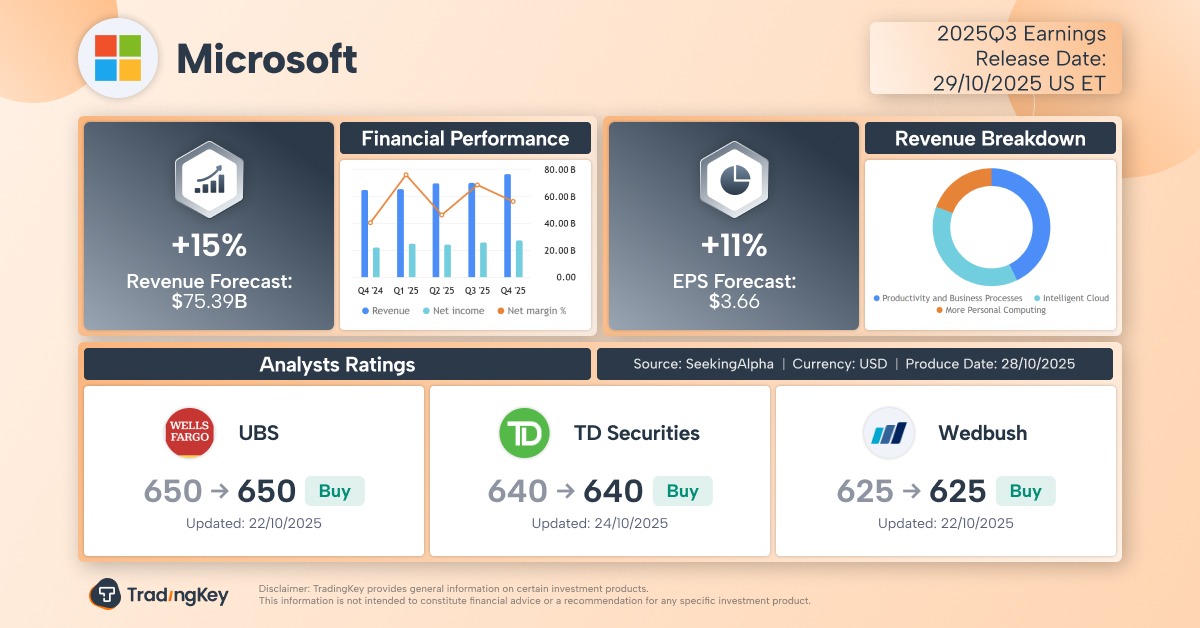

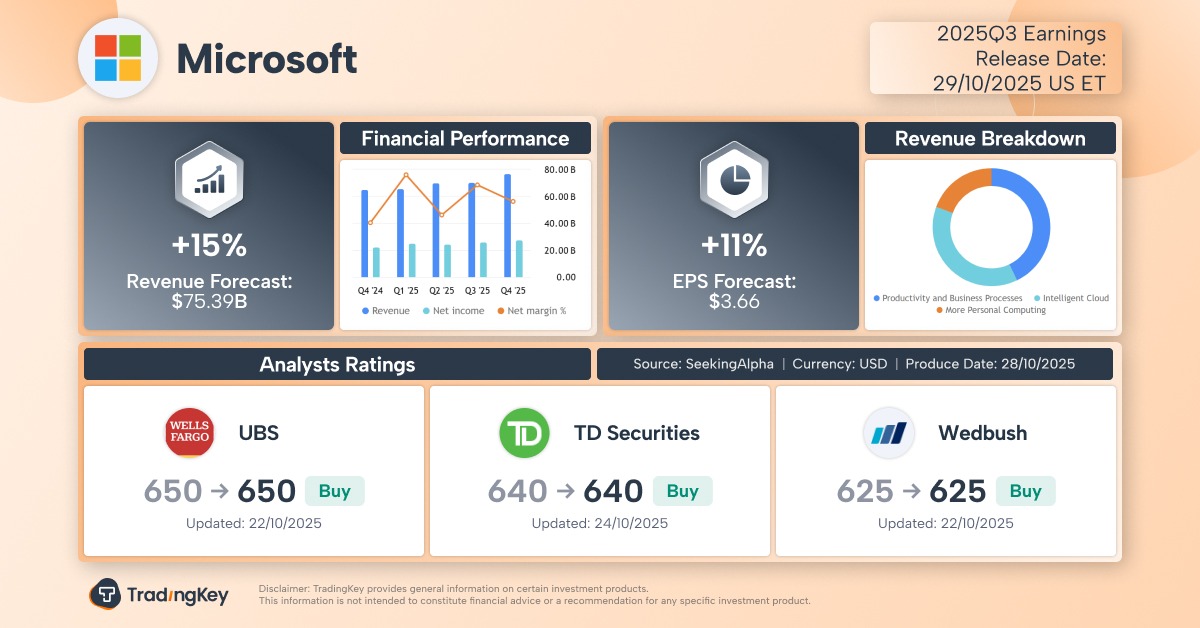

Microsoft Q1 Earnings Preview: AI-Powered Cloud Growth Fuels Wall Street’s “Zero Sell” Consensus

TradingKey - AI giant Microsoft (MSFT) will report its Q1 FY2026 earnings (natural Q3 2025) on October 29. While Microsoft’s stock has shown little movement since its last strong earnings beat, Wall Street analysts expect another quarter of AI-driven cloud growth outpacing peers, with EPS potentially exceeding expectations for the 10th consecutive quarter — a streak underscored by a rare “zero sell ratings” consensus, reflecting overwhelming analyst optimism.

According to Seeking Alpha, analysts forecast:

- Revenue: $75.39 billion, up 15% YoY from $65.59B

- EPS: $3.66, up 11% YoY from $3.30

Similar to last quarter, analysts remain bullish on Microsoft’s cloud segment, projecting Azure and related cloud services to grow over 30% — slightly below management’s earlier guidance of ~37% for FY2026.

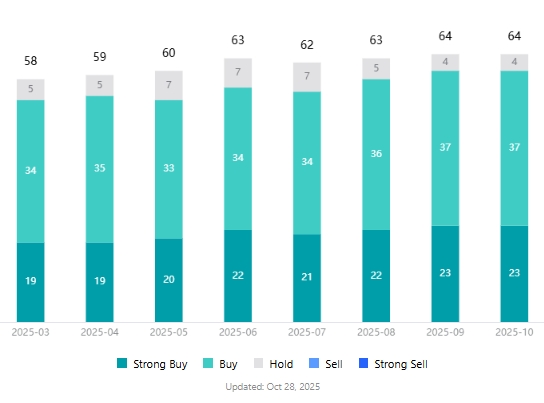

As of this report, among 64 analysts covering Microsoft, none rate it as “Sell”, and nearly 94% recommend “Buy.”

Wall Street Analyst Ratings for Microsoft Stock, Source: TradingKey

AI Cloud Continues to Gain Market Share

