U.S. Payrolls Rebound Masks Cooling Labor Market as Unemployment Hits Four-Year High

AI Podcast

The U.S. labor market in November 2025 showed mixed signals: non-farm payrolls increased by 64,000, exceeding forecasts, but the unemployment rate unexpectedly rose to 4.6%. Wage growth also slowed to 3.5% year-over-year. Concerns exist over potential data distortions due to a government shutdown, with some analysts suggesting actual job growth might be near zero. While the report is unlikely to prompt immediate Fed rate cuts, continued weakness could accelerate easing. Market interpretations varied, with futures showing cautious optimism. Future data will determine the Fed's policy trajectory.

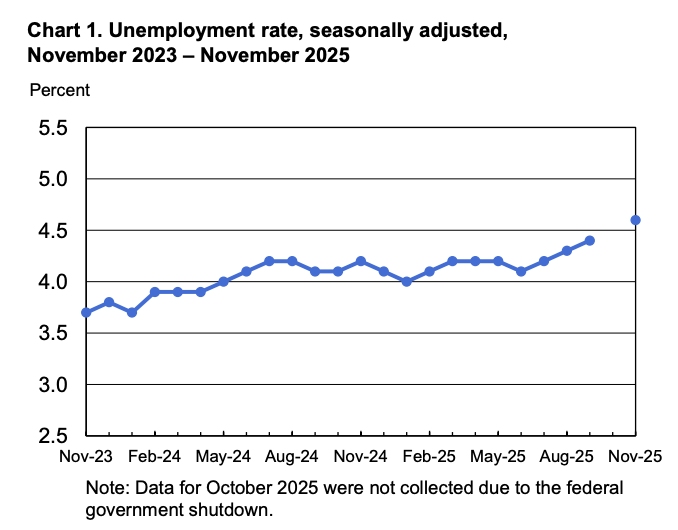

TradingKey – The U.S. labor market delivered a mixed message in November 2025, with job growth topping estimates but unemployment surging to a multi-year high. Non-farm payrolls increased by 64,000, slightly surpassing the market forecast of 50,000 and ending the significant negative growth of the prior month. However, the unemployment rate unexpectedly jumped to 4.6%, the highest level recorded since September 2021.

Market observers noted that while the report averted the worst-case scenario, the clear cooling trend in the labor market introduces new variables for the Federal Reserve's rate-cutting path.

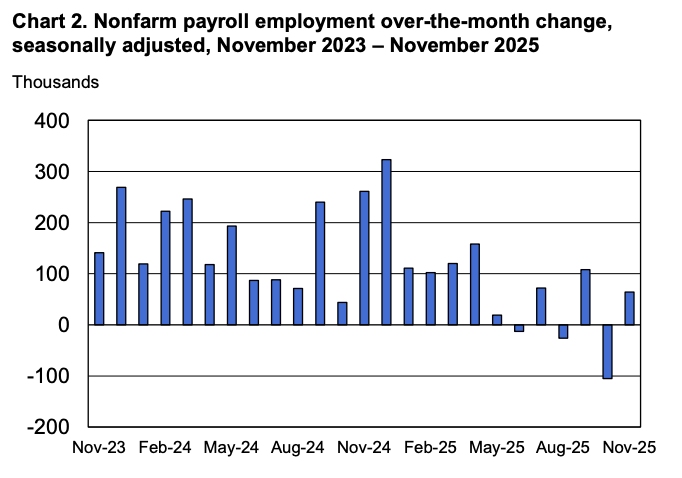

The core positive signal from the report stemmed from a modest rebound in the private sector, which added 69,000 jobs in November. However, the underlying concerns within the report drew more attention, as the unemployment rate surged from 4.4% in the previous month to 4.6%.

【U.S. Unemployment Rate Hits New Multi-Year High in November, Source: BLS】

Further amplifying these concerns is the deterioration in employment structure. An industry breakdown reveals that new jobs were primarily concentrated in healthcare, construction, and social assistance, reflecting continued labor absorption in service-oriented and infrastructure-related sectors. Conversely, federal government employment saw sustained declines, with a cumulative reduction of approximately 168,000 positions in October and November, significantly dragging down the overall labor market performance.

