Arm Holdings PLC Stock (ARM) Moved Up by 3.76% on Jun 30: Facts Behind the Movement

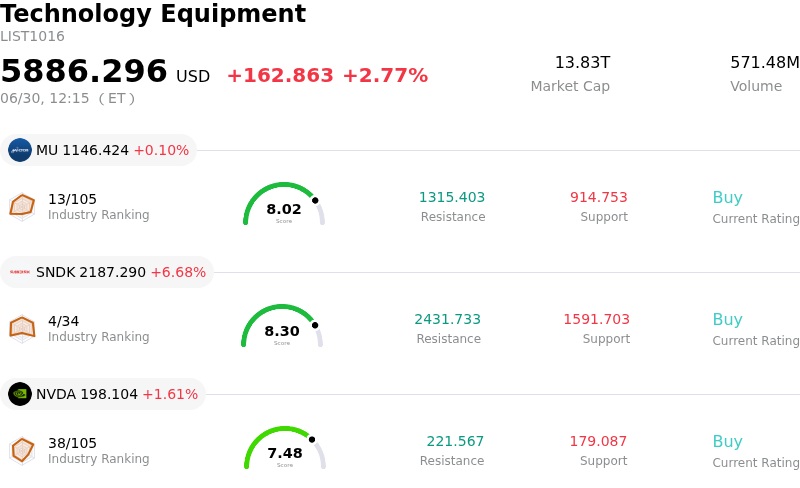

Arm Holdings PLC (ARM) moved up by 3.76%. The Technology Equipment sector is up by 2.77%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 0.19%; SanDisk Corporation (SNDK) up 6.68%; NVIDIA Corp (NVDA) up 1.66%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

Arm Holdings experienced positive movement amid notable intraday volatility, reversing some of the downward pressure seen during recent sector-wide profit-taking. The upward trajectory is primarily driven by mounting institutional optimism surrounding Arm's artificial intelligence and data center capabilities, particularly following the company's recent introduction of its advanced AGI CPU. This processor architecture, targeted at agentic AI workloads, has captured significant market attention as Oracle Cloud Infrastructure and other major cloud and enterprise customers integrate into the ecosystem. Investors are increasingly viewing CPU technology as a major beneficiary of the transition toward agentic AI, where the operational workload shifts from processing to task execution.

This fundamental enthusiasm is further reinforced by a wave of bullish target-price adjustments from Wall Street analysts. Major investment banks have substantially raised their price objectives, citing accelerating CPU demand and the rapid adoption of Arm's energy-efficient Neoverse architecture within AI cloud infrastructure. Analysts expect Arm to rapidly expand its market share in the custom silicon data-center space, which is driving projections for sustained royalty revenue growth.

Despite these positive drivers, the stock remains subject to high intraday volatility due to its premium valuation. Having experienced a massive year-to-date rally, the company trades at a elevated price-to-earnings multiple, leaving it sensitive to minor shifts in market sentiment, interest rate expectations, and macro tech sector trends. While broader market concerns about rising component costs and high tech valuations have recently sparked occasional profit-taking, the underlying business momentum and strong fundamental demand for Arm's IP architecture have ultimately supported the stock's recovery.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of -22.990, indicating a neutral signal. The RSI at 50.105 suggests neutral condition and the Williams %R at 70.710 suggests sell condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $281.13, a high of $500.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- Severe Valuation Stretching and Analyst Downgrades: Following an aggressive year-to-date rally, New Street Research recently downgraded Arm from Buy to Neutral, warning that its trailing P/E multiple exceeding 470x and forward P/E over 100x are fundamentally unsustainable. This extreme valuation premium has left the stock highly sensitive to profit-taking, causing a steep decline of over 15% in recent sessions.

- Ecosystem Friction and Channel Conflict: Arm's aggressive pivot into designing its own proprietary custom silicon processors (including its new 136-core AGI CPU) introduces direct channel conflict. Core licensing partners—including Apple, Qualcomm, NVIDIA, and AWS—may increasingly view Arm as a hardware competitor rather than a neutral, high-margin architecture licensor.

- Active FTC Antitrust Investigation and Legal Headwinds: The company faces intensifying regulatory scrutiny, driven by an ongoing U.S. Federal Trade Commission (FTC) probe into whether Arm is trying to illegally monopolize the semiconductor market by refusing or degrading the quality of CPU blueprint licenses for competing third-party chipmakers. This is coupled with the looming, high-stakes Qualcomm/Nuvia contract litigation set for late 2026.

- Operating Margin Compression: Despite strong revenue growth, Arm’s operating margins compressed from 52.8% to 49.1%. This margin pressure is driven by a massive 43% surge in research and development spending (jumping to $1.911 billion) to fund the execution and scaling of its standalone AGI CPU hardware roadmap.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.