When CEO Satya Nadella reported Q4 FY2025 results in July, he emphasized that cloud computing and AI are driving transformation across industries, and Microsoft is innovating across the tech stack to help customers adapt and grow.

The global cloud market remains dominated by three players:

- Amazon AWS: 30% share

- Microsoft Azure: 20%

- Google Cloud: 13%

With Alibaba and Oracle trailing at 4% and 3%, respectively.

In Q2 2025, Azure’s revenue grew 39%, outpacing Google Cloud’s 32% and AWS’s 17.5%. Driven by broad-based workload growth, Azure delivered 34% annual growth in FY2025, reaching $75 billion in revenue — accounting for 27% of Microsoft’s total FY2025 sales and nearly doubling the company’s overall 15% growth rate.

Angelo Zino, CFRA analyst with a “Strong Buy” rating, expects Azure to maintain strong momentum into FY2026 and beyond, with AI services increasingly contributing to overall revenue.

Karl Keirstead, UBS analyst, said sustained and healthy cloud spending will continue to benefit Amazon, Microsoft, and Google, noting that recent conversations with enterprise clients and partners reveal positive sentiment around core cloud infrastructure spending.

Keirstead added that customer and partner sentiment continues to improve. Major Azure partners report accelerating growth trends, and the Microsoft-OpenAI partnership will further enhance Azure’s outlook over the next several years.