【U.S. Employment Rebounds, Source: BLS】

Wage growth also slowed notably, with average hourly earnings year-over-year growth falling to 3.5% in November, its lowest since May 2021. With inflation not yet fully subdued, weakening real wage growth could curb consumer spending among middle-to-lower income groups, thereby exacerbating downside risks to the economy.

Data Distortion Issues constituted another significant uncertainty in this report. The U.S. government shutdown led to reduced survey response rates and unusual weight adjustments, prompting the Bureau of Labor Statistics (BLS) to use a two-month analysis period with higher-than-usual standard errors. Federal Reserve Chair Jerome Powell had previously warned that non-farm payroll data might systematically overstate monthly job gains by approximately 60,000.

If this bias were excluded, actual job growth since May of this year could be near zero or even negative. This implies the labor market might already be in a hidden recession, far more severe than the surface numbers suggest.

Wall Street's interpretation of the report was divided, but the prevailing view leaned towardscautious optimism.

Krishna Guha, Head of Global Policy and Central Bank Strategy at Evercore ISI, opined that the data's weakness was insufficient to prompt the Federal Reserve to restart rate cuts in the short term, stating that onlyreadings significantly below expectationswould trigger more aggressive action.

Capital Economics economist Stephen Brown also commented that the report was "not enough for the Federal Open Market Committee to consider rate cuts at its next few meetings."

Nick Timiraos, widely considered the Fed's unofficial mouthpiece, offered a more balanced assessment: current hiring weakness is sufficient to support Powell's recent push for three rate cuts, but it hasn't deteriorated enough to necessitate action in January, particularly given thenoise stemming from the government shutdown.

Some analysts, however, adopted a moredovish stance.

Joe Brusuelas, Chief Economist at RSM, indicated that the non-farm payroll data would likelybolster the Federal Reserve's dovish faction. He noted that in the later stages of an economic cycle, the BLS often overestimates employment, subsequently revising initial figures downwards through benchmark revisions. If January's data continues to show weakness, the door for rate cuts would open rapidly.

From a deeper analytical perspective, thismixed non-farm payroll reportreflects a U.S. economy at a critical turning point.

The Federal Reserve has already implemented three consecutive rate cuts, guidingrates into a neutral range, aimed at preventing excessive weakness in the labor market. Powell has repeatedly stressed that the policy objective is to achieve stable unemployment or, at most, a slight increase of one to two tenths of a percentage point.

However, downside risks are accumulating: if job losses in manufacturing and government sectors spread, combined with slowing wage growth and deteriorating job quality, it could trigger a chain reaction in consumption and investment, leading to a further deceleration in growth.

While resilience in certain areas of the private sector provides a buffer, the structural issues within the employment composition cannot be ignored. Furthermore, the displacement effect of AI technology on middle and low-skilled jobs may become more evident in the coming months, therebyamplifying hiring caution. If the December jobs report fails to provide a"noise-free" signal of stabilization, another upward surge in the unemployment rate is not impossible, at which point the Federal Reserve might beforced to accelerate its easing paceto avert a hard landing.

Market reactions also reflected this uncertainty. Following the report's release, U.S. equity futures turned positive in pre-market trading, with the technology sector leading the rebound, while 10-year Treasury yields pulled back slightly, indicating investors were wavering between defensive positioning and risk appetite.

