Salesforce Inc Stock (CRM) Opened Down by 3.18% on May 21: What Signal Does It Send?

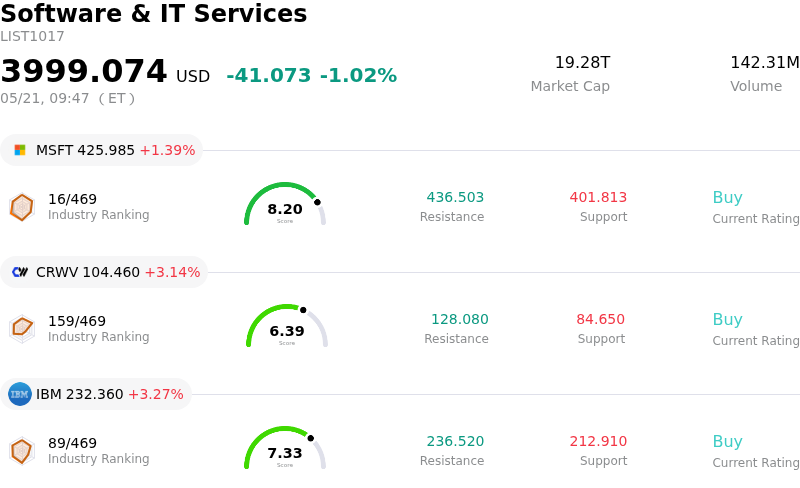

Salesforce Inc (CRM) opened down by 3.18%. The Software & IT Services sector is down by 1.02%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) up 1.39%; CoreWeave Inc (CRWV) up 3.14%; International Business Machines Corp (IBM) up 3.27%.

What is driving Salesforce Inc (CRM)’s stock price down today?

The decline in Salesforce's (CRM) share price today can be primarily attributed to recent analyst downgrades and persistent concerns regarding the company's long-term growth trajectory amidst the evolving artificial intelligence landscape.

Earlier this week, on May 18, Bank of America reinstated its coverage of Salesforce with an "Underperform" rating and a lowered price target. This cautious outlook stems from expectations of moderated new customer acquisition, limited potential for upselling to existing clients, and an "underwhelming" pathway for monetizing its AI products. The bank's analysis suggests a structural shift for Salesforce from a high-growth platform to a more mature cash generator, with anticipated annual revenue growth stabilizing around 10%, a notable reduction from historical rates. Similarly, Citigroup also recently reduced its price target for Salesforce, citing concerns over extended transaction cycles and increased client optimization during renewals, particularly impacting its Tableau and Marketing Cloud offerings. Citi also slightly lowered its fiscal 2027 earnings per share estimates for the company.

These analyst adjustments amplify broader market sentiment that has seen Salesforce's stock under pressure for much of 2026, trading near its 52-week low. Fears that advancements in AI could disrupt traditional enterprise software business models have weighed on the SaaS sector, with particular attention paid to the potential for AI coding agents to enable companies to develop custom solutions rather than relying on established platforms.

Adding to the intraday volatility is the impending release of Salesforce's first-quarter fiscal 2027 earnings report, scheduled for next Wednesday, May 27. Investors are keenly awaiting these results and the associated guidance for the next quarter, especially given the recent analyst concerns about a potential moderation in organic remaining performance obligation (cRPO) growth. While Salesforce has reported strong past financial results, including beating earnings and revenue estimates in its last quarterly report, and has initiated a substantial share repurchase program and increased dividends, the market appears to be prioritizing the recent bearish analyst commentary and the ongoing debate surrounding its AI monetization strategy.

Technical Analysis of Salesforce Inc (CRM)

Technically, Salesforce Inc (CRM) shows a MACD (12,26,9) value of [-2.13], indicating a neutral signal. The RSI at 50.69 suggests neutral condition and the Williams %R at -39.30 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Salesforce Inc (CRM)

Salesforce Inc (CRM) is in the Software & IT Services industry. Its latest annual revenue is $41.52B, ranking 13 in the industry. The net profit is $7.46B, ranking 15 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $264.60, a high of $475.00, and a low of $160.00.

More details about Salesforce Inc (CRM)

Company Specific Risks:

- A recent analyst downgrade to "Underperform" with a $160 price target reflects concerns regarding a structural growth slowdown attributed to the AI transition and an underwhelming monetization strategy for the Agentforce platform.

- Analysts report lengthening deal cycles and increased customer optimization of software portfolios at renewal, particularly affecting Tableau and Marketing Cloud, suggesting muted new customer acquisition and limited upsell opportunities.

- Intensified competitive pressure from hyperscalers and rivals such as ServiceNow, HubSpot, and Adobe is contributing to market share erosion and potentially impacting Salesforce's pricing power.

- Citi analysts anticipate a deceleration in organic current Remaining Performance Obligation (cRPO) growth for the second quarter of fiscal year 2027, projecting a slowdown to 8-8.5%.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.