Despite overall optimism, growth divergence among the “Big Three” may persist. UBS notes limited upside potential for AWS estimates, while Azure and Google Cloud have greater room for upward revisions.

Industry observers suggest Azure’s growth may accelerate in Q3 and further in Q4, continuing to gain share, while AWS could underperform in Q3 before stabilizing in Q4.

Per Visible Alpha, Q3 forecasts show:

- Microsoft Azure: +38.4%

- Google Cloud: +30.1%

- Amazon AWS: +18%

Jamie Murray, CEO of The Murray Wealth Group, said that among the five ‘Magnificent Seven’ companies reporting this week, Microsoft and Google will be the standout picks of Q3 earnings season.

He praised Microsoft’s capital efficiency and operational excellence, and is optimistic that cloud growth could reach 40%.

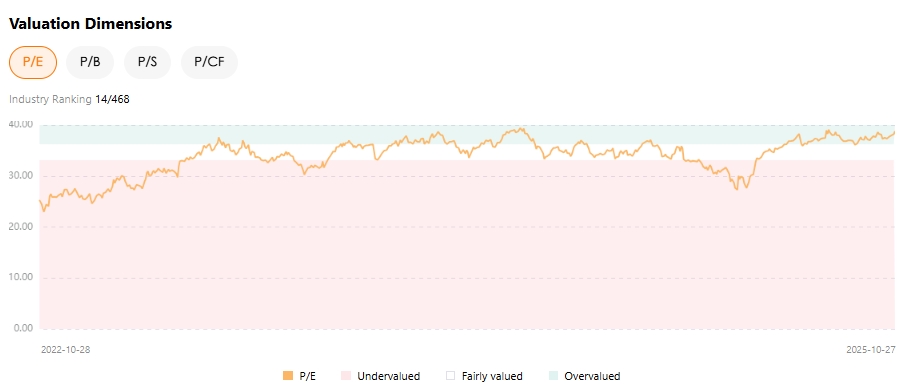

High Valuation? Don’t Underestimate Office’s Monopoly Position

Year-to-date, Microsoft shares are up 26%, outperforming the Nasdaq’s 22.41% and Amazon’s 3.46%. According to TradingKey’s Stock Score tool, Microsoft trades at a P/E of 38.80 — near a three-year high.

Yet analysts remain overwhelmingly positive, with an average price target of $612.74, implying about 15% upside from current levels.

John DiFucci, Guggenheim analyst, acknowledged Microsoft’s valuation isn’t cheap — and may never be “cheap” — but stressed that exceptional fundamentals justify the premium.

He highlighted two key drivers:

- Azure’s direct exposure to the AI wave, with a sustainable subscription model fueling future growth

- Microsoft’s unique ability to monetize AI through its Office monopoly — with M365 poised to generate incremental revenue and profit atop its dominant productivity software base

The EPS Beat Streak Continues?

Per Tipranks, Microsoft has beaten EPS estimates in nine of the past ten quarters. If Q3 delivers strong results, it would mark the 10th consecutive beat — a testament to consistent execution.

However, EPS beats don’t always lift the stock: in the past nine earnings reactions, five saw price declines — ranging from 1.08% to 6.18%.

Analysts say markets will focus on four key areas:

- Growth rate of Intelligent Cloud

- Resilient operating margins despite rising capex

- Expansion in Productivity & Business Processes

- Updates on capital spending and AI monetization — especially whether AI data centers begin generating revenue in H1 2026, or if delays push it to H2

Risks Ahead: AI Bubble, Competition, and Cash Flow

Despite strong sentiment, risks remain:

- A potential AI demand bubble could burst

- Signs of slowing Azure growth

- Commentary from competitors and partners

- Pressure on free cash flow from massive AI investments

Amazon was punished by markets for cloud growth lagging peers, yet maintains strong partnerships. Oracle, boosted by its OpenAI collaboration and Trump’s “Stargate” project, is emerging as a credible challenger.

How long can Microsoft sustain its momentum with its superior product suite and integrated ecosystem? The market will soon find out.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.