Intel Corp Stock (INTC) Moved Up by 10.64% on Jun 21: What Investors Need To Know

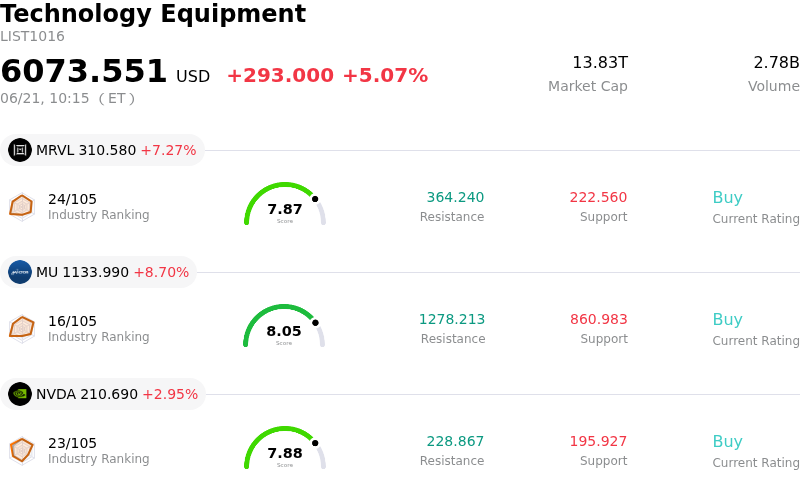

Intel Corp (INTC) moved up by 10.64%. The Technology Equipment sector is up by 5.07%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Marvell Technology Inc (MRVL) up 7.27%; Micron Technology Inc (MU) up 8.70%; NVIDIA Corp (NVDA) up 2.95%.

What is driving Intel Corp (INTC)’s stock price up today?

Intel Corporation (INTC) experienced a strong upward move, driven by a series of high-profile developments that bolstered investor confidence in its foundry business and long-term artificial intelligence growth. The primary catalyst was a major political and industry announcement indicating a potential strategic collaboration with Apple to design and manufacture chips domestically in the United States. This news, which highlighted the growing push for domestic chip fabrication and the U.S. government's vested interest through its equity stake in Intel, generated immense speculative momentum and propelled the stock to new heights.

Beyond speculation, Intel's technical milestones have provided solid fundamental backing for its turnaround strategy. The company officially announced that its next-generation Intel 18A-P process node has entered the risk production phase on schedule. This follows reports of massive customer commitments, including Google ordering millions of Tensor Processing Units (TPUs) for future production and ongoing evaluations by other major chip designers like Nvidia. These concrete developments showcase Intel's growing competitive stance against global foundry giants, signaling that its transition from a traditional chip designer to a commercial foundry is gaining real operational traction.

On the operational front, Intel announced a strategic leadership transition within its critical foundry division. The appointment of a new executive vice president to lead advanced packaging and system integration is expected to streamline back-end manufacturing and accelerate the commercialization of cutting-edge nodes. This leadership update coincides with robust demand forecasts for computing infrastructure, particularly in agentic artificial intelligence and enterprise server inference workloads. The shift from training-heavy AI to inference workloads represents a massive, multi-year tailwind for Intel's server and data center divisions, which have already shown accelerating revenue growth.

From a market perspective, the sudden surge triggered a wave of technical buying and short-covering as the stock broke through major long-term resistance levels. However, institutional analysts and market strategists maintain a degree of caution. Despite the positive news flow, Intel's foundry segment remains unprofitable with a projected breakeven timeline delayed to next year. Furthermore, with the Apple manufacturing partnership still unconfirmed by either company, some market players warn that the stock's valuation has become stretched, leaving it susceptible to near-term options hedging and speculative volatility.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of 1.364, indicating a buy signal. The RSI at 64.208 suggests neutral condition and the Williams %R at 4.011 suggests overbought condition. Please monitor closely.

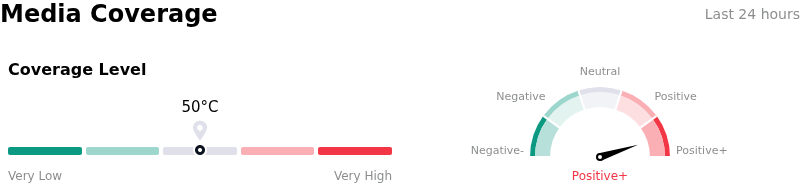

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 50, indicating a moderate level of media attention. The overall market sentiment index is currently in extremely bullish zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $91.92, a high of $150.00, and a low of $25.00.

More details about Intel Corp (INTC)

Company Specific Risks:

- Unconfirmed Partnership Hype and Contract Execution Risk: The stock’s recent surge was triggered by social media announcements of an Apple partnership to manufacture chips domestically, yet neither Apple nor Intel has formally confirmed the deal. The lack of signed, binding commitments introduces substantial downside risk if the scope of the agreement is narrower than expected or fails to translate into near-term revenue.

- Extreme Valuation Multiples and Consensus Downgrades: Driven by an aggressive turnaround rally, Intel trades at an elevated forward P/E ratio of over 111x–133x, severely disconnected from institutional consensus price targets of $82–$93. Analysts have flagged this valuation gap, with major institutions like Bank of America maintaining Underperform ratings, warning of a potential sharp correction.

- Persistent Foundry Losses and Margin Dilution: Intel’s Foundry Services (IFS) division remains structurally unprofitable, suffering a $2.4 billion operating loss and contributing to a $3.87 billion negative free cash flow in Q1 2026. Despite the advanced 18A-P node entering risk production, profitable manufacturing yields are not projected until late 2026, posing an ongoing threat of margin erosion and balance sheet strain.

- Market Share Erosion and Competitive Threats: Intel faces intensifying competition in its highest-margin segments, notably with AMD capturing a 33% server CPU market share in Q1 2026. Additionally, the rapid rise of custom ARM-based processors from cloud hyperscalers and NVIDIA's entry into PC processors threaten Intel’s core market share and premium AI PC positioning.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.