SanDisk Corporation Stock (SNDK) Moved Down by 3.30% on Jun 16: What Signal Does It Send?

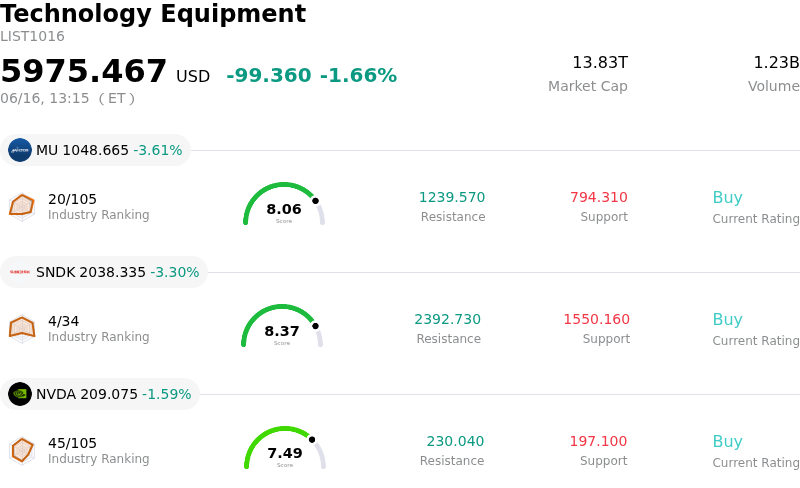

SanDisk Corporation (SNDK) moved down by 3.30%. The Technology Equipment sector is down by 1.66%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 3.62%; SanDisk Corporation (SNDK) down 3.30%; NVIDIA Corp (NVDA) down 1.59%.

What is driving SanDisk Corporation (SNDK)’s stock price down today?

SanDisk Corporation experienced notable downward pressure and significant intraday volatility as technical indicators and valuation debates triggered a wave of profit-taking. Despite the company’s recent operational triumphs, the stock has entered highly overbought territory after a parabolic, multi-month run following its spin-off. With momentum indicators such as the Relative Strength Index flashing historically rare extreme readings, a near-term correction was widely anticipated by market participants, leaving the stock vulnerable to rapid intraday reversals as traders locked in gains.

At the core of the market action is an intensifying debate over the sustainability of the current memory supercycle. On one side, the rapid deployment of artificial intelligence at the edge—running local AI models directly on smartphones and personal computers—continues to drive massive demand for high-capacity NAND storage. This trend is supported by robust sequential revenue growth and multi-year supply contracts that have locked up the company's production capacity. However, skeptical investors are increasingly questioning how long this favorable supply-demand bottleneck will last, particularly as some chipmakers hint at a potential easing of memory shortages in the coming years.

Furthermore, SanDisk’s profile as a pure-play NAND provider acts as a double-edged sword. Unlike some of its more diversified semiconductor peers, the company lacks exposure to high-bandwidth memory or DRAM markets. This pure-play focus exposes SanDisk directly to the highly cyclical pricing dynamics of the flash memory market. Concerns that current valuation levels are reflecting peak supercycle earnings have prompted some analysts to issue caution, warning that any future expansion in global NAND supply could compress margins and trigger a sharp downturn.

Ultimately, the decline and elevated volatility reflect a technical consolidation rather than a fundamental breakdown. The collision between overextended technical conditions and long-term cyclical anxieties has temporarily outweighed the persistent structural tailwinds of the AI-driven storage boom. As institutional investors realign their portfolios and reassess peak-valuation risks, SanDisk remains subject to sharp, volume-driven fluctuations.

Technical Analysis of SanDisk Corporation (SNDK)

Technically, SanDisk Corporation (SNDK) shows a MACD (12,26,9) value of 39.848, indicating a buy signal. The RSI at 73.883 suggests buy condition and the Williams %R at 1.988 suggests overbought condition. Please monitor closely.

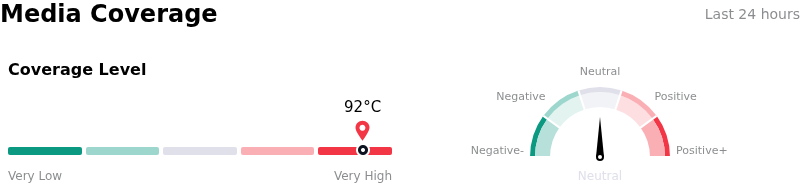

Media Coverage of SanDisk Corporation (SNDK)

In terms of media coverage, SanDisk Corporation (SNDK) shows a coverage score of 92, indicating a very high level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of SanDisk Corporation (SNDK)

SanDisk Corporation (SNDK) is in the Technology Equipment industry. Its latest annual revenue is $7.36B, ranking 10 in the industry. The net profit is $-1.64B, ranking 41 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1604.06, a high of $3250.00, and a low of $250.00.

More details about SanDisk Corporation (SNDK)

Company Specific Risks:

- Lack of DRAM and HBM Diversification: Since spinning off as a pure-play NAND flash memory provider, SanDisk lacks the broader product diversification of competitors who produce DRAM or High-Bandwidth Memory (HBM). Analysts warn that when industry-wide HBM demand normalizes, competitors will shift idle wafer capacity back to NAND, potentially triggering a rapid oversupply and severe pricing depreciation that SanDisk cannot offset.

- Heavy Operational Reliance and Commitments to Kioxia: SanDisk's asset-light business model relies entirely on Kioxia Corporation through their joint venture for manufacturing. Consequently, SanDisk does not control production capacity decisions, yield outcomes, or capital expenditure timing, yet it remains bound to heavy contract obligations including $1.2 billion in direct payments and over $370 million in facility depreciation prepayments through 2029.

- Softness in Consumer Segment Demand: While hyper-scale data center demand has temporarily masked broader cyclicality, SanDisk’s consumer business segment experienced a 10% sequential decline in revenue last quarter. This sequential drop signals that pricing power and demand are weakening outside of the artificial intelligence infrastructure vertical.

- Stretched Valuations and Notable Insider Liquidations: Following a nearly 600% year-to-date run, the stock trades at an elevated trailing price-to-earnings multiple of over 70x. This vulnerability is compounded by persistent record-high short interest and recent insider liquidations, including open-market share sales executed by Chief Legal Officer Bernard Shek and EVP Alper Ilkbahar.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.