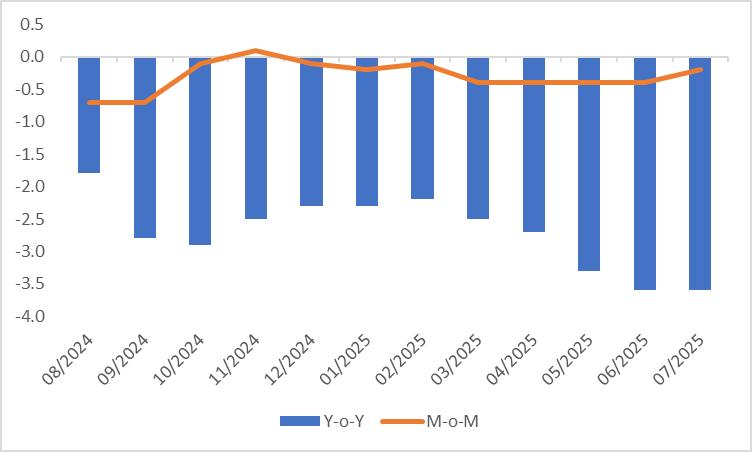

With the ongoing strengthening of "anti-involution" policies, the year-on-year decline in PPI did not widen further in July, and the month-on-month decline also narrowed (Figure 3). Specifically, in the means of production sector, the mining industry saw a year-on-year decline of 14 percentage points, with the drop expanding further compared to previous periods. Meanwhile, the year-on-year declines in the raw materials and processing industries slightly narrowed. In the consumer goods sector, the year-on-year decline for durable goods widened, while the decline for food items slightly contracted.

Figure 3: China PPI (%)

Source: Refinitiv, TradingKey

Looking forward, we anticipate that the intensifying impact of "anti-involution" measures will gradually lead to a recovery in PPI prices. As this unfolds, the upward trend in PPI prices will gradually transfer to CPI, aiding China in addressing the risk of low inflation.

China July Inflation Preview: Low Inflation Risks May Ease

TradingKey - On 9 August 2025, China's National Bureau of Statistics will release July inflation data as scheduled. The market widely expects the Consumer Price Index (CPI) for July to shift from June’s 0.1% year-on-year increase to negative growth. The Producer Price Index (PPI) is projected to record a year-on-year decline of -3.2% in July, showing an upward trend compared to June’s figure. We concur with these market expectations.

The primary factors influencing July’s inflation data stem from “anti-involution” measures. Against this backdrop, consumer goods prices are expected to maintain some support. Meanwhile, with the arrival of the summer season, the holiday economy is likely to drive a surge in tourism and travel, boosting service consumption demand. However, there are counterbalancing pressures: downward price trends in food (particularly vegetables and pork) and energy are expected to offset the upward factors, potentially leading to a 0.1% year-on-year decline in the CPI. Concurrently, as “anti-involution” policies intensify, the decline in factory-gate prices is likely to narrow. The PPI is projected to improve from June’s year-on-year drop of -3.6%, reaching -3.2% in July.

Looking ahead, we anticipate that as the effects of “anti-involution” policies deepen, the PPI will gradually show signs of recovery. During this process, the upward momentum in PPI prices is expected to progressively transmit to the CPI, helping China mitigate the risk of low inflation.

Main Body

On 9 August 2025, China's National Bureau of Statistics is scheduled to release inflation data for July. The prevailing market view suggests that the Consumer Price Index (CPI) for July will shift from a 0.1% year-on-year increase in June to negative growth. Meanwhile, the Producer Price Index (PPI) is expected to record a year-on-year decline of -3.2% in July, reflecting an improvement compared to June’s figure (Figure 1). We align with these market expectations.

Figure 1: Consensus Forecasts

%20(1).jpg) Source: Refinitiv, TradingKey

Source: Refinitiv, TradingKey

The primary drivers of July’s inflation data are tied to “anti-involution” policies. Specifically, the sixth meeting of the Central Financial and Economic Affairs Commission on 1 July outlined a clear roadmap for implementing policies to address “comprehensive management of involutionary competition”. The meeting emphasised measures such as “regulating enterprises’ disorderly low-price competition following laws and regulations and promoting the orderly exit of outdated production capacity”. Following this, multiple government departments took successive actions to tackle “involution” issues in the market. At the end of July, the Political Bureau meeting further underscored the importance of “anti-involution” efforts, focusing on three key areas: “governance of disorderly corporate competition”, “capacity regulation in key industries”, and “standardisation of local government investment attraction practices”.

Under the current “anti-involution” policy framework, prices of consumer goods are expected to retain some support. Additionally, with the onset of the summer season, the holiday economy is likely to spur a peak in tourism and travel, thereby boosting service consumption demand. However, counteracting factors are also at play: due to a high base effect from the previous year, China’s vegetable price index is projected to shift from positive to negative growth. In the pork market, sustained high hog production capacity, combined with warmer weather potentially accelerating slaughter rates, is expected to maintain a pattern of “strong supply and weak demand”, leading to a decline in pork prices. Overall, downward pressure on food prices, coupled with a marginal retreat in fuel prices, is likely to offset upward factors. Consequently, we forecast a 0.1% year-on-year decline in the CPI for July (Figure 2).

Figure 2: China CPI (%, y-o-y)

.jpg) Source: Refinitiv, TradingKey

Source: Refinitiv, TradingKey

Against the backdrop of intensifying “anti-involution” policies, the decline in factory-gate prices is likely to gradually narrow. According to July’s PMI sub-indices, the purchase price index and the ex-factory price index rose by 3.1 and 2.1 percentage points, respectively, compared to June. This shift suggests that the year-on-year decline in the PPI may improve from -3.6% in June to an estimated -3.2% in July (Figure 3).

Looking forward, we assess that as the effects of “anti-involution” policies continue to deepen, PPI prices will gradually show signs of recovery. This upward momentum in PPI prices is expected to progressively transmit to the CPI, helping China mitigate the risk of low inflation.

Figure 3: China PPI (%, y-o-y)

.jpg) Source: Refinitiv, TradingKey

Source: Refinitiv, TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.