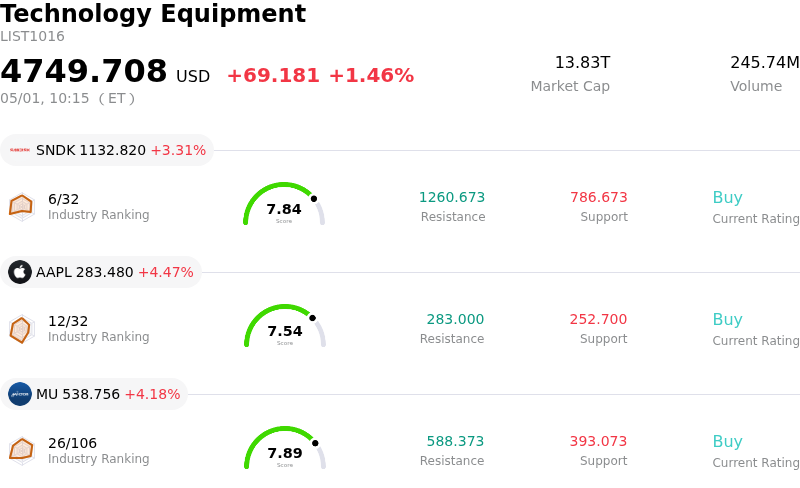

Micron Technology Inc Stock (MU) Moved Up by 4.18% on May 1: Facts Behind the Movement

Micron Technology Inc (MU) moved up by 4.18%. The Technology Equipment sector is up by 1.46%. The company outperformed the industry. Top 3 stocks by turnover in the sector: SanDisk Corporation (SNDK) up 3.31%; Apple Inc (AAPL) up 4.47%; Micron Technology Inc (MU) up 4.18%.

What is driving Micron Technology Inc (MU)’s stock price up today?

Micron Technology's stock experienced significant upward movement today, primarily driven by strong positive market sentiment surrounding the artificial intelligence (AI) driven memory supercycle and optimistic analyst forecasts. Several reports highlight the persistent demand for high-bandwidth memory (HBM) and other advanced memory solutions, which are crucial for AI infrastructure.

Industry analysts are increasingly bullish on Micron's prospects, with some setting aggressive price targets. For instance, DA Davidson initiated coverage with a "Buy" rating and a $1,000 price target, signaling nearly 100% upside, based on the belief that the current memory cycle will be longer and stronger than typical due to AI infrastructure build-out. Other firms like TD Cowen and Melius Research have also recently raised their price targets and maintained "Buy" ratings, citing expanding gross margins and the company's strong position in the AI memory market. This wave of positive analyst coverage and the reaffirmation of Micron's role as a structural enabler of AI growth has likely fueled investor confidence.

Furthermore, the memory market is expected to remain supply-constrained through 2026 and potentially beyond, particularly for DRAM and NAND. The shift in manufacturing capacity towards high-bandwidth memory (HBM) to meet AI demand is contributing to shortages in conventional memory products, leading to elevated pricing and strong margins for manufacturers like Micron. Micron has also made strategic moves such as signing five-year sales deals for HBM, which provides better visibility into future sales and earnings. The company's recent financial performance, including a significant increase in revenue and surging gross margins in its fiscal second quarter of 2026, further supports the positive outlook.

Technical Analysis of Micron Technology Inc (MU)

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of [23.21], indicating a buy signal. The RSI at 67.90 suggests neutral condition and the Williams %R at -14.44 suggests oversold condition. Please monitor closely.

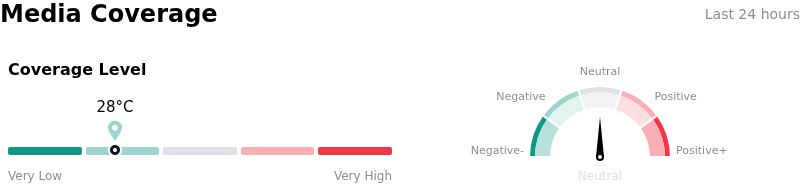

Media Coverage of Micron Technology Inc (MU)

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 28, indicating a low level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Micron Technology Inc (MU)

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $535.54, a high of $1000.00, and a low of $125.00.

More details about Micron Technology Inc (MU)

Company Specific Risks:

- Micron's significant increase in capital expenditure, projected to exceed $25 billion for the current fiscal year and further rise in 2027, is expected to reduce free cash flow and carries execution risk if demand falters or technology shifts impact expected returns.

- Intensifying competition in the High-Bandwidth Memory (HBM) market, particularly from rivals like Samsung which has begun HBM4 volume shipments, poses a direct threat of pricing pressure and potential erosion of Micron's HBM margins in 2026 and 2027.

- The inherent cyclicality of the broader memory market presents a risk of oversupply as new manufacturing capacity from multiple players comes online in 2027 and 2028, potentially leading to declining average selling prices and negatively impacting margins, despite current AI-driven demand.

- Micron's strong current performance and sold-out HBM capacity for 2026 are heavily reliant on robust AI infrastructure build-out and demand within the data center market, making the company vulnerable to any slowdown in AI adoption or general demand volatility in this segment.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.