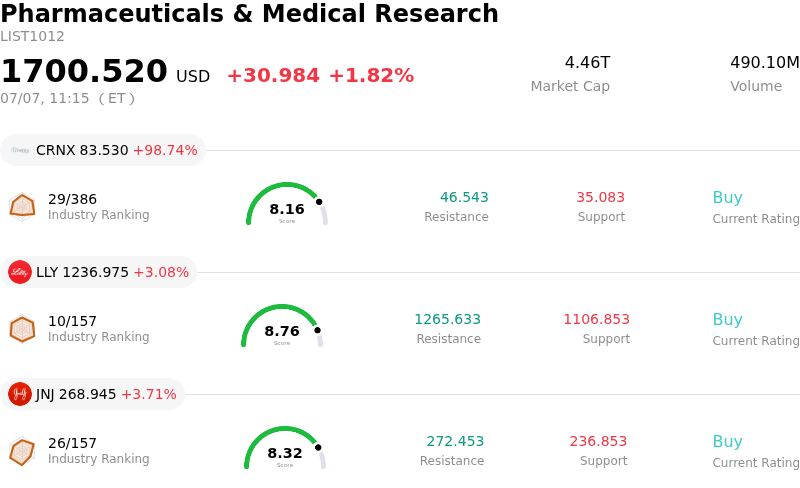

Eli Lilly and Co Stock (LLY) Moved Up by 3.08% on Jul 7: Facts Behind the Movement

Eli Lilly and Co (LLY) moved up by 3.08%. The Pharmaceuticals & Medical Research sector is up by 1.82%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Crinetics Pharmaceuticals Inc (CRNX) up 98.74%; Eli Lilly and Co (LLY) up 3.08%; Johnson & Johnson (JNJ) up 3.71%.

What is driving Eli Lilly and Co (LLY)’s stock price up today?

The upward movement in Eli Lilly’s share price is primarily driven by highly positive Wall Street sentiment ahead of the company's upcoming earnings release. Analysts at JPMorgan raised their price target on the stock, citing strong confidence in the pharmaceutical giant’s growth trajectory. The upward revision is underpinned by expectations of continued international expansion for Mounjaro, robust domestic sales of its best-selling obesity drug Zepbound, and the massive market potential for its GLP-1 and triple-receptor agonist pipeline. Analysts anticipate the upcoming quarterly financial results will comfortably exceed previous market consensus on both top-line revenue and bottom-line earnings per share.

Further driving market optimism is a significant positive regulatory tailwind concerning access. The launch of the Medicare GLP-1 Bridge program has officially gone live, introducing wider insurance coverage and offering a flat monthly copay for eligible members. This demonstration program has eased investor concerns regarding drug pricing pressures by demonstrating that policy shifts can dramatically widen patient volumes, which offsets potential price-concession headwinds. With the overall obesity treatment market projected to expand exponentially over the next decade, institutional confidence remains anchored in Eli Lilly's market leadership and clinical breakthroughs.

Technical Analysis of Eli Lilly and Co (LLY)

Technically, Eli Lilly and Co (LLY) shows a MACD (12,26,9) value of 6.628, indicating a buy signal. The RSI at 63.905 suggests neutral condition and the Williams %R at 23.895 suggests buy condition. Please monitor closely.

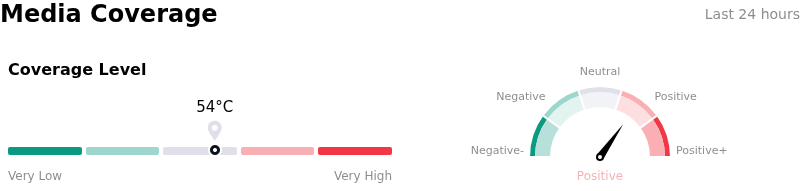

Media Coverage of Eli Lilly and Co (LLY)

In terms of media coverage, Eli Lilly and Co (LLY) shows a coverage score of 54, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Eli Lilly and Co (LLY)

Eli Lilly and Co (LLY) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is $65.18B, ranking 4 in the industry. The net profit is $20.64B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1216.27, a high of $1500.00, and a low of $850.00.

More details about Eli Lilly and Co (LLY)

Company Specific Risks:

- Accelerating GLP-1 Pricing Pressure and Realized Price Erosion: Eli Lilly is experiencing systemic declines in net realized drug prices, which are projected to drag down top-line revenue growth in the low-to-mid teens range. This margin compression is expected to worsen following the July 1, 2026 launch of the Medicare GLP-1 Bridge program, which caps patient out-of-pocket costs for Zepbound and Foundayo at $50 per month.

- Regulatory Backlash Over 340B Program Restrictions: The company's policy restricting safety-net hospital access to the federal 340B drug discount program and demanding proprietary insurance claims data has generated severe pushback from healthcare trade associations, exposing Eli Lilly to potential federal dispute-resolution actions, administrative penalties, and costly litigation.

- Safety Overhangs and Regulatory Hurdles: Clinical and commercial risks are rising due to heightened regulatory scrutiny, including an FDA demand for additional safety data on liver injury risks associated with the newly approved oral GLP-1 drug Foundayo, alongside hundreds of documented adverse event reports regarding impaired gastric emptying that could limit market adoption.

- Extreme Valuation Multiple and Portfolio Concentration: Trading at a premium price-to-earnings (P/E) multiple of over 42x—significantly higher than the industry average—the stock is highly vulnerable to severe intraday volatility and profit-taking. This valuation risk is intensified by flat-to-declining revenue trends for legacy blockbusters like Trulicity and Verzenio, concentrating Lilly's future growth targets almost entirely on its incretin franchise.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.