KLA Corp Stock (KLAC) Moved Up by 8.73% on Jun 20: Key Drivers Unveiled

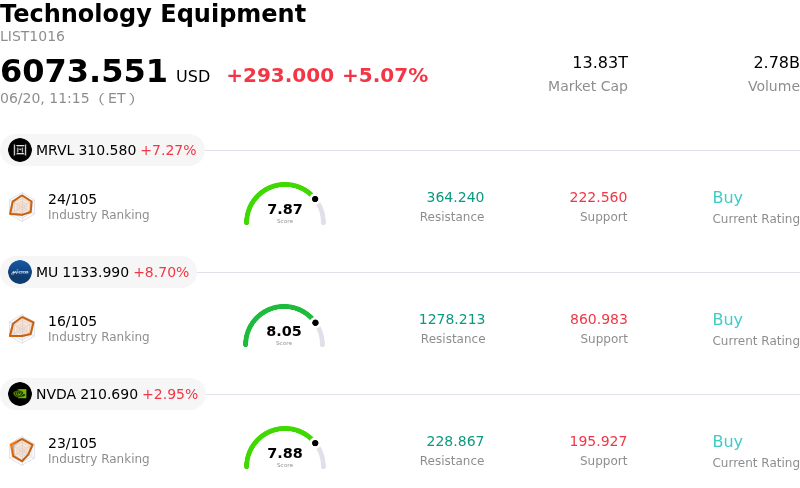

KLA Corp (KLAC) moved up by 8.73%. The Technology Equipment sector is up by 5.07%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Marvell Technology Inc (MRVL) up 7.27%; Micron Technology Inc (MU) up 8.70%; NVIDIA Corp (NVDA) up 2.95%.

What is driving KLA Corp (KLAC)’s stock price up today?

KLA Corporation has experienced pronounced intraday volatility following a series of technical, macro, and fundamental developments. A key catalyst for the stock's recent price action was the execution of its highly anticipated ten-for-one forward stock split. While the stock split improved trading liquidity and retail accessibility without changing the underlying fundamentals, it initially triggered a wave of profit-taking. High-profile insider selling and a surge in defensive options hedging contributed to a brief technical correction. However, this downward momentum was quickly reversed as institutional investors recognized a buying opportunity, viewing the dip as a tactical entry point into a structurally vital player in the artificial intelligence supply chain.

The primary driver of the sharp upward trajectory was a flurry of positive analyst updates and price target adjustments. Prominent Wall Street firms, including Citigroup, Cantor Fitzgerald, and Barclays, raised their post-split valuation models for KLA. Analysts pointed to upward revisions in global wafer fabrication equipment spending, supported by multi-year capital expenditure projections from hyperscale cloud providers. The accelerating deployment of agentic artificial intelligence is shifting the technical requirements for memory and logic chips, increasing process complexity. This trend places KLA's leading-edge process control and metrology tools in high demand, as chipmakers are forced to prioritize yield management in advanced packaging nodes.

Broader market dynamics also played a critical role in fueling KLA's intraday gains. The wider technology and semiconductor sectors received a significant boost following eased geopolitical tensions, specifically the signing of an interim agreement that promised to reopen the Strait of Hormuz. This development cooled global inflation fears, triggered a slide in oil prices, and sparked a massive relief rally across tech equities. Furthermore, positive domestic headlines regarding collaborative chip design and domestic manufacturing initiatives injected additional optimism into the US semiconductor ecosystem. This rising tide lifted KLA, which remains a cornerstone of domestic manufacturing capabilities.

On the technical front, KLA's stock entered oversold territory following its post-split sell-off, prompting quantitative and momentum-driven trading systems to trigger buy signals. The recovery was further amplified by the quarterly expiration of derivative contracts, known as triple witching, which coincided with exceptionally heavy trading volume. This event naturally heightened intraday price swings as market makers adjusted their hedging books. Supported by an active multi-billion-dollar share repurchase program, KLA's strong operational foundation and robust revenue visibility through the latter half of the year continue to attract institutional backing, driving a substantial recovery in its market valuation despite underlying concerns regarding near-term multiple premiums.

Technical Analysis of KLA Corp (KLAC)

Technically, KLA Corp (KLAC) shows a MACD (12,26,9) value of -402.481, indicating a sell signal. The RSI at 19.618 suggests oversold condition and the Williams %R at 98.132 suggests oversold condition. Please monitor closely.

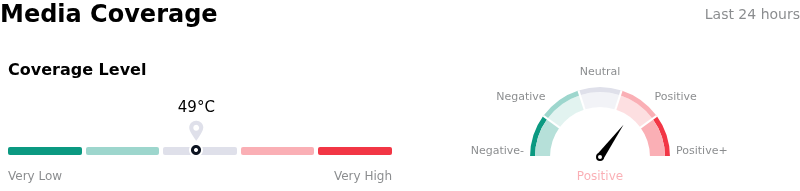

Media Coverage of KLA Corp (KLAC)

In terms of media coverage, KLA Corp (KLAC) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of KLA Corp (KLAC)

KLA Corp (KLAC) is in the Technology Equipment industry. Its latest annual revenue is $12.16B, ranking 15 in the industry. The net profit is $4.06B, ranking 11 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $196.47, a high of $290.00, and a low of $138.80.

More details about KLA Corp (KLAC)

Company Specific Risks:

- Stretched Post-Split Valuation Premium: Following its recent 10-for-1 stock split, KLAC's valuation has ballooned to over 70x trailing earnings, representing a massive premium relative to its historical median P/E of 26.0x. This extreme multiple leaves no room for operational error and has triggered aggressive institutional profit-taking, causing the stock to tumble nearly 9.5% from its post-split high of $267.17.

- Unprecedented Surge in Bearish Options Activity: Market data reveals a massive spike in defensive positioning, with traders accumulating 39,161 put contracts in a single session—representing a 1,456% increase over the daily historical average. This sudden wave of bearish derivatives activity indicates a sharp rise in investor expectations for a deeper near-term price correction.

- Significant Executive and Insider Divestments: Public disclosures showing $19.7 million in insider selling over the past three months have damaged market sentiment. This includes a prominent $10 million stock liquidation by CEO Richard P. Wallace, prompting concerns among institutional investors regarding the stock's near-term valuation ceiling.

- Geopolitical Export Restraints and Margin Pressures: Tightening governmental export controls targeting advanced semiconductor equipment shipments to China are expected to drag heavily on top-line growth, threatening to forfeit an estimated $300 million to $350 million in annual revenue. Additionally, rising input costs from memory component inflation are projected to compress gross margins by roughly 100 basis points.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.