$11.4 Billion Revenue Vs. 1.75 Trillion Valuation: Can Starlink Support SpaceX IPO?

AI Podcast

Starlink's 2025 revenue reached $11.4 billion with a 63% EBITDA margin, becoming SpaceX's sole profitable segment as xAI incurs losses and rocket launch growth slows. User base doubled to 10 million by February 2026. Starlink's vertical integration and expansion into B2B sectors like aviation and maritime drive profitability. While Starlink shows strong growth, potential IPO valuation relies heavily on this segment, facing competition and risks from xAI's cash burn and launch delays. Future growth depends on sustained expansion, technological advancements, and market acceptance of its valuation narrative.

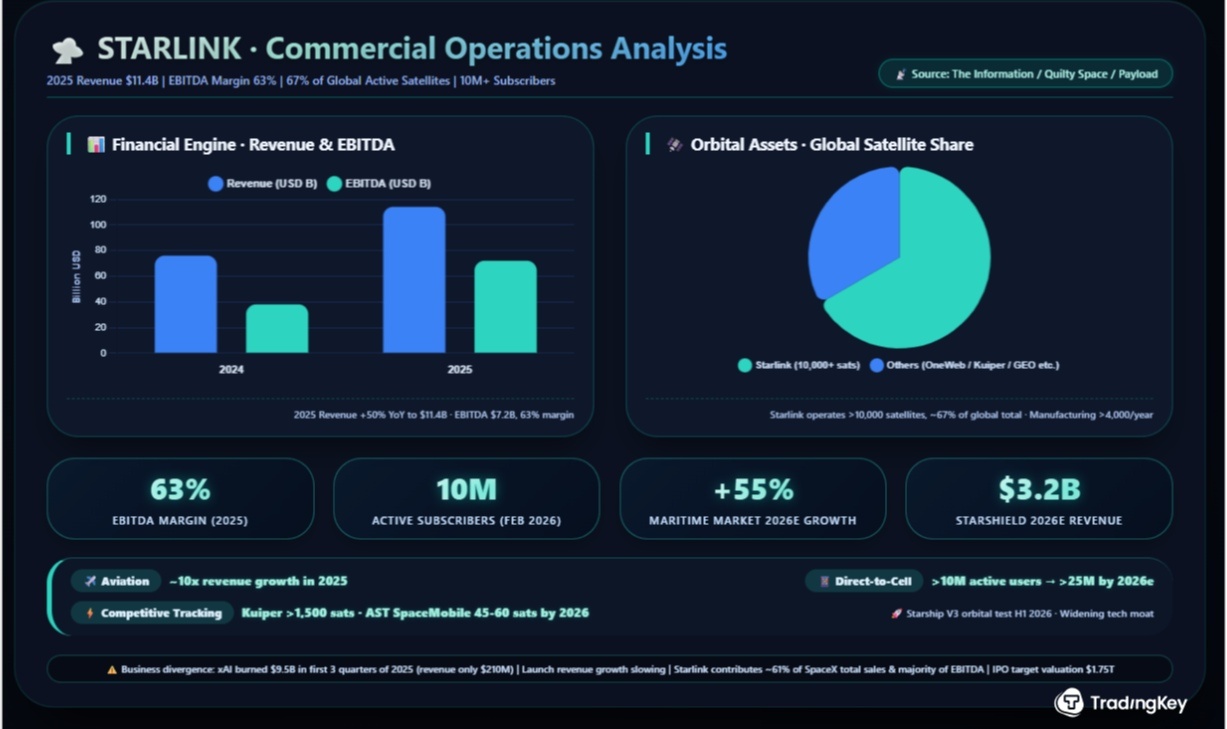

TradingKey - On April 14, The Information disclosed a set of non-public financial data: Starlink's satellite internet business revenue grew 50% year-over-year in 2025 to $11.4 billion, with EBITDA reaching $7.2 billion and an adjusted profit margin as high as 63%. Starlink is now the only profitable business segment under SpaceX, accounting for 61% of total sales, while the xAI artificial intelligence business is still "burning cash" and revenue growth in the rocket launch business has slowed.

What does $11.4 billion signify? This figure exceeds the annual revenue of traditional aerospace giants such as Boeing ( BA) and Lockheed Martin ( LMT ), meaning that a satellite internet project founded just six years ago has already successfully navigated the entire chain from technical verification to large-scale commercial monetization.

From 4.5 Million to 10 Million: What’s Driving the Doubling of Starlink’s User Base?

The rapid growth of Starlink's revenue is rooted in the significant expansion of its user base. In 2025, Starlink's user count doubled, jumping from approximately 4.5 million at the beginning of the year to 9 million by year-end, with an average of about 20,000 new users added daily in November and December. By February 2026, global active users surpassed 10 million. Starlink network traffic more than doubled in 2025, covering over 150 markets worldwide.

By the end of 2025, Starlink had over 10,000 satellites in orbit, accounting for approximately two-thirds of the global total. Satellite manufacturing speed increased from about 2,880 satellites per year in 2024 to over 4,000. This vertically integrated model—where satellite manufacturing, rocket launches, and terminal operations are all handled in-house—gives Starlink a cost structure that traditional telecommunications operators find difficult to match.

An EBITDA margin of 63% is exceptionally impressive in any industry. In comparison, the average EBITDA margin for global mobile network operators typically ranges between 30% and 40%, while traditional satellite communication operators (such as Viasat and Eutelsat) hover around 20%. Starlink's margin rose from 41% in 2023 to 50% in 2024, and reached 63% in 2025. This improvement stems primarily from two factors: the extremely low marginal cost of adding new users and the expanding share of high-margin B2B segments (aviation, maritime, and government) within the revenue mix. In 2025, Starlink's aviation revenue is projected to grow nearly tenfold, while maritime installations continue to climb. The maritime market alone is expected to contribute $1.9 billion in 2026, a year-over-year increase of 55%.

