Qualcomm Inc Stock (QCOM) Moved Up by 6.95% on May 5: Drivers Behind the Movement

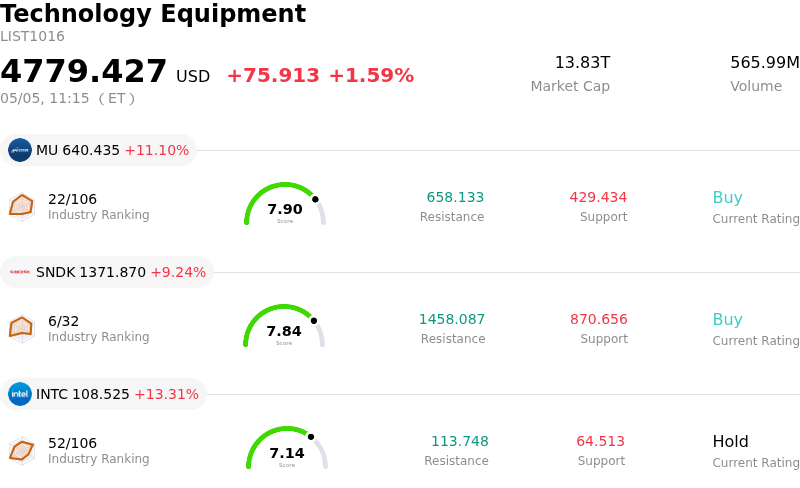

Qualcomm Inc (QCOM) moved up by 6.95%. The Technology Equipment sector is up by 1.59%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 11.10%; SanDisk Corporation (SNDK) up 9.24%; Intel Corp (INTC) up 13.31%.

What is driving Qualcomm Inc (QCOM)’s stock price up today?

Qualcomm's shares experienced a significant upward movement today, primarily driven by a confluence of positive developments related to its strategic diversification and advancements in artificial intelligence. A key catalyst appears to be recent reports indicating a partnership with OpenAI to develop an AI-native smartphone chip, with mass production targeted for 2028. This potential collaboration positions Qualcomm at the forefront of a new category of consumer devices and suggests significant future revenue streams beyond its traditional mobile chipset business.

This news builds on the momentum from the company's strong fiscal second-quarter 2026 earnings report, released recently, where Qualcomm exceeded consensus estimates for both revenue and earnings per share. The company also highlighted record revenue in its automotive segment, which surpassed an annualized run rate of $5 billion for the first time. The continued expansion into the automotive sector, alongside increasing engagement in data centers with planned initial shipments of custom silicon later in 2026, reinforces the narrative of successful diversification away from an over-reliance on the mature smartphone market.

Furthermore, the company's proactive capital allocation strategy, including the initiation of a substantial share repurchase program and an increase in its quarterly dividend, likely contributed to positive investor sentiment. While some analysts previously expressed caution regarding the company's fiscal third-quarter guidance, citing expected softness in handset demand from Chinese customers due to memory supply constraints, the market appears to be focusing on Qualcomm's long-term growth opportunities in AI and its expanding presence in new end markets. Analyst forecasts, despite some mixed ratings, generally point to significant long-term potential, with some upgrading price targets based on these emerging catalysts. The company's consistent unveiling of new Snapdragon platforms with advanced on-device AI capabilities at recent industry events further underscores its commitment to technological leadership and market expansion.

Technical Analysis of Qualcomm Inc (QCOM)

Technically, Qualcomm Inc (QCOM) shows a MACD (12,26,9) value of [5.16], indicating a buy signal. The RSI at 71.16 suggests buy condition and the Williams %R at -33.59 suggests oversold condition. Please monitor closely.

Media Coverage of Qualcomm Inc (QCOM)

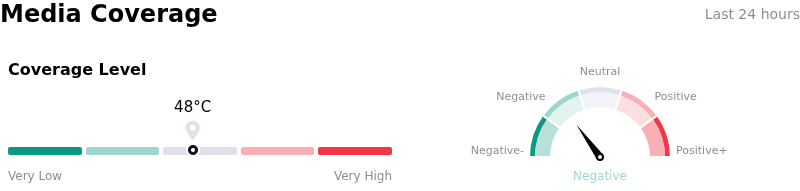

In terms of media coverage, Qualcomm Inc (QCOM) shows a coverage score of 48, indicating a moderate level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Qualcomm Inc (QCOM)

Qualcomm Inc (QCOM) is in the Technology Equipment industry. Its latest annual revenue is $44.28B, ranking 5 in the industry. The net profit is $5.54B, ranking 7 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $170.76, a high of $300.00, and a low of $100.00.

More details about Qualcomm Inc (QCOM)

Company Specific Risks:

- Qualcomm issued weaker-than-expected guidance for fiscal Q3 2026, projecting revenue below analyst forecasts and a significant decline in EPS, largely driven by anticipated reductions in QCT Handsets revenue.

- The company is experiencing a persistent decline in handset revenue, with Q2 FY26 handset revenues down 13% year-over-year, and analysts anticipate further contractions in the QCT handset business for calendar year 2026 due to a challenging market environment, memory supply shortages, and potential market share losses from key customers like Apple and Samsung.

- Analysts express ongoing concerns regarding increased competitive intensity in the datacenter market and a slower-than-anticipated adoption of Qualcomm's ARM-based chips in the PC market, where established competitors like Nvidia and AMD pose significant challenges.

- Despite diversification efforts into automotive and IoT segments, their current growth is not substantial enough to fully offset the ongoing revenue declines in the core handset business in the near term, with future catalysts like data center and OpenAI phone partnerships being years away from generating meaningful revenue.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.