Lam Research Corp Stock (LRCX) Moved Up by 3.28% on Mar 10: A Full Analysis

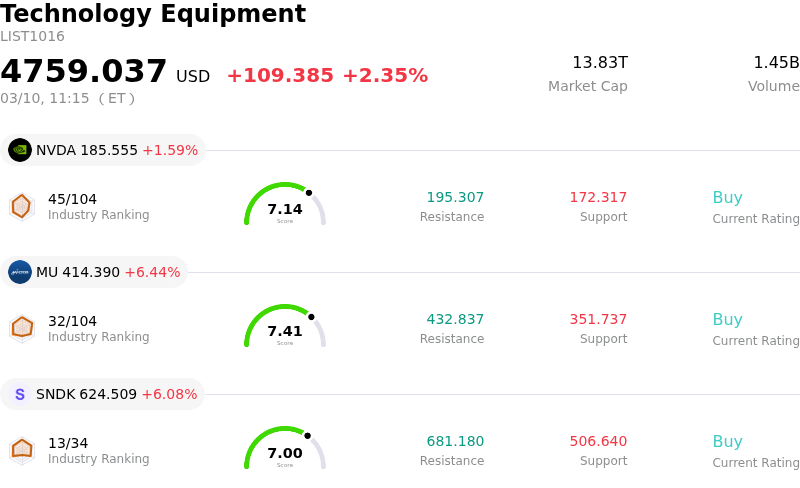

Lam Research Corp (LRCX) moved up by 3.28%. The Technology Equipment sector is up by 2.35%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 1.59%; Micron Technology Inc (MU) up 6.44%; SanDisk Corporation (SNDK) up 6.08%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research experienced an upward movement in its share price today, primarily driven by robust company fundamentals, optimistic analyst sentiment, and favorable industry tailwinds in the semiconductor sector.

The company's recent financial performance has been strong, with fiscal second-quarter 2026 results surpassing both revenue and earnings expectations. Management further bolstered investor confidence by providing optimistic guidance for the third quarter of 2026, projecting healthy revenue and earnings per share. This strong operational execution, including annual revenue growth and healthy operating margins, signals effective management and efficient processes. The recent announcement of a quarterly dividend also indicates financial health and a commitment to returning capital to shareholders.

Analyst forecasts have significantly contributed to the positive sentiment. Numerous analysts maintain a strong positive outlook, issuing "Buy" or "Strong Buy" ratings and revising earnings per share estimates upwards. Specifically, Barclays raised its price target for Lam Research today, following similar actions by other firms in recent months. The consensus among analysts suggests significant potential for appreciation, with many recommending the stock.

Moreover, the broader industry dynamics, particularly the surging demand for artificial intelligence (AI) infrastructure, are creating a highly favorable environment for Lam Research. The global Wafer Fab Equipment (WFE) market is anticipated to experience substantial growth in 2026, largely fueled by the AI boom, with projections reaching $135 billion. Lam Research is strategically positioned to capitalize on this expansion due to its leadership in critical areas such as advanced packaging, deposition, and etch capabilities, which are essential for AI-related technology transitions. The company has also seen strong demand in the memory sector, with DRAM revenue rising significantly, driven by advanced technologies. Global semiconductor sales recorded strong year-over-year growth in January 2026, indicating the overall industry is entering a robust growth cycle driven by AI demand.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [2.89], indicating a neutral signal. The RSI at 42.84 suggests neutral condition and the Williams %R at -72.73 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $270.22, a high of $325.00, and a low of $116.32.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Escalating geopolitical tensions in the Middle East are increasing liquefied natural gas (LNG) prices, potentially leading to higher operating costs for key South Korean semiconductor fabrication plant customers and indirectly impacting demand for Lam Research's equipment.

- The company faces ongoing scrutiny from the US House Select Committee on the CCP regarding its sales practices in China, coupled with a projected decline in revenue contribution from China due to export controls.

- Recent regulatory filings indicate significant institutional selling pressure, including planned sales by Fidelity Brokerage Services LLC, and a director's reduction of their stake by over 12% within the last 72 hours, potentially signaling cautious insider sentiment.

- Analyst valuation models suggest that the stock may be significantly overvalued, with GuruFocus estimating a potential downside of over 34%, and the company faces a negative outlook due to a decline in gross margin attributed to an unfavorable customer mix and reduced revenue from China.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.