Marvell Technology Inc Stock (MRVL) Moved Up by 7.00% on Jun 30: Facts Behind the Movement

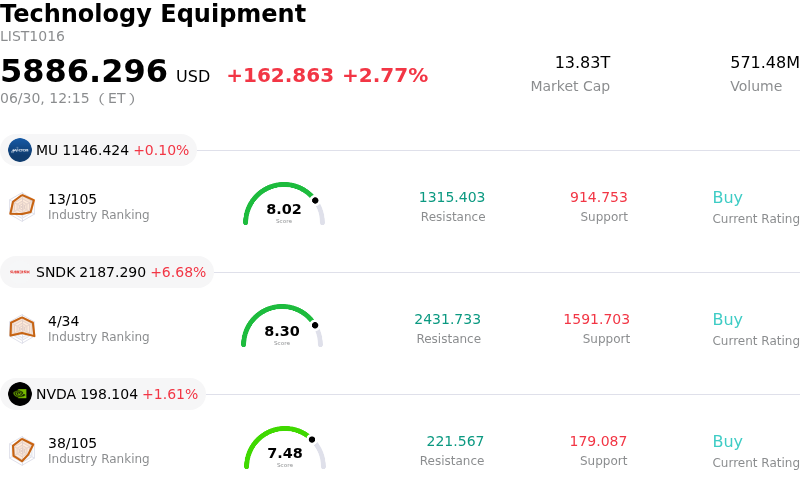

Marvell Technology Inc (MRVL) moved up by 7.00%. The Technology Equipment sector is up by 2.77%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 0.19%; SanDisk Corporation (SNDK) up 6.68%; NVIDIA Corp (NVDA) up 1.66%.

What is driving Marvell Technology Inc (MRVL)’s stock price up today?

The upward movement in Marvell Technology shares is primarily driven by a highly bullish analyst update from UBS, which has reignited market enthusiasm for the company’s advanced data center and artificial intelligence capabilities. UBS raised its price target on the stock significantly from $230 to $340 while keeping a Buy rating, highlighting Marvell’s strategic positioning to dominate the rapidly growing Compute Express Link market.

Compute Express Link is a crucial data infrastructure technology designed to facilitate efficient, high-speed connectivity between processors and memory within dense AI server racks. According to UBS, the total addressable market for Compute Express Link is projected to reach $4.5 billion by 2027 and expand further to between $7 billion and $10 billion by 2030. Analysts project that Marvell is on track to secure approximately $1 billion in revenue from this technology in 2027 and $2 billion in 2028, largely supported by custom chip designs developed in collaboration with two prominent U.S. hyperscale cloud providers.

This specialized growth channel serves as an incredibly powerful expansion catalyst beyond the company's existing high-speed optical connectivity and custom silicon businesses. In response to these developments, UBS upgraded its full-year revenue projections for Marvell to $16.8 billion for 2027 and $23.9 billion for 2028, bolstering investor confidence in the long-term sustainability of the firm's growth.

The positive sentiment is further supported by solid fundamental backing and ongoing sector-wide tailwinds. Investors are increasingly viewing Marvell as a primary beneficiary of the ongoing AI infrastructure wave, particularly following its high-profile collaborations with major players and its recent addition to the S&P 500 index on June 22. Although the stock experienced some technical profit-taking and volatility immediately following the index inclusion, today’s major target price increase from UBS has effectively refocused market attention on Marvell’s substantial long-term earnings potential and its strategic role in next-generation data centers.

Technical Analysis of Marvell Technology Inc (MRVL)

Technically, Marvell Technology Inc (MRVL) shows a MACD (12,26,9) value of -11.807, indicating a neutral signal. The RSI at 55.103 suggests neutral condition and the Williams %R at 60.701 suggests sell condition. Please monitor closely.

Fundamental Analysis of Marvell Technology Inc (MRVL)

Marvell Technology Inc (MRVL) is in the Technology Equipment industry. Its latest annual revenue is $8.19B, ranking 18 in the industry. The net profit is $2.67B, ranking 12 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $243.18, a high of $385.00, and a low of $90.00.

More details about Marvell Technology Inc (MRVL)

Company Specific Risks:

- Large-Scale Insider Equity Divestment: Outgoing CFO Willem Meintjes filed a Form 144 to liquidate 211,329 shares (representing roughly 48% of his direct equity holdings) valued at approximately $60.1 million near the stock's historical highs, triggering negative market sentiment and downward pressure.

- Financial Leadership Transition Vulnerabilities: The sudden transition of the Chief Financial Officer role from Willem Meintjes to Dan Durn introduces operational and supply chain integration risks at a critical juncture of capital scaling and complex manufacturing for next-generation custom AI chipsets.

- Extreme Valuation and Lack of Margin of Safety: Trading at a trailing P/E ratio of over 95x and a forward P/E of approximately 91x, the company is valued significantly above its historical benchmarks (a 203% premium to its 5-year median P/E), leaving the stock highly vulnerable to sharp technical reversals on any execution slips.

- Severe Customer and Sector Concentration: The company's top ten cloud hyperscaler customers account for approximately 82% of its total net revenue, exposing its custom XPU and data center connectivity pipeline to severe disintermediation risks if key clients shift toward in-house vertical chip designs.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.