TradingKey’s The Week on Wall Street: S&P 7,000 Breakthrough, Q1 Earnings Surge, and Fed Rate Projections

AI Podcast

Geopolitical de-escalation regarding the Strait of Hormuz, following initial U.S.-Iran tensions, propelled U.S. equities to new all-time highs. While energy prices initially surged, they sharply declined on a ceasefire. Economic data showed resilient labor markets and elevated inflation driven by energy costs. The Federal Reserve signaled prolonged higher rates. Despite market resilience, Navigen Wealth Management advises reducing U.S. equity exposure due to a negative intermediate-term trend. Key risks include ongoing Middle East instability and persistent inflationary pressures. Upcoming events include Retail Sales and an FOMC meeting.

Previous Week’s Market Review & Analysis

TradingKey - Macroeconomic Landscape: The week was significantly influenced by geopolitical tensions between the U.S. and Iran concerning the Strait of Hormuz. Early in the week, a fragile ceasefire collapsed, leading to a U.S. naval blockade and a surge in oil prices, creating market pressure. However, a ceasefire agreement and the subsequent reopening of the Strait later in the week caused WTI crude oil prices to fall sharply, dropping 9% to $83 per barrel. Economic data released included the March Producer Price Index (PPI), which rose 0.5% month-over-month and 4.0% year-over-year, with core PPI up 0.2% and 3.6% respectively, largely driven by energy prices. Import prices increased by 0.8%, below expectations. March 2026 Consumer Price Index (CPI) showed headline inflation reaching a two-year high due to a 21% surge in gasoline prices, while core inflation remained relatively stable. The U.S. labor market demonstrated resilience in March 2026, with nonfarm payrolls increasing by 178,000 and the unemployment rate at 4.3%. The Federal Reserve maintained its stance on interest rates, with expectations for prolonged higher rates due to elevated energy prices.

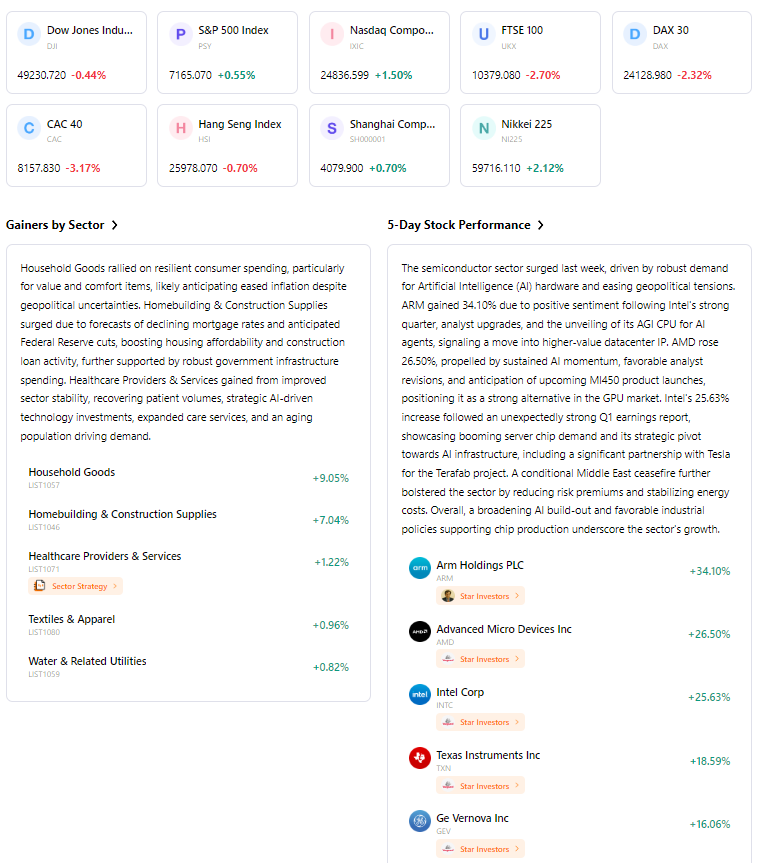

Market Performance Overview: U.S. equity markets generally showed resilience, extending their advance for a third consecutive week and reaching new all-time highs for the S&P 500, NASDAQ Composite, and Small Cap S&P 600 by mid-week. The S&P 500 notably crossed the 7,000 point barrier for the first time. On Monday, April 20, major indices experienced a slight pullback, with the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite closing modestly lower, while the Russell 2000 posted gains. Technology led sector performance with an 8.09% gain, followed by Communication Services (+6.28%) and Consumer Discretionary (+6.64%). Conversely, the Energy sector corrected, declining 3.50% as oil prices fell.

Key Events Analysis: The primary market driver was the evolving geopolitical situation in the Middle East. Initial concerns over the U.S.-Iran conflict and the Strait of Hormuz led to market caution, but a subsequent ceasefire and reopening of the waterway fueled a significant rally. Q1 2026 earnings season saw a strong start, with major U.S. banks reporting better-than-expected results, and S&P 500 earnings growth expectations revised up to 12%. Companies like Tesla, UnitedHealth Group, Moodys, Philip Morris Intl, AT&T, and GE Vernova were among those reporting earnings.

Flows & Sentiment: Global equity funds saw their fourth consecutive weekly inflow through April 15, with U.S. equity funds receiving $21.25 billion. Active ETFs attracted significant inflows. Market sentiment, which was bearish earlier in April, showed cautious optimism regarding a Middle East resolution. The CBOE Volatility Index (VIX) fluctuated, opening at 18.87 on April 20 and closing at 18.71 on April 24, reflecting declining volatility overall.

Overall Assessment: The market demonstrated resilience and responsiveness to geopolitical de-escalation this week. Despite initial volatility from U.S.-Iran tensions and mixed economic data, a resolution in the Middle East propelled equities to new highs. This rapid recovery suggests investor confidence in fundamental strength, though underlying macroeconomic challenges persist.

Next Week's Key Market Drivers & Investment

Upcoming Events: The week ahead will feature several key economic data releases, including Retail Sales on Tuesday, Jobless Claims on Thursday, and Consumer Sentiment on Friday. The Q1 2026 earnings season will continue, with notable reports from Verizon Communications, Coca-Cola, General Motors, Spotify, and Starbucks. An FOMC Meeting is also scheduled for April 29, 2026.

Market Logic Projection: Market behavior next week will likely hinge on incoming economic data, particularly Retail Sales, which will provide insight into consumer spending and economic momentum. Geopolitical developments in the Middle East will continue to be a significant factor. The interplay between labor market conditions, consumer sentiment, and overall economic growth will be crucial for shaping market direction.

Strategy & Allocation Recommendations: Navigen Wealth Management advises reducing U.S. equity exposure to an underweight position, citing a negative intermediate-term trend despite a positive long-term outlook. Investors should maintain a disciplined approach given the constructive yet fragile market backdrop.

Risk Alerts: Continued geopolitical instability in the Middle East, particularly affecting the Strait of Hormuz, remains a key risk that could disrupt supply chains and escalate energy prices. Persistent inflationary pressures, especially from energy costs, continue to influence central bank policy decisions. Policy uncertainty, including Federal Reserve leadership dynamics, adds an additional layer of risk to the outlook.

Markets Weekly

5-Day Index Performance

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.