PDD Holdings Inc Stock (PDD) Moved Up by 3.87% on May 13: Drivers Behind the Movement

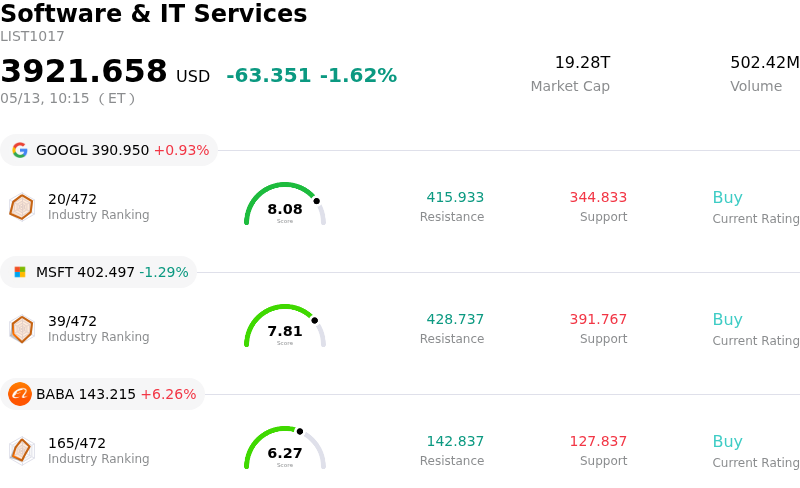

PDD Holdings Inc (PDD) moved up by 3.87%. The Software & IT Services sector is down by 1.62%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Alphabet Inc Class A (GOOGL) up 0.93%; Microsoft Corp (MSFT) down 1.29%; Alibaba Group Holding Ltd (BABA) up 6.26%.

What is driving PDD Holdings Inc (PDD)’s stock price up today?

PDD Holdings experienced an upward movement on May 13, 2026, driven by a confluence of positive analyst sentiment and strategic company developments ahead of its anticipated first-quarter 2026 earnings report. Analysts have expressed increasing optimism regarding PDD's outlook, with expectations for a significant year-over-year increase in earnings per share for the upcoming quarter. This positive forecast has been bolstered by recent analyst upgrades and reiterated buy ratings, with some firms highlighting the company's improving earnings trajectory and substantial growth potential both in China and internationally. The market appears to be positioning favorably in anticipation of these strong financial results.

Further contributing to the positive momentum are PDD's ongoing strategic initiatives aimed at long-term growth and market expansion. The company's domestic Pinduoduo platform continues to generate significant cash, while its international arm, Temu, is seen as offering substantial global optionality. Management has emphasized a strategic reinvestment into merchant support and supply chain efficiency, a move intended to build a more robust and globally scalable platform, even if it entails lower near-term margins. Notably, the launch of the "New Pinmu" strategy in April 2026, involving a substantial investment over three years to build owned brands and deeply integrate the supply chain with a focus on international markets, signals a proactive approach to addressing overseas growth challenges and adapting to evolving global trade policies. This initiative is perceived as a significant step towards enhancing Temu's supply chain quality and operational efficiency.

Moreover, there is a prevailing view among some analysts that PDD remains undervalued, with its robust business quality and significant net cash position not fully reflected in its current valuation. The perception that recent regulatory actions by Chinese authorities, such as fines, might be interpreted by the market as a clearance of regulatory uncertainties, could also be contributing to an improved investor outlook. These factors, combined with a broader positive sentiment towards U.S.-listed Chinese e-commerce equities, are likely contributing to the stock's elevated trading activity.

Technical Analysis of PDD Holdings Inc (PDD)

Technically, PDD Holdings Inc (PDD) shows a MACD (12,26,9) value of [-0.63], indicating a sell signal. The RSI at 40.91 suggests neutral condition and the Williams %R at -96.10 suggests oversold condition. Please monitor closely.

Fundamental Analysis of PDD Holdings Inc (PDD)

PDD Holdings Inc (PDD) is in the Software & IT Services industry. Its latest annual revenue is $62.58B, ranking 8 in the industry. The net profit is $14.18B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $142.80, a high of $198.00, and a low of $110.00.

More details about PDD Holdings Inc (PDD)

Company Specific Risks:

- PDD Holdings faces immediate legal and reputational risks due to the ongoing copyright infringement lawsuit filed by Shein in London's High Court, which commenced on May 11, 2026, and parallel lawsuits by the Attorneys General of Oklahoma (filed May 11, 2026) and Arizona (filed December 2, 2025) alleging unlawful data collection, privacy violations, and consumer fraud related to its Temu platform.

- Increased global regulatory scrutiny, including the European Commission's October 2024 investigation into Temu's compliance with the Digital Services Act (DSA) with potential fines up to 6% of annual global turnover, and ongoing examination of "de minimis" import provisions, threatens to impose significant financial penalties and operational hurdles on the company's international expansion efforts.

- Aggressive investment in customer acquisition, merchant subsidies, and supply chain efficiency for the Temu platform is placing continued pressure on PDD Holdings' near-term operating margins, potentially impacting overall profitability despite revenue growth.

- Intensifying competition within both the domestic Chinese and international e-commerce markets, alongside rising compliance and logistics costs, poses a threat to PDD Holdings' market share and could lead to increased customer acquisition expenses.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.