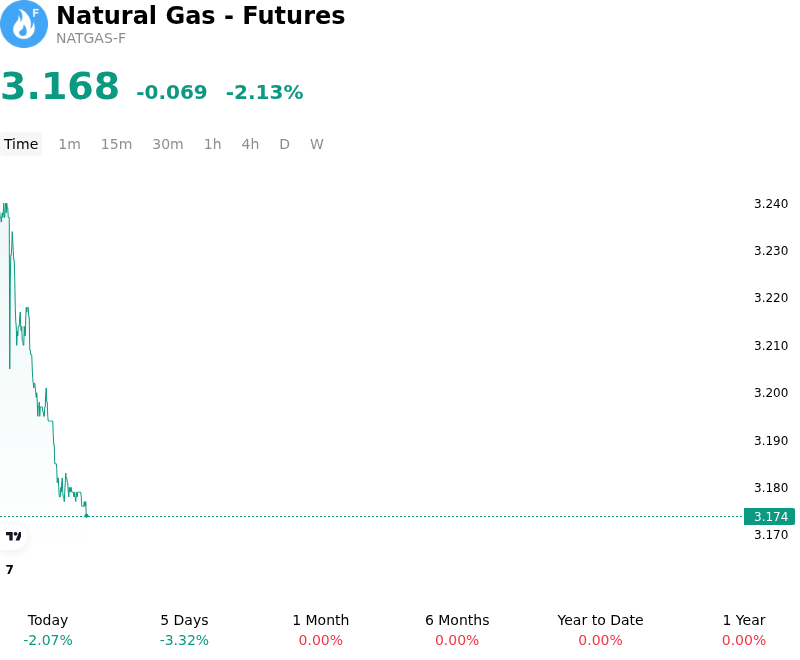

Natural Gas - Futures (NATGAS-F) Is down by 2.13% on Jul 5: Is the Demand Outlook Changing?

Natural Gas - Futures (NATGAS-F) is down 2.13% at Jul 5 20:55(ET), now at $3.168, with a 7-day up of 0.13%.

What is driving Natural Gas - Futures (NATGAS-F)’s stock price down today?

US natural gas futures faced downward pressure as the market reacted to a combination of bearish domestic storage data, strong supply, and shifting weather models that offset the impact of seasonal heat.

The primary catalyst driving negative sentiment was the latest weekly inventory report from the Energy Information Administration. The data showed a larger-than-expected injection of 87 billion cubic feet into underground storage, which surpassed consensus market expectations. This heavy build pushed total domestic stockpiles to more than six percent above the five-year historical average, reassuring market participants of highly comfortable supply buffers and capping immediate upside potential.

On the demand side, recent updates to short-term meteorological models contributed to the price decline. Forecasters adjusted near-term outlooks to show cooling and moderating temperatures across the eastern two-thirds of the United States. This shift lowered overall Cooling Degree Day expectations, which directly translates to reduced gas-fired power burn for air conditioning and effectively stripped the weather-driven demand premium from the prompt contract.

These demand headwind adjustments occurred against a backdrop of highly resilient domestic production. Dry natural gas output in the Lower 48 remained exceptionally robust, averaging around 110 billion cubic feet per day. Strong associated gas production, particularly from Permian Basin drilling, has maintained a persistent oversupply cushion that restricts the market's ability to sustain any summer rallies.

Additionally, broader global supply concerns eased as geopolitical risks in key energy corridors showed signs of improvement. Major importing nations, such as India, began rolling back emergency natural gas allocation curbs after a regional ceasefire facilitated the resumption of normal liquefied natural gas shipments through the Strait of Hormuz. This stabilization of international maritime flows reduced the broader safe-haven and supply-risk premium across global energy markets, further weighing on domestic pricing sentiment.

These bearish factors kept near-term prices under technical pressure, with the front-month contract struggling to find support amidst weak immediate momentum. While long-term structural demand tailwinds from data centers and expanding export terminals continue to build, the current oversupplied spot market and softer mid-July weather outlook keep near-term expectations firmly anchored.

More details about Natural Gas - Futures (NATGAS-F)

Recent Events and Risks:

- Larger-Than-Expected Weekly Inventory Build: The U.S. Energy Information Administration (EIA) reported a working gas injection of 87 billion cubic feet (Bcf) for the week ending June 26, 2026, exceeding consensus market expectations of 79 to 83 Bcf. This bearish print pushed total domestic stockpiles to more than 6% above the historical five-year average, signaling that near-term supply continues to outpace demand.

- Moderating Near-Term Weather Forecasts: Meteorological models from the Commodity Weather Group and other forecasters have adjusted outlooks to show cooling and moderating temperatures across the eastern two-thirds of the United States for July 7–16, 2026. This expected drop in Cooling Degree Days (CDDs) will curb electricity demand for air conditioning, stripping the near-term weather-driven demand premium out of the market.

- Highly Resilient Dry Gas Production: Despite regional maintenance and pipeline constraints, Lower 48 dry natural gas production remains exceptionally strong, averaging approximately 110 to 111.7 Bcf per day (up roughly 2.8% year-over-year). This relentless supply growth reinforces the domestic storage overhang and limits any sustainable price recovery.

- Technical Support Breakdown and Long Liquidation: Natural gas futures recently broke below key trend indicators, including the convergence of the 20-day moving average near $3.21 and a critical rising trendline, sliding to two-week lows. This technical deterioration, paired with broader energy sector weakness from sliding crude oil prices, has triggered institutional long liquidations and speculative selling.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.