Vertiv Holdings Co Stock (VRT) Closed Down by 3.85% on Jun 16: Drivers Behind the Movement

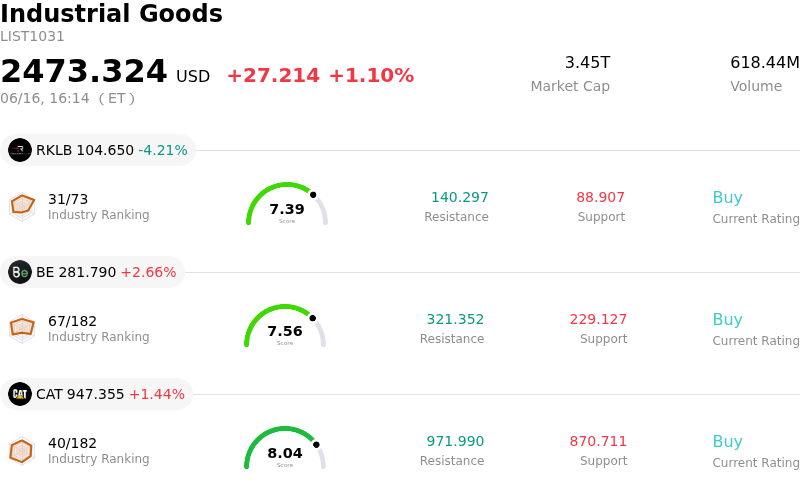

Vertiv Holdings Co (VRT) closed down by 3.85%. The Industrial Goods sector is up by 1.10%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Rocket Lab USA Inc (RKLB) down 4.21%; Bloom Energy Corp (BE) up 2.66%; Caterpillar Inc (CAT) up 1.44%.

What is driving Vertiv Holdings Co (VRT)’s stock price down today?

The intraday volatility and downward pressure on Vertiv Holdings Co. reflect a broader reassessment of high-flying artificial intelligence infrastructure stocks, as investors weigh the company's stellar growth against its premium valuation and specific regional execution risks. Despite the company's strong position in the AI data center cooling and power management market, the stock has experienced heightened sensitivity as market participants evaluate whether the current price fully incorporates both near-term tailwinds and potential headwinds.

A primary driver of the downward movement is profit-taking and multiple compression following an extraordinary rally. Vertiv trades at a highly elevated price-to-earnings multiple, which places immense pressure on the company to execute flawlessly. While the overall demand for high-density computing and advanced thermal solutions remains incredibly strong, some analysts and investors are growing cautious that consensus expectations for out-year margins may be overly optimistic. With a high beta, the stock naturally magnifies any macro-driven swings or rotation away from premium-valued industrial tech names, leading to sharp, sudden drawdowns.

The tension is further compounded by localized execution risks, particularly within the Europe, Middle East, and Africa (EMEA) segment. While Vertiv’s Americas segment has demonstrated robust growth, EMEA revenues experienced a steep year-over-year decline in the first quarter of the year. Management has projected a major acceleration and recovery in the EMEA region for the second half of the year, which is crucial for achieving their raised full-year guidance. However, this heavy reliance on a back-half turnaround introduces significant execution uncertainty, giving some investors pause before committing further capital at these elevated multiples.

In addition to these structural concerns, technical factors such as the stock recently passing its ex-dividend date on June 15 have contributed to the downward drift. While strategic moves like the completed acquisition of ThermoKey S.p.A. and the launch of new AI-driven cooling services reinforce the long-term bull case, they also underscore the capital-intensive nature of sustaining such rapid scaling. Ultimately, the high concentration of Vertiv’s growth in the capital expenditure cycles of massive hyperscalers means that any macro wobble or perceived pause in AI infrastructure spending carries outsized risks of rapid multiple compression, prompting tactical downside moves and sharp intraday volatility.

Technical Analysis of Vertiv Holdings Co (VRT)

Technically, Vertiv Holdings Co (VRT) shows a MACD (12,26,9) value of -5.305, indicating a sell signal. The RSI at 48.700 suggests neutral condition and the Williams %R at 47.500 suggests neutral condition. Please monitor closely.

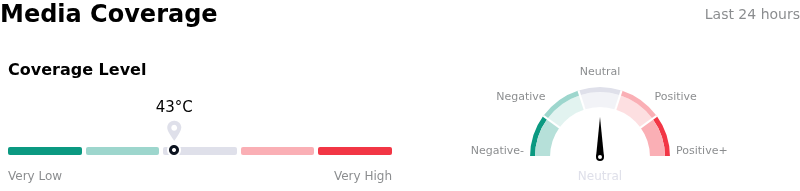

Media Coverage of Vertiv Holdings Co (VRT)

In terms of media coverage, Vertiv Holdings Co (VRT) shows a coverage score of 43, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Vertiv Holdings Co (VRT)

Vertiv Holdings Co (VRT) is in the Industrial Goods industry. Its latest annual revenue is $10.23B, ranking 17 in the industry. The net profit is $1.33B, ranking 13 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $361.33, a high of $500.00, and a low of $112.00.

More details about Vertiv Holdings Co (VRT)

Company Specific Risks:

- **Premium Valuation & Hyperscaler Capex Sensitivity:** Trading at a demanding multiple of approximately 70x–78x trailing earnings, Vertiv's stock remains highly sensitive to shifts in market sentiment. Market analysts have expressed concern that a projected slowdown in capital expenditure growth by hyperscale data center operators in 2027 could trigger severe multiple compression and downward valuation pressure.

- **Severe Regional Growth Deceleration in EMEA:** While global metrics remain elevated, Vertiv's latest quarterly financials showed a stark 20.3% year-over-year revenue decline in Europe, the Middle East, and Africa (EMEA), with organic sales plunging 29.4%. This deep geographic contraction represents a major vulnerability to the company's international growth expectations.

- **Operational Expansion and Backlog Execution Hurdles:** To satisfy its unprecedented $15.0 billion backlog, Vertiv must rapidly scale its manufacturing capabilities. Analysts warn that assuming a frictionless capacity expansion carries high operational and execution risks, as any regional supply chain disruptions or factory bottlenecks will impair the company’s ability to convert orders into realized revenue.

- **Integration Risks of the ThermoKey Acquisition:** Following the official closing of the ThermoKey S.p.A. acquisition disclosed in an 8-K filing on June 12, 2026, Vertiv faces immediate integration complexities. Merging the specialized European heat-exchange supplier's manufacturing facilities and proprietary liquid-cooling technology into Vertiv's existing global footprint introduces execution risks and near-term capital expenditure overhead.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.