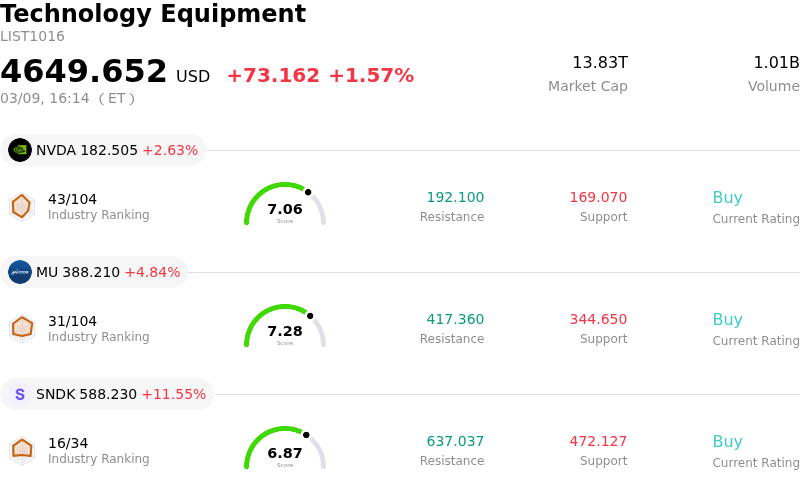

Micron Technology Inc Stock (MU) Closed Up by 4.84% on Mar 9: A Full Analysis

Micron Technology Inc (MU) closed up by 4.84%. The Technology Equipment sector is up by 1.57%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 2.63%; Micron Technology Inc (MU) up 4.84%; SanDisk Corporation (SNDK) up 11.55%.

What is driving Micron Technology Inc (MU)’s stock price up today?

Micron Technology's stock experienced significant upward movement today, primarily driven by a confluence of strong industry tailwinds, highly favorable analyst sentiment, and anticipation of robust financial performance.

The memory chip market, particularly for DRAM and High-Bandwidth Memory (HBM), is facing a severe shortage, largely due to insatiable demand from artificial intelligence (AI) data centers. These data centers are consuming a substantial portion of the available supply, leading to a significant increase in memory component prices. Analysts project that this elevated pricing and tight supply will persist, with normalization not expected until at least 2027. Micron, as a key producer of these essential memory types, is directly benefiting from this dynamic, gaining substantial pricing power. Its entire 2026 HBM supply is reportedly already sold out under locked agreements, de-risking future revenue streams.

Adding to the positive momentum, multiple investment firms have recently reiterated "Buy" or "Outperform" ratings for Micron and significantly raised their price targets. Firms such as Citigroup, Susquehanna, Stifel, UBS, Needham, Morgan Stanley, and Mizuho have issued bullish outlooks, with some targets reaching as high as $650. These adjustments reflect a growing confidence in Micron's ability to capitalize on the accelerating AI-driven memory demand and the resulting favorable supply-demand dynamics.

Furthermore, investor excitement is building ahead of Micron's fiscal Q2 2026 earnings report, scheduled for March 18. The company previously delivered strong Q1 2026 results, exceeding revenue and earnings per share expectations, and provided encouraging Q2 guidance. Market commentary suggests expectations for another earnings beat and strong forward guidance, fueled by the relentless spending on AI infrastructure and the surging memory prices. Micron's management is reportedly guiding for record-setting revenue and exceptional gross margins, signaling an unprecedented period of profitability. The company has also recently started shipping samples of its new 256GB SOCAMM2 LPDDR5X-based module, the industry's highest-capacity low-power DRAM for AI data centers, which further enhances its product portfolio for the high-growth AI segment.

Technical Analysis of Micron Technology Inc (MU)

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of [11.21], indicating a neutral signal. The RSI at 42.62 suggests neutral condition and the Williams %R at -95.90 suggests oversold condition. Please monitor closely.

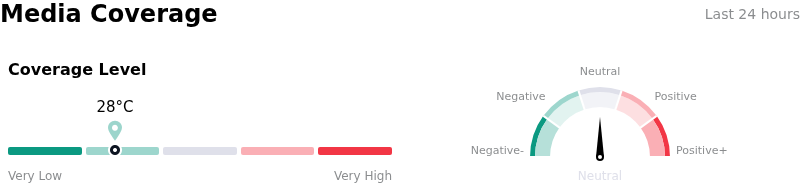

Media Coverage of Micron Technology Inc (MU)

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 28, indicating a low level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Micron Technology Inc (MU)

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $388.17, a high of $650.00, and a low of $86.28.

More details about Micron Technology Inc (MU)

Company Specific Risks:

- Increased competitive pressure in the High Bandwidth Memory (HBM) market, particularly from Samsung and SK Hynix, could pressure Micron's market share and future guidance, with reports indicating potential exclusion from Nvidia's next-generation HBM4 supplier list for Vera Rubin accelerators.

- Execution risk remains regarding the successful ramp-up of Micron's HBM4 production, specifically the transition from pilot to full production at its India assembly line, which could lead to market share loss if delays occur.

- Concerns about Micron's elevated valuation make the stock susceptible to market corrections and shifts in investor sentiment, as some analyses suggest it is overvalued despite strong fundamentals.

- Underlying concerns about potential oversupply or weakness in demand for other DRAM and NAND markets, outside of the robust AI-driven HBM sector, could negatively impact overall revenue and profitability.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.