U.S. April CPI Preview: Weaker-Than-Expected Inflation to Boost U.S. Stocks

TradingKey - Market consensus forecasts the April Headline CPI year-over-year (YoY) growth at 2.4%, unchanged from March. However, our analysis of leading indicators across CPI components suggests that April inflation will come in below this consensus estimate. This could increase the likelihood of the Federal Reserve resuming its rate-cutting cycle in June. As a result, we expect U.S. stocks to rise, while the U.S. dollar index and Treasury yields decline following the data release.

Source: Refinitiv, TradingKey

On 13 May 2025, the U.S. will release its April Consumer Price Index (CPI) data. The market widely anticipates the Headline CPI month-over-month (MoM) growth to turn positive, rising to 0.3% from March’s -0.1%, resulting in a YoY increase of 2.4%, flat compared to the previous month (Figure 1). However, we believe April inflation will fall short of this consensus expectation.

Figure 1: Consensus Forecasts

Source: Refinitiv, TradingKey

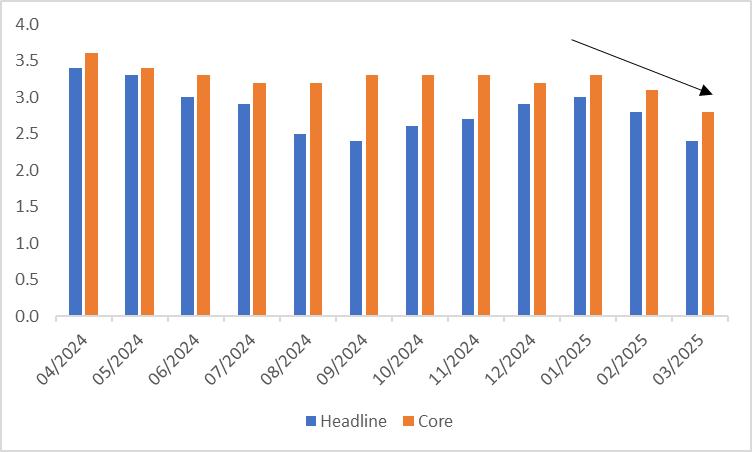

In March, U.S. inflation cooled significantly, with both Headline and Core CPI recording their smallest annual increases in the past year (Figure 2). Despite this, many economists and investors expect inflation to rebound, primarily due to high tariffs driving up imported goods prices. Jeffrey Gundlach, dubbed the “New Bond King”, has warned that inflation could rise, potentially pushing the U.S. CPI above 4% by year-end.

Figure 2: CPI (y-o-y, %)

Source: Refinitiv, TradingKey

Our assessment of April CPI trends is based on leading inflation indicators:

· The CRB Food Index’s YoY growth surged in April, likely driving further increases in the CPI food component.

· U.S. retail gasoline prices continued to decline YoY, suggesting a probable decline in the energy goods component.

· A slight drop in the Manheim Used Car Price Index indicates limited upward pressure on the transportation component.

· Weakening S&P CoreLogic Case-Shiller Home Price Index and Zillow Rent Index signal a slowdown in housing-related inflation.

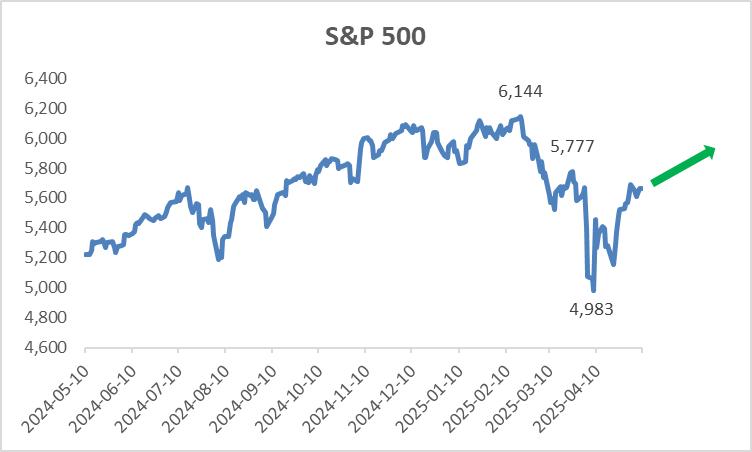

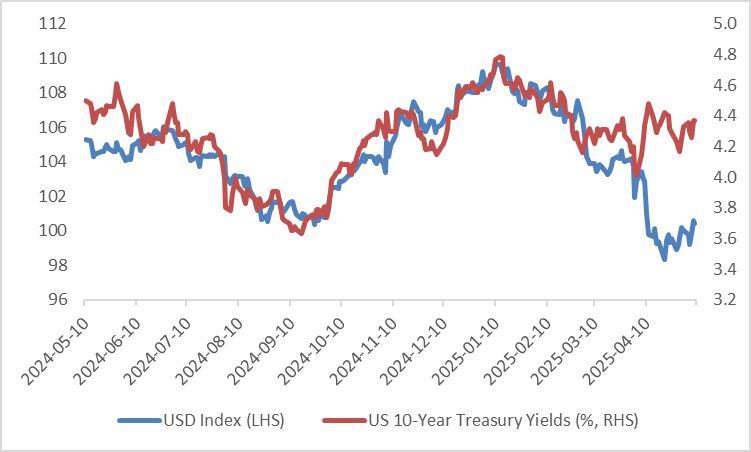

Among the four major CPI components, only food shows upward momentum, but it accounts for just 13.7% of the overall CPI. We expect April CPI to undershoot market expectations, increasing the odds of the Fed restarting rate cuts in June. Consequently, we anticipate U.S. stocks to rally, with the U.S. dollar index and Treasury yields declining post-release.

Figure 3: USD Index and U.S. 10-Year Treasury Yields

Source: Refinitiv, TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.