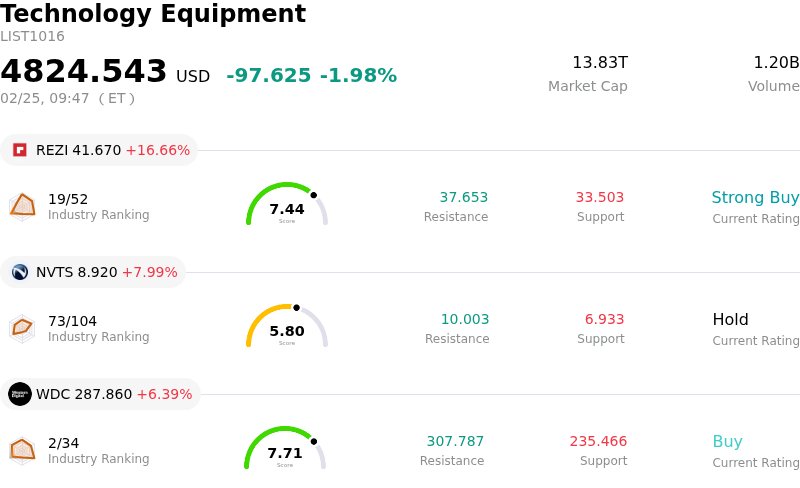

Lam Research Corp Stock Opened Up by 3.04% on Feb 25: Drivers Behind the Movement

Lam Research Corp (LRCX) opened up by 3.04%. The Technology Equipment industry is down by 1.98%. The company outperformed the industry. Top 3 gainers of the industry: Resideo Technologies Inc (REZI) up 16.66%; Navitas Semiconductor Corp (NVTS) up 7.99%; Western Digital Corp (WDC) up 6.39%.

Lam Research (LRCX) experienced significant intraday volatility, concluding the day with an upward movement, primarily driven by a confluence of strong company-specific performance, optimistic guidance, and favorable industry dynamics. The positive momentum reflects sustained investor confidence in the company's market position within the semiconductor equipment sector.

A key catalyst for this upward trend originated from the company's robust second-quarter fiscal year 2026 earnings report and subsequent guidance, released in late January. Lam Research surpassed analyst expectations for both revenue and earnings per share for the reported quarter. More importantly, the company issued an encouraging outlook for the third quarter of fiscal year 2026, with guidance for both EPS and revenue exceeding consensus estimates. Management commentary accompanying these results emphasized accelerating demand in the semiconductor industry, particularly driven by artificial intelligence (AI) and investments in advanced foundry and DRAM technologies, which directly benefit Lam Research's core business in wafer fabrication equipment.

Following the strong financial disclosures, numerous analysts revised their price targets for Lam Research upwards, reinforcing a widespread "Strong Buy" or "Buy" consensus across the investment community. This positive analyst sentiment and their continued belief in the company's growth trajectory likely contributed to the stock's performance and investor interest. The company's focus on innovative technologies like advanced packaging, which is projected to see substantial growth, further bolsters its competitive advantage and long-term prospects.

Broader industry trends also played a significant role. The semiconductor equipment market is experiencing robust expansion, with global sales projected to reach record highs in 2026. This growth is underpinned by increasing demand for high-performance computing, AI, and 5G infrastructure, all of which require advanced chip manufacturing capabilities where Lam Research is a critical supplier. The company's strategic initiatives, including leadership transitions and partnerships aimed at developing next-generation specialty devices, further underscore its proactive approach to capitalizing on these industry tailwinds. The overall market environment, characterized by an intensifying AI infrastructure boom driving the semiconductor industry towards record annual sales, provides a strong macroeconomic backdrop for companies like Lam Research.

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [8.93], indicating a neutral signal. The RSI at 61.62 suggests neutral condition and the Williams %R at -11.49 suggests oversold condition. Please monitor closely.

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is 18.44B, ranking 12 in the industry. The net profit is 5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 269.87, a high of 325.00, and a low of 116.32.

Company Specific Risks:

- Increased geopolitical and regulatory exposure to China, which accounts for 35% of revenues, heightens vulnerability to potential Chinese mandates for domestic chip equipment usage and geopolitical tensions.

- The stock exhibits an elevated valuation, with a P/E ratio of approximately 49.85, significantly above its historical median, indicating that current prices may already discount a highly optimistic future, limiting further upside potential.

- Recent insider selling includes a director reducing their holdings by over 12% and an investment advisor firm trimming its stake by more than 50%, potentially signaling diminished confidence from informed parties.

- Potential demand volatility from leading-edge clients and anticipated capital expenditure cuts by major customers like Intel pose risks to future equipment orders and overall market potential.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.