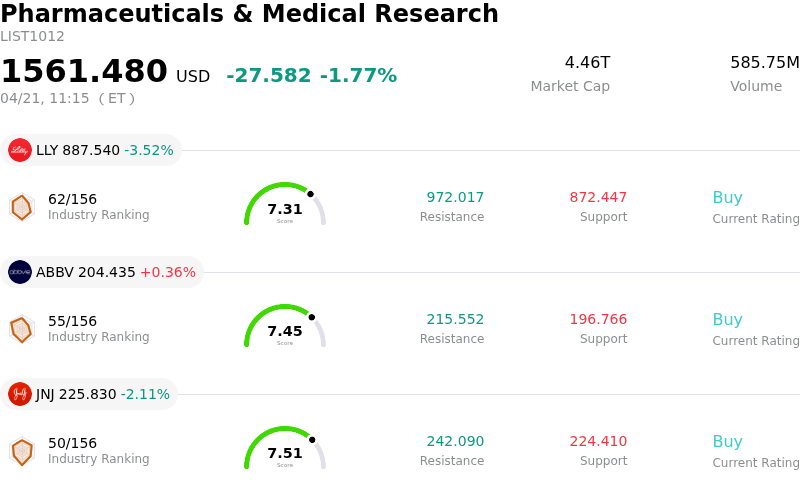

Eli Lilly and Co Stock (LLY) Moved Down by 3.52% on Apr 21: Key Drivers Unveiled

Eli Lilly and Co (LLY) moved down by 3.52%. The Pharmaceuticals & Medical Research sector is down by 1.77%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Eli Lilly and Co (LLY) down 3.52%; AbbVie Inc (ABBV) up 0.36%; Johnson & Johnson (JNJ) down 2.11%.

What is driving Eli Lilly and Co (LLY)’s stock price down today?

Eli Lilly and Company's stock experienced a significant intraday decline, primarily driven by developments concerning market access and regulatory considerations for its key obesity drug pipeline. The most immediate factor impacting investor sentiment was the announcement that CVS Health opted out of the Medicare obesity drug coverage model. This decision signals a potential challenge to the market penetration and revenue projections for Lilly's highly anticipated obesity treatments, as it limits access for a segment of the patient population.

Adding to the downward pressure is the continued regulatory scrutiny surrounding Lilly's oral obesity pill, Foundayo (orforglipron). While Lilly recently released positive topline results from the Phase 3 ACHIEVE-4 trial, demonstrating cardiovascular safety and no drug-induced liver injury, the FDA had previously requested additional safety data and initiated post-marketing cardiovascular studies. The agency also mandated a registry to track children with obesity using weight loss drugs and a pregnancy registry for Foundayo. This regulatory overhang, despite positive trial data, creates uncertainty regarding the drug's label and future market trajectory, contributing to investor caution.

Broader market sentiment also reflects concerns about the valuation of Lilly's stock, with some commentary suggesting that current prices may reflect overly optimistic expectations for the obesity drug market's size and the potential for intensifying price competition. An earlier analyst downgrade in March had