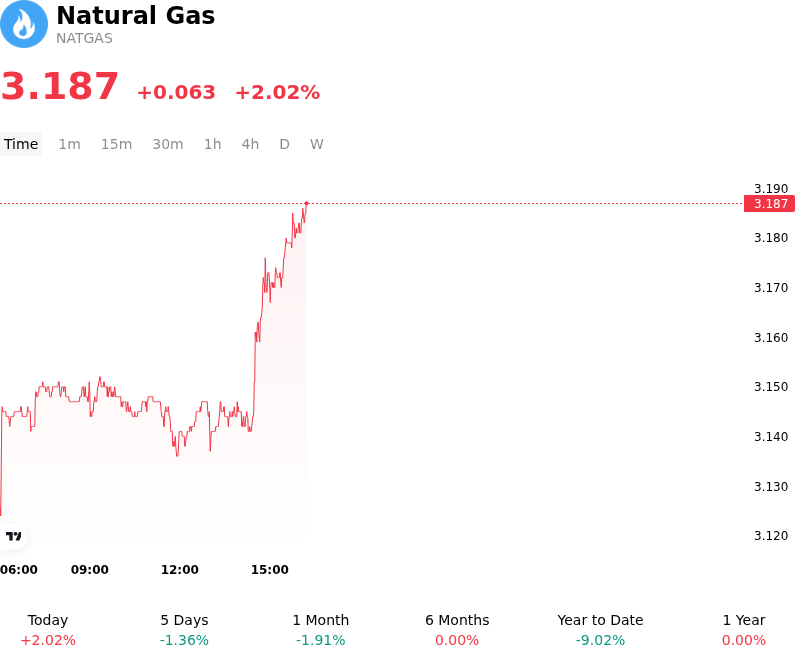

Natural Gas (NATGAS) Is up 2.02% on Jun 30: Key Drivers to Watch

Natural Gas (NATGAS) is up 2.02% at Jun 30 04:15(ET), now at $3.187, with a 7-day up of 0.89%.

What is driving Natural Gas (NATGAS)’s stock price up today?

The upward movement in natural gas prices is primarily driven by a robust reacceleration of weather-driven demand expectations. Near-term meteorological models predict an intense summer heat dome taking shape across major population centers in the eastern two-thirds of the United States, including the Midwest and Northeast. With temperatures forecast to hover in the upper 80s to over 100 degrees through early July, power sector demand for air-conditioning is expected to reach fresh seasonal highs. Because gas-fired generation accounts for approximately 40 percent of the U.S. electricity mix, this surge in cooling degree days has prompted a sharp repricing of short-term power-burn demand, tightening near-term domestic balances.

Complementing the domestic demand surge is the continued strength in liquefied natural gas (LNG) export fundamentals. Daily feedgas flows to major U.S. Gulf Coast export terminals have remained highly resilient, averaging over 17 billion cubic feet per day throughout June. This structural demand is further amplified by geopolitical disruptions in global markets. Geopolitical tensions in the Middle East have resulted in reduced LNG loadings, with notable long-term infrastructure damage to key facilities like Qatar's Ras Laffan plant. Additionally, shipping bottlenecks through the Strait of Hormuz have significantly curtailed LNG shipments to Europe and Asia. This global supply squeeze has kept European gas storage well below historical averages, keeping global spot prices elevated and fueling strong, continuous demand for U.S. exports.

On the supply side, domestic dry gas production has stabilized after spring maintenance, with Lower 48 output holding steady around 110 billion cubic feet per day. While these production levels reflect a comfortable supply cushion, the market has shrugged off bearish supply narratives as recent weekly storage injections have tracked near seasonal norms. Although overall U.S. inventories remain roughly 5.7 percent above the five-year average, the rapid expansion of summer power-burn demand and steady LNG export pull are expected to accelerate storage withdrawals, or at least significantly limit the pace of further injections, keeping the market balanced.

From a broader structural standpoint, the commodity continues to trade within an established ascending channel, supported by the ongoing build-out of pipeline infrastructure, such as West Texas takeaway projects that have helped resolve previous regional bottlenecks. While short-term profit-taking and contract rollovers can introduce brief periods of volatility, the underlying fundamentals of high power-sector utilization, accelerating global LNG demand, and impending peak summer heat continue to establish a firmer price floor. Investors remain highly sensitive to any weather model revisions and upcoming inventory reports, which will dictate whether the current bullish momentum can be sustained into late summer.

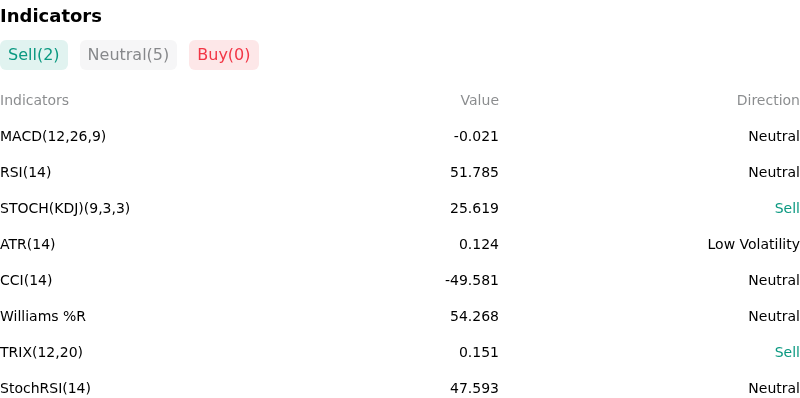

Technical Analysis of Natural Gas (NATGAS)

Technically, Natural Gas (NATGAS) shows a MACD (12,26,9) value of -0.021, indicating a neutral signal. The RSI at 51.785 suggests neutral condition and the Williams %R at 54.268 suggests neutral condition. Please monitor closely.

More details about Natural Gas (NATGAS)

Recent Events and Risks:

- Retreating Futures Prices and Technical Selling: U.S. natural gas futures fell for a second consecutive session, dropping 2.5% to $3.20/MMBtu as the market retreated from its recent peak of $3.44/MMBtu. Technical indicators show the prompt-month contract is losing upward momentum, exposing futures to potential long liquidation and testing key downside support levels at $3.15 and $2.92.

- Unabated Domestic Production: Lower-48 dry gas production remains near record levels, averaging 110.6 to 112.0 Bcf/d (a 3.4% year-over-year increase). This persistent supply growth is heavily driven by associated gas output from Permian Basin oil drilling, creating a high supply baseline that continues to outpace demand.

- Persistently High Storage Surplus: Domestic working gas inventories remain structurally elevated at 2,835 Bcf, which is 152 Bcf (nearly 6%) above the five-year historical average. The latest larger-than-expected weekly storage build of 76 Bcf indicates that overall supply remains highly comfortable, minimizing the likelihood of a near-term supply squeeze.

- Weather Revisions and Renewable Displacement: Despite current regional heat, meteorologists warn that the midsummer heat dome may be short-lived, with temperatures projected to cool back to normal. Additionally, robust electricity generation from renewable energy sources (wind and solar) in the Northeast and Midwest is displacing gas-fired power burn, preventing spot prices from sustaining upward momentum.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.