Arm Holdings PLC Stock (ARM) Moved Down by 3.22% on Jun 24: Key Drivers Unveiled

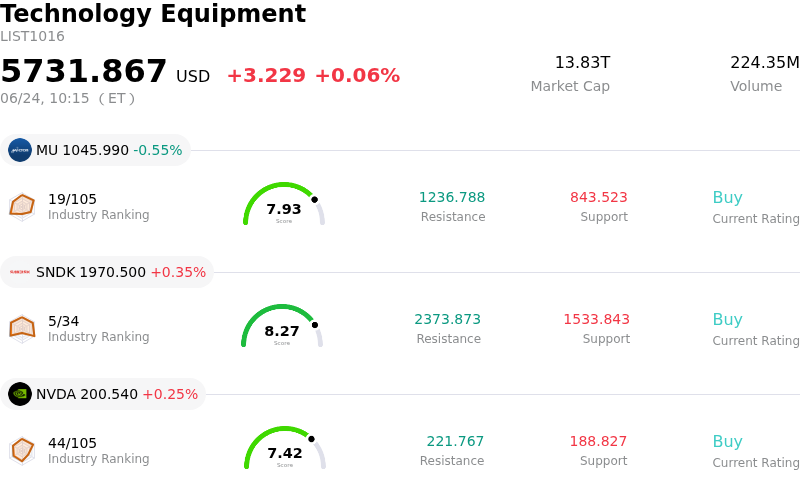

Arm Holdings PLC (ARM) moved down by 3.22%. The Technology Equipment sector is up by 0.06%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 0.55%; SanDisk Corporation (SNDK) up 0.35%; NVIDIA Corp (NVDA) up 0.25%.

What is driving Arm Holdings PLC (ARM)’s stock price down today?

The downward pressure on Arm Holdings on Wednesday is a result of a sharp struggle between massive long-term bullish catalysts and a broader, sentiment-driven pullback across the technology and semiconductor sectors. After starting the day with strong premarket momentum fueled by positive commentary from its parent company leadership and major Wall Street upgrades, the stock ultimately succumbed to sector-wide de-risking and profit-taking. This highlights the heightened sensitivity of highly valued artificial intelligence beneficiaries in the current market environment.

Early in the session, positive momentum was catalyzed by highly bullish comments from SoftBank Group CEO Masayoshi Son during the company's annual shareholder meeting. Son expressed extreme confidence in the chip designer, predicting that its valuation could grow tenfold over the next decade as AI computing increasingly shifts toward central processing unit-centric architectures. Adding to the enthusiasm, major investment banks issued substantial price target upgrades. UBS lifted its target significantly, highlighting Arm's core competency in latency and efficiency aligning with hyperscaler needs, while TD Cowen also raised its price target, pointing to accelerating demand for central processing units driven by agentic AI adoption.

Despite these strong endorsement signals, the stock reversed course due to overriding macroeconomic and sector-level headwinds. A broader global tech rout has recently weighed on high-growth technology and semiconductor stocks. Investors are increasingly concerned about potential interest rate adjustments and tighter monetary policies, which disproportionately pressure companies trading at extreme valuation premiums. With Arm trading at highly elevated trailing and forward earnings multiples, investors are exceptionally sensitive to any signs of valuation stretching. The recent rating downgrade by New Street Research to neutral served as a warning of these valuation limits, prompting institutional investors to take profits and rebalance portfolios.

Ultimately, the significant intraday volatility illustrates the ongoing tension between Arm's strong business narrative—solidified by its expanding role in custom silicon and data center CPUs—and its steep market valuation. While the underlying demand for the company's IP and its long-term growth prospects remain robust, short-term trading is currently dominated by macroeconomic anxieties, sector rotation, and profit-taking across the semiconductor space.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of -4.729, indicating a neutral signal. The RSI at 54.003 suggests neutral condition and the Williams %R at 55.929 suggests sell condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $269.13, a high of $500.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- Extreme Valuation Premium and Analyst Downgrades: Following an aggressive year-to-date rally, New Street Research downgraded ARM from Buy to Neutral, warning that its trailing P/E ratio exceeding 480x and forward multiple over 100x are fundamentally unsustainable. This extreme valuation premium leaves the high-beta stock with zero margin for error, triggering severe profit-taking and intraday downside volatility during the broader semiconductor sector pullbacks.

- Ecosystem Friction and Channel Conflict: ARM’s strategic pivot into developing and selling its own proprietary custom silicon (including its new co-developed 136-core AGI CPU) introduces severe channel conflict. Core licensing partners like Nvidia, Apple, Qualcomm, and AWS may increasingly view ARM as a hardware competitor rather than a neutral technology partner, threatening the long-term viability of ARM's core high-margin IP licensing business model.

- Intensifying Antitrust and Regulatory Scrutiny: Regulators are actively investigating ARM's licensing practices. The probes are specifically examining whether the company's expansion into proprietary hardware and production silicon will lead to anti-competitive behavior, such as degrading or denying CPU design blueprints to third-party chipmakers who compete with ARM's physical hardware.

- Substantial Executive Insider Liquidations: Market sentiment has been weighed down by consecutive, multi-million dollar open-market share sales by senior company executives—including the Chief Commercial Officer, Chief Accounting Officer, and Chief People Officer—throughout late May and June 2026. These coordinated liquidations have signaled to institutional investors that insiders may view the current stock price as a peak valuation level.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.