Applied Materials Inc Stock (AMAT) Moved Up by 3.54% on Jun 30: A Full Analysis

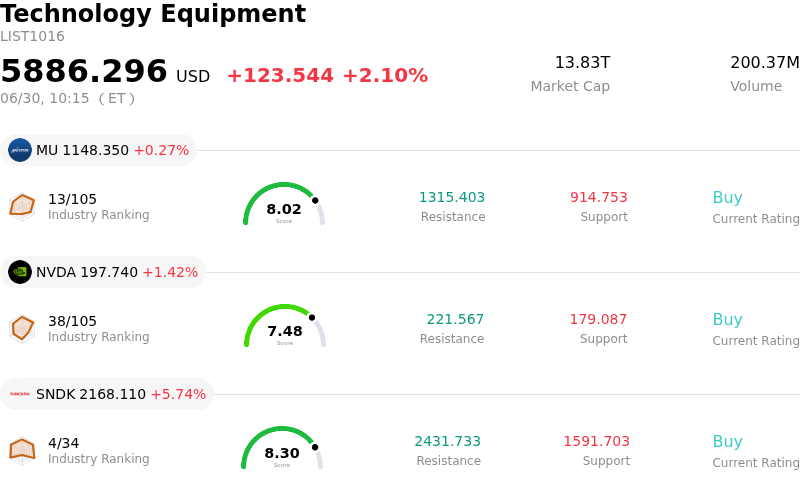

Applied Materials Inc (AMAT) moved up by 3.54%. The Technology Equipment sector is up by 2.10%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 0.27%; NVIDIA Corp (NVDA) up 1.48%; SanDisk Corporation (SNDK) up 5.51%.

What is driving Applied Materials Inc (AMAT)’s stock price up today?

Applied Materials experienced upward price movement today following a wave of positive catalyst revisions from major Wall Street institutions, which boosted investor confidence and offset recent profit-taking pressures in the technology sector.

The primary driver of the upward momentum is a series of significant price target increases from top financial analysts. Over the past twenty-four hours, several prominent investment firms aggressively revised their forecasts upward, reflecting a highly bullish outlook on the semiconductor equipment sector. Notably, Cantor Fitzgerald raised its target price to $850, highlighting strong positioning alongside peer companies in wafer fabrication. KeyBanc Capital Markets also adjusted its target price substantially higher to $750, pointing to the structural durability of the ongoing artificial intelligence capital expenditure cycle as a critical tailwind. Analysts emphasize that the hardware demands of high-performance computing, advanced packaging, and generative AI workloads will drive sustained investment in next-generation chipmaking technologies.

Furthermore, institutional support was bolstered by recent earnings estimate upward revisions from Erste Group Bank, signaling that the broader street expects the company's fiscal performance to strengthen significantly over the next two years. This analytical optimism follows the company's recent product introductions targeted directly at resolving the AI "memory wall" by modernizing dynamic random-access memory and advanced chip packaging processes.

In addition to fundamental and analytical upgrades, technical and structural factors have supported the upward trend. The stock's recent inclusion in the Russell Top 50 Index has generated steady index-tracking inflows, prompting passive funds and institutional managers to increase their portfolio allocations toward the stock.

However, despite today's positive price action, the stock continues to experience elevated intraday volatility. This behavior reflects an ongoing market debate over valuation, with some market participants warning that the current premium trading multiple relative to historical averages may limit near-term upside. Concerns persist regarding recent executive selling and potential capacity realignments by major global memory manufacturers, which can inject rapid shifts in sector momentum. Nonetheless, today's heavy analytical support and strong long-term growth narrative in the AI hardware value chain have firmly placed buyers in control.

Technical Analysis of Applied Materials Inc (AMAT)

Technically, Applied Materials Inc (AMAT) shows a MACD (12,26,9) value of 17.586, indicating a buy signal. The RSI at 70.191 suggests buy condition and the Williams %R at 5.918 suggests overbought condition. Please monitor closely.

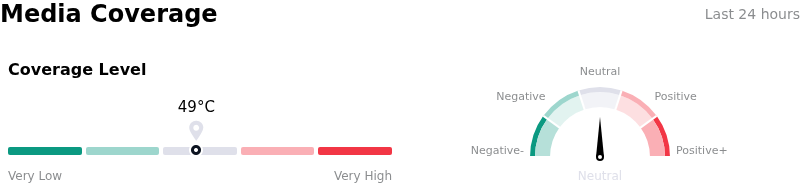

Media Coverage of Applied Materials Inc (AMAT)

In terms of media coverage, Applied Materials Inc (AMAT) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Applied Materials Inc (AMAT)

Applied Materials Inc (AMAT) is in the Technology Equipment industry. Its latest annual revenue is $28.37B, ranking 10 in the industry. The net profit is $7.00B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $570.07, a high of $900.00, and a low of $308.00.

More details about Applied Materials Inc (AMAT)

Company Specific Risks:

- Downstream Memory Capex Moderation: Industry reports indicating that major memory manufacturers like SK Hynix are moderating High-Bandwidth Memory (HBM) expansion present an immediate threat to the company's mid-term order pipeline. Because Applied Materials is heavily exposed to DRAM and NAND flash deposition, etching, and process control tools, downstream capital spending deceleration among key Asian chipmakers risks creating a tool oversupply.

- Aggressive and Concentrated Insider Liquidations: Recent SEC Form 4 and Form 144 filings from late June 2026 reveal heavy executive de-risking, totaling over $114 million in insider stock sales over the last three months with zero purchasing activity. This massive selling pressure—headlined by CEO Gary Dickerson's $42.5 million liquidation, SVP/CTO Omkaram Nalamasu's $14.4 million sale, and Semiconductor Products Group President G. Raja Prabu's $25.3 million sale—signals that corporate leadership perceives the stock's current price to be at a near-term valuation ceiling.

- Extreme Valuation and Multiple Compression Risk: Following intense AI-driven speculation and a rapid price surge, AMAT's trailing P/E ratio has expanded past 65x, representing a massive premium over its 5-year median P/E of 20.4x. This substantial overvaluation leaves the stock highly vulnerable to sharp multiple compression and profit-taking in the event of macroeconomic shocks, rising Treasury yields, or a broader reassessment of near-term AI spending.

- High Embedded Expectations and Consensus Lag: Despite recent product showcases for DRAM and packaging, market analysts warn that excessively high expectations are embedded in the current valuation, creating significant downside risk if upcoming Q3 2026 earnings or guidance fall short. Furthermore, the broader analyst consensus target of approximately $541 to $552 sits well below the current trading range, highlighting a substantial disconnect between the stock's parabolic climb and the average institutional valuation model.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.