Coherent Corp Stock (COHR) Opened Up by 7.46% on May 13: What Investors Need To Know

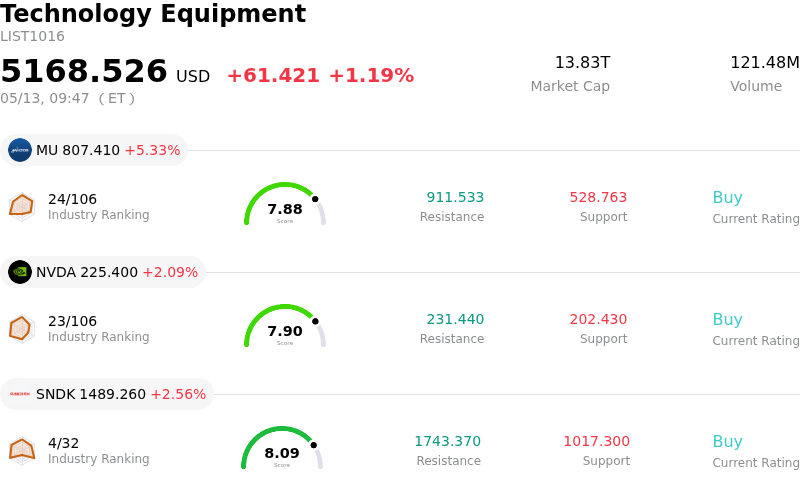

Coherent Corp (COHR) opened up by 7.46%. The Technology Equipment sector is up by 1.19%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 5.33%; NVIDIA Corp (NVDA) up 2.09%; SanDisk Corporation (SNDK) up 2.56%.

What is driving Coherent Corp (COHR)’s stock price up today?

Coherent Corp (COHR) is experiencing a notable upward movement today, primarily driven by a positive re-evaluation from a major investment bank. BofA Securities increased its price target for Coherent, citing the company's strong positioning to capitalize on the increasing demand for high-speed optical transceivers, specifically 800G and 1.6T models. This analyst optimism suggests confidence in Coherent's ability to benefit from the ongoing expansion in AI data center infrastructure.

This recent analyst action builds upon strong financial performance reported earlier this month. Coherent’s third-quarter fiscal year 2026 results, released on May 6, significantly surpassed analyst expectations for both revenue and non-GAAP earnings per share. The company highlighted robust demand within its Datacenter and Communications segment, which has become a dominant revenue driver. Management also provided an optimistic outlook for the fourth quarter of fiscal year 2026 and for fiscal year 2027, anticipating continued growth fueled by expanding AI infrastructure deployments and increasing optical networking demand.

Further contributing to the positive sentiment are recent upgrades from other analysts. For instance, a Stifel analyst maintained a "Buy" rating and sharply raised their price target on May 11, pointing to accelerating capital expenditures by U.S. hyperscalers for AI data centers. The analyst underscored Coherent's crucial role as a primary beneficiary of the "Scale-Out" and "Scale-Up" frameworks essential for AI data centers, noting extended order visibility.

Coherent's strategic partnerships and technological advancements also support its market position. The company has a significant agreement with NVIDIA, including a substantial equity investment and a multiyear supply agreement, reinforcing its pivotal role in the AI supply chain. Furthermore, Coherent is actively expanding its indium phosphide output capacity, a critical component for its high-speed transceivers, with plans to double production ahead of schedule. This capacity expansion is essential for meeting the escalating demand from the AI sector.

The broader market environment also plays a role, with a generally bullish sentiment in the technology sector, particularly in areas related to AI. This favorable backdrop, coupled with company-specific positive news, contributes to heightened investor interest in Coherent. While some market analysis suggests the stock might be overvalued by certain metrics, the strong operational performance, strategic positioning, and positive analyst revisions are currently outweighing these concerns, driving the stock's upward trajectory.

Technical Analysis of Coherent Corp (COHR)

Technically, Coherent Corp (COHR) shows a MACD (12,26,9) value of [16.50], indicating a buy signal. The RSI at 66.00 suggests neutral condition and the Williams %R at -11.55 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Coherent Corp (COHR)

Coherent Corp (COHR) is in the Technology Equipment industry. Its latest annual revenue is $5.81B, ranking 12 in the industry. The net profit is $-80.56M, ranking 63 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $370.99, a high of $455.44, and a low of $230.00.

More details about Coherent Corp (COHR)

Company Specific Risks:

- Near-term capacity constraints and persistent supply chain issues are impacting the company's ability to fully capitalize on strong demand, leading to management delaying long-term capacity ramp by at least a quarter, which negatively affected post-earnings stock performance.

- The industrial segment experienced a notable year-over-year revenue decline from $529.2 million to $444 million in Q3 FY 2026, indicating a significant weakness in a core business area outside of AI-driven growth.

- Recent insider selling, including a Form 144 filing for a proposed sale of 2,000 common shares by a company officer and prior reports of $5.6 million in insider sales without corresponding purchases, may signal a lack of confidence from company insiders.

- Concerns exist regarding market overvaluation, with a Price/Sales ratio of 11.08x significantly exceeding the Electronic industry average of 2.68x and peer average of 5.67x, coupled with reported underperformance in CISCO's CPO revenue capacity against competitor Lumentum.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.