Pop Mart Soars Over 13%, Market Cap Tops HK$400 Billion; CEO Projects Effortless HK$30 Billion Revenue in 2025

TradingKey - On Wednesday, August 20, Pop Mart (9992.HK) shares soared more than 13% to HK$318.4 during Hong Kong trading, pushing its market cap past the HK$400 billion mark. The stock closed up 12.54% at HK$316.

In the first half of 2025 (FY2025 H1), Pop Mart's performance exceeded expectations significantly, with net profit soaring nearly 400% and revenue climbing 204.4% to surpass HK$10 billion. On Wednesday, CEO Wang Ning provided an optimistic outlook during a conference call, stating that achieving HK$30 billion in revenue this year should be "quite easy." Management anticipates that the net profit margin will continue to improve in the second half, reaching approximately 35%.

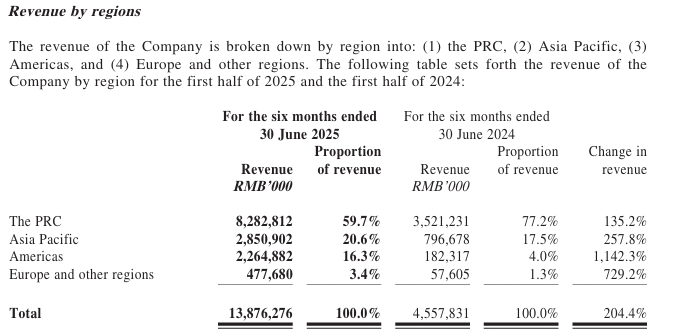

Overseas Revenue Jumps 440%, Plans to Open Three Stores Weekly in H2

In the first half of the year, overseas markets (including Hong Kong, Macau, and Taiwan) became the primary driver of revenue growth. Overseas business revenue surged 440% year-on-year to HK$5.59 billion, increasing its share of total revenue from 22.8% to 40.3%. The Americas saw a growth of 1142.3%, and Europe and other regions grew by 729.2%. The number of retail stores in the Americas expanded from 10 in early 2024 to 41 this year. In the Asia-Pacific region, Pop Mart opened a large store this month at Bangkok's landmark shopping center, Iconsiam.

Management disclosed that markets in countries like Germany and Mexico are just getting started, and they're exploring emerging markets in the Middle East, Central Europe, and Central and South America. In the second half of the year, they plan to maintain an average opening rate of 3 stores per week. Wang Ning expressed high confidence in faster-than-expected overseas market growth, anticipating that overseas sales might surpass the Chinese market by 2025.

Pop Mart's Overseas Market Revenue, Source: Pop Mart

Labubu Emerges as a Cash Cow; New Mini Labubu to Be Released

A notable highlight is the IP THE MONSTERS, featuring the global sensation Labubu, which generated HK$4.81 billion in revenue, accounting for 34.7% of the company’s total, solidifying it as a cash cow. Last year, this IP’s revenue share was only 13.7%.

.jpg)

Pop Mart's Revenue by IPs, Source: Pop Mart

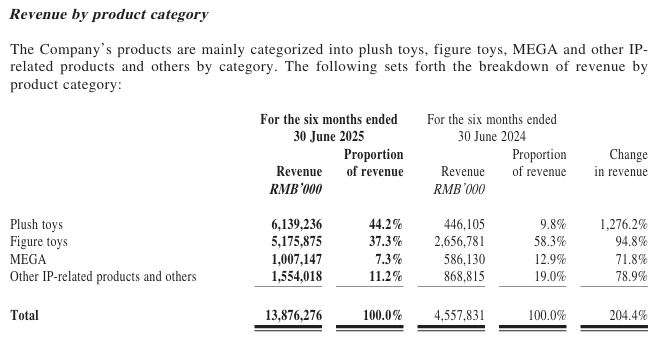

Thanks to the high demand for the third-generation Labubu vinyl plush series "High Energy Ahead," which sold out immediately upon release, the plush product category saw a 1276.2% year-on-year increase to HK$6.14 billion, becoming the largest category at 44.2% of total revenue.

Pop Mart's Revenue by product category, Source: Pop Mart

Wang Ning doesn’t believe that a single IP contributing a large portion of revenue is unhealthy. However, he mentioned that the new Labubu products were launched in a relatively restrained manner, preserving the IP's value for future growth. He hopes Labubu will become a super IP like Mickey Mouse or Hello Kitty, possessing high commercial value even when public discussion is low. He hinted at the release of a mini version of Labubu this week, potentially the next big hit, which can be hung on phones.

Furthermore, Pop Mart’s range of original IPs demonstrates the company’s health as a platform-based IP creator. Besides its popular IPs, emerging IPs like Twinkle Twinkle have performed well, generating HK$390 million in half-year revenue. Morgan Stanley observed at Pop Mart's international toy fair that Twinkle Twinkle's booth attracted large crowds and sold out quickly, indicating this IP could significantly contribute to sales in 2025 and beyond.

Monthly Production Capacity Soars Tenfold, Yet Challenges Loom

Despite Labubu's significant sales, its revenue share is only 34.7%. The management pointed out that the main challenge lies in production capacity.

Due to overwhelming market demand for plush products, the company is in a phase of rapid capacity expansion. The core strategy is to maximize production capabilities. Compared to last year, production capacity has improved significantly, with monthly plush production now over 10 times higher than the same period last year.

Following the earnings release, Morgan Stanley stated that Pop Mart's intrinsic value is undervalued by the market, with profitability likely to improve further. The firm gave an "overweight" rating with a target price of HK$365, predicting adjusted price-to-earnings ratios of 46, 32, and 26 times for 2025-2027, respectively.

JPMorgan considers Pop Mart a top pick in China's consumer sector, with potential inclusion in the Hang Seng Index (announcement on August 22, adjustment on September 8). Nomura Securities suggests that inclusion in the index could be another strong positive catalyst for the stock, giving it a "buy" rating and a target price of HK$330.

This year, Pop Mart's stock price has risen over 250%, with its market cap now exceeding industry giants like Barbie maker Mattel and Hello Kitty parent company Sanrio.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.