HDFC Bank Ltd Stock (HDB) Moved Up by 6.21% on Jul 6: Key Drivers Unveiled

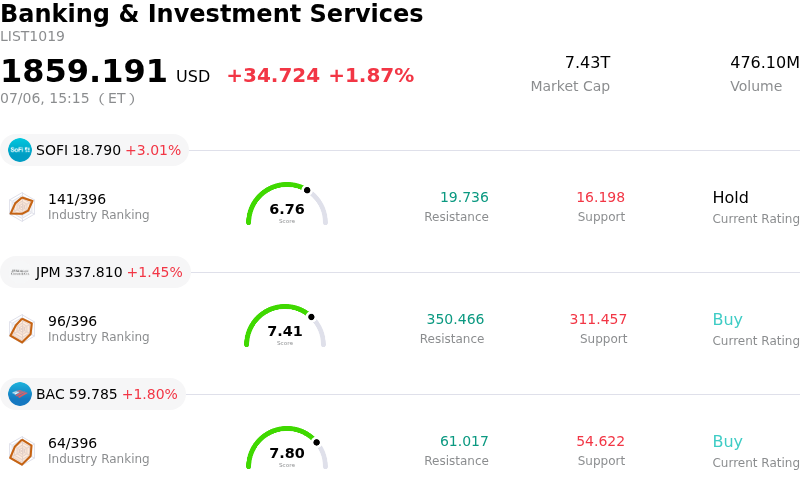

HDFC Bank Ltd (HDB) moved up by 6.21%. The Banking & Investment Services sector is up by 1.87%. The company outperformed the industry. Top 3 stocks by turnover in the sector: SoFi Technologies Inc (SOFI) up 3.01%; JPMorgan Chase & Co (JPM) up 1.45%; Bank of America Corp (BAC) up 1.80%.

What is driving HDFC Bank Ltd (HDB)’s stock price up today?

HDFC Bank has experienced a strong upward movement in its stock price, driven primarily by a robust and highly encouraging first-quarter business update for the fiscal year 2027. This performance has significantly boosted investor confidence, signaling that India’s largest private-sector lender is successfully moving past its post-merger integration challenges.

The primary catalyst for the stock's upward trajectory is the bank's better-than-expected double-digit growth in both lending and funding activities. HDFC Bank reported a substantial 15.4 percent year-on-year increase in gross advances, marking its strongest credit expansion in five quarters. This performance comfortably beat Wall Street and local analyst expectations, demonstrating resilient loan demand across both retail and corporate segments.

Importantly, the bank managed to support this credit expansion by mobilising deposits at an equally impressive rate. Total deposits grew by 14.7 percent year-on-year, outpacing the broader market consensus. By successfully attracting deposits in a highly competitive banking landscape where consumer funds are increasingly migrating toward equities and mutual funds, the bank has relieved concerns over its credit-to-deposit ratio. While low-cost current account savings account deposits grew at a more moderate 9.4 percent, the overall expansion of the balance sheet confirms steady funding capabilities.

Beyond these strong operational metrics, positive sentiment was further supported by significant leadership transitions designed to strengthen governance and strategic direction. The bank announced the board's approval of former Finance Secretary Rajiv Kumar as an independent director and part-time chairman, subject to regulatory approval, which brings substantial regulatory and economic expertise to the helm. Additionally, the appointment of a new chief financial officer-designate establishes a clear path for smooth executive succession.

With sustained foreign institutional investor buying providing additional structural support, the combination of market-beating credit growth, effective deposit mobilization, and institutional governance changes has driven the positive market momentum for the stock, offsetting previous concerns regarding near-term net interest margin pressures ahead of the full quarterly earnings release.

Technical Analysis of HDFC Bank Ltd (HDB)

Technically, HDFC Bank Ltd (HDB) shows a MACD (12,26,9) value of 0.304, indicating a buy signal. The RSI at 60.385 suggests neutral condition and the Williams %R at 11.224 suggests overbought condition. Please monitor closely.

Fundamental Analysis of HDFC Bank Ltd (HDB)

HDFC Bank Ltd (HDB) is in the Banking & Investment Services industry. Its latest annual revenue is $28.79B, ranking 17 in the industry. The net profit is $8.61B, ranking 12 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $34.42, a high of $36.00, and a low of $29.70.

More details about HDFC Bank Ltd (HDB)

Company Specific Risks:

- Elevated Funding Costs and Margin Pressures: While HDFC Bank reported double-digit growth in its June 2026 quarter business update, the loan expansion was heavily driven by time deposits rather than lower-cost CASA (Current Account Savings Account) balances. This shifting funding mix is elevating the bank's overall cost of funds, keeping near-term Net Interest Margins (NIM) under intense pressure.

- Overreliance on One-Off Gains for Profitability: The bank’s Q1 FY26 standalone net profit growth was heavily propped up by one-off disinvestment gains—specifically, a net gain of roughly Rs 6,949 crore to Rs 9,128 crore from the partial sale of its stake in its subsidiary, HDB Financial Services—masking underlying weaknesses in its core operational banking earnings.

- Persistent Governance and Leadership Instability: Despite a recent external review finding no evidence to substantiate claims made by the former non-executive chairman, the lingering effects of his unexpected resignation, alongside legacy compliance matters and recent executive reshuffling (including the appointment of a new CFO), continue to feed institutional skepticism and keep governance risks elevated.

- Deposit Franchise Lag and Credit-to-Deposit Imbalances: Institutional analysts remain concerned about the bank’s ongoing struggle to normalize its elevated loan-to-deposit ratio following its major corporate merger. The bank must aggressively narrow its credit-growth gap with peers, which creates a highly competitive and costly battle for deposits.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.