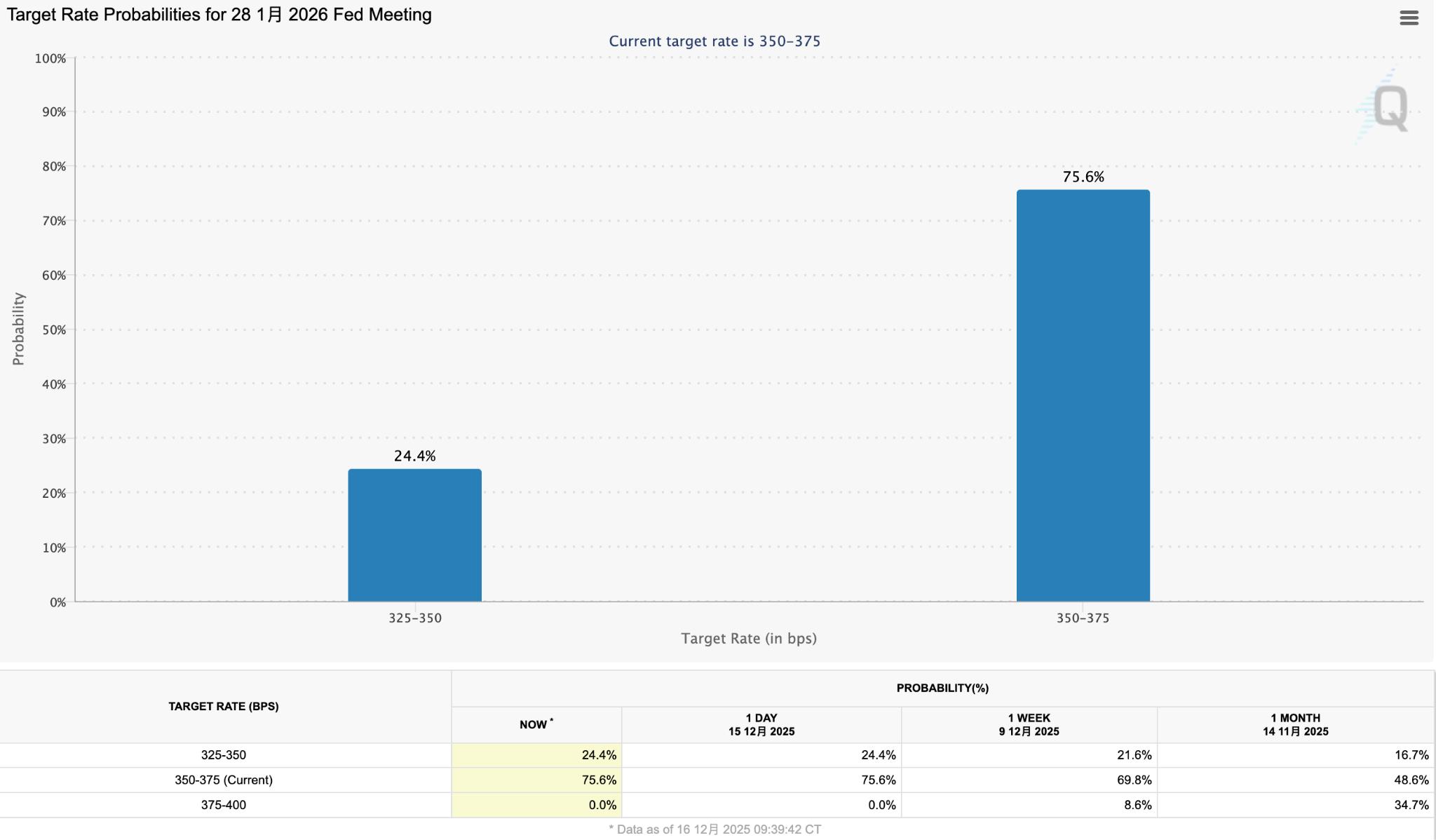

【Probability of January Rate Cut, Source: cmegroup.com】

CME Group's FedWatch Tool indicated that the probability of a January rate cut remained around 25%, a slight increase from the previous day.

Goldman Sachs strategist Chris Hussey noted that investors' interpretations of the data diverged, with falling bond yields signaling defensive postures, while the strength in tech stocks might suggest the market is betting on easing prospects.

Overall, while November's non-farm payroll data showed a modest improvement, it largely failed to mask the underlying cooling in the labor market. It provides the Federal Reserve room for gradual easing but is insufficient to pinpoint the timing of the next rate cut.

Market attention will now focus on the December and January employment readings, which will serve as a decisive test. If private sector hiring continues to stabilize, the Fed might opt to observe, prioritizing a sustained return of inflation to target. Conversely, if the unemployment rate rises further or job gains remain sluggish, rate cut expectations will quickly escalate.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.