Government and defense business (Starshield) is another major driver of profitability. A $537 million contract signed with the U.S. Department of Defense will continue through 2027, and Quilty Space expects Starshield to contribute $3.2 billion in revenue by 2026. The Direct-to-Cell service already has approximately 650 satellites in orbit, with monthly active users surpassing 10 million and projected to exceed 25 million by the end of 2026.

xAI Burns $9.5 Billion: How Severe Is SpaceX’s Business Divergence?

Starlink's stellar performance stands in contrast to SpaceX's other business segments. While the rocket launch business remains profitable, its revenue growth has slowed; meanwhile, xAI, Musk's strategic piece against OpenAI, is still in the early stages of model training and computing power investment, far from the point of commercialization. According to data from The Information, xAI burned $9.5 billion in the first three quarters of 2025, while revenue for the same period was only $210 million.

This divergence creates a structural contradiction at the valuation level. SpaceX is planning to launch an IPO in 2026 with a target valuation as high as $1.75 trillion. However, the foundation supporting this valuation relies almost entirely on the Starlink business line. According to a Reuters report, SpaceX's total revenue for 2025 is approximately $15 billion to $16 billion, with an EBITDA of about $8 billion. Starlink accounts for 61% of revenue and contributes the vast majority of EBITDA, while xAI continues to incur losses and the rocket launch business provides a limited contribution.

$20 Billion Expectation vs. Accelerating Competition: Can Starlink’s Growth Be Sustained?

Looking ahead to 2026, institutional revenue forecasts for Starlink vary significantly. Quilty Space predicts Starlink's 2026 revenue will reach $20 billion, with an EBITDA of approximately $14 billion. Payload Space’s forecast is more aggressive, projecting an 80% revenue increase to $18.7 billion, accounting for roughly 79% of SpaceX's total revenue.

The core support for these optimistic expectations lies in Starlink's transition from a pure "land grab" phase focused on user numbers to a new stage characterized by diversified revenue structures and refined pricing strategies. In the high-end market, Starlink is accelerating its penetration into high-value sectors such as aviation, maritime, and government contracts. In emerging markets, driven by robust demand and tight bandwidth resources, Starlink maintains premium pricing and imposes demand surcharges. This pricing strategy effectively balances global expansion with the quality of profitability.

Furthermore, the first orbital flight test of Starship V3 could take place as early as the first half of 2026. A single Starship V3 launch can deploy approximately 100 next-generation Starlink V3 satellites. Each satellite boasts a communication capacity of up to 1 Tbps and features a fully upgraded laser-interconnected network, which is expected to further widen Starlink's technological lead.

However, competitors are also accelerating their catch-up efforts. Amazon's Project Kuiper is facing a critical FCC licensing milestone: it must deploy at least 1,618 satellites by July 2026, or its spectrum authorization will be at risk. More than 1,500 satellites have already been deployed, utilizing ULA's Atlas V, the in-house New Glenn, and Europe's Ariane rockets, and even leveraging SpaceX's Falcon 9 for deployment. Additionally, AST SpaceMobile plans to deploy 45 to 60 satellites in 2026 to launch commercial direct-to-device services, with investment support from AT&T and Verizon.

The competitive landscape is evolving from a single technical race into a multi-dimensional interplay of technology, capital, and regulation. Meanwhile, SpaceX itself faces structural constraints—the expansion speed of Starlink is highly dependent on SpaceX's internal launch schedule. Any delays in Falcon 9 or Starship missions will directly impact the pace of Starlink's constellation network construction. This also exposes the vulnerability of the entire Low Earth Orbit (LEO) satellite industry.

What supports a $1.75 trillion valuation?

SpaceX’s targeted $1.75 trillion IPO valuation implies a staggering 109x price-to-sales multiple based on projected 2025 revenue of roughly $16 billion. Even factoring in robust growth expectations for 2026, this multiple remains significantly higher than those of other high-valuation tech peers like Tesla and Palantir. Wedbush analysts suggest the valuation is heavily driven by an "orbital intelligence" narrative surrounding a potential early 2026 merger between SpaceX and xAI—a move to integrate the Grok AI model directly into the Starlink network for on-orbit edge computing. Market conviction in this narrative will be a decisive factor for the IPO’s pricing power.

Whether the market can digest a $1.75 trillion valuation hinges on investor buy-in for the "orbital intelligence" narrative. Fundamentally, Starlink’s 63% EBITDA margin, subscriber base exceeding 10 million, and projected 2026 revenue of over $20 billion provide a solid commercial bedrock. However, ongoing losses at xAI, intensifying competition, and stagnant growth in the rocket launch segment represent significant risks. Another critical variable is the deployment timeline for Starship V3; delays in Starship testing could stall the V3 network rollout, potentially eroding Starlink’s technological edge and souring the market’s outlook on SpaceX’s long-term growth trajectory.

Summary

Starlink surpassing $11.4 billion in revenue for 2025 marks a landmark pivot for Elon Musk’s commercial space endeavor, shifting from "cash burn" to "cash flow generation." When a firm can deliver reliable broadband from space to 10 million users and generate substantial profits, it ceases to be a science fiction concept and becomes a bona fide infrastructure operator. Yet, if SpaceX seeks a $1.75 trillion valuation in the capital markets, Starlink’s current financials might not suffice. Investors are demanding answers: How long can Starlink’s rapid growth persist? Will the emergence of rivals threaten its dominant position? Is the emerging narrative of AI integration a fundamental value driver or a valuation bubble? As momentum builds toward a SpaceX IPO, the global discourse on the value and frontiers of space-based internet is only just beginning.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.