Intel Corp Stock (INTC) Moved Up by 3.76% on Jun 30: Facts Behind the Movement

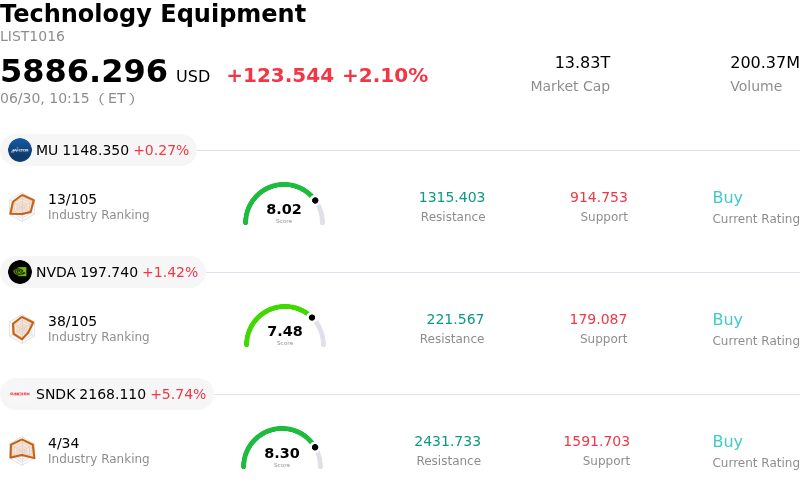

Intel Corp (INTC) moved up by 3.76%. The Technology Equipment sector is up by 2.10%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 0.27%; NVIDIA Corp (NVDA) up 1.48%; SanDisk Corporation (SNDK) up 5.51%.

What is driving Intel Corp (INTC)’s stock price up today?

Intel Corporation shares rallied on Tuesday, demonstrating notable upward momentum amid a broader climate of heightened intraday volatility. The primary driver behind this positive performance is a wave of optimistic adjustments from Wall Street analysts, which has significantly bolstered investor sentiment.

A key catalyst for the advance was a major price-target revision from Cantor Fitzgerald. The firm raised its target on the chipmaker to one hundred and fifty dollars, citing the generational buildout of artificial intelligence infrastructure as a durable and extended cycle. This bullish outlook highlights the company's competitive positioning in the compute and accelerator sectors. The upgrade reinforces a growing consensus that the company’s structural turnaround, specifically its pivot toward AI-capable silicon and domestic foundry services, is increasingly credible.

Furthermore, the company recently highlighted its ongoing domestic manufacturing and packaging leadership. These strategic moves have been supported by significant regulatory tailwinds and preliminary manufacturing partnerships, including a landmark deal to produce tensor processing units for Google and integration into next-generation accelerator hardware. Traders also pointed to positive technical indicators, noting that the stock has held firmly above key moving averages, signaling strong institutional inflows and buying momentum.

However, the day's trading was characterized by significant intraday volatility. While the dominant narrative remains optimistic, some market participants remain cautious due to valuation concerns. Traditional metrics show the stock trading at a premium relative to its semiconductor peers, and some analysts warn that the actual revenue and margin contributions from the advanced process nodes are still a few years away. Despite these underlying structural debates and occasional profit-taking, the combination of influential Wall Street upgrades and positive long-term AI-related manufacturing catalysts successfully drove the stock upward.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of 0.563, indicating a buy signal. The RSI at 58.830 suggests neutral condition and the Williams %R at 23.172 suggests buy condition. Please monitor closely.

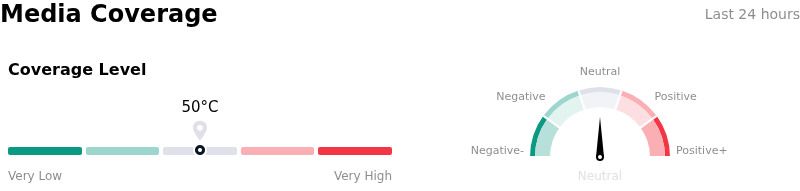

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 50, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $94.77, a high of $160.00, and a low of $25.00.

More details about Intel Corp (INTC)

Company Specific Risks:

- Overextended Valuation and Limited Safety Margin: Following recent Wall Street coverage initiations, analysts have flagged that the stock's massive rally has stretched its forward price-to-earnings (P/E) ratio to a premium of over 113x–121x. This extreme valuation leaves virtually no margin of safety for investors, especially when competitors like NVIDIA and AMD offer stronger revenue visibility at comparable multiples.

- Margin Dilution and Sub-Profitable Foundry Yields: While Intel’s next-generation 18A-P process node has officially entered its risk production phase, industry research indicates that current manufacturing yields remain below the 50% profitable commercial threshold. Reaching commercial-scale profitability on these advanced nodes is delayed until late 2026 or 2027, exposing the company to near-term margin dilution and heightened execution risks.

- Severe Capital Strain from Unprofitable Operations: Intel's foundry segment remains heavily unprofitable, undercutting the broader business with a $2.4 billion operating loss and a negative free cash flow of $3.87 billion in its last quarterly reporting cycle. This structural cash drain forces heavy reliance on debt markets, illustrated by the issuance of $6.5 billion in high-interest senior notes and a $6.5 billion bridge loan utilized to repurchase Apollo's stake in Ireland's Fab 34.

- Ongoing CPU Market Share Erosion: Despite optimistic sentiment around custom-chip demand, institutional analysts maintain caution regarding the core processor landscape. The company continues to face accelerated market share loss to primary CPU competitors and alternative silicon designs in a mature personal computer and data center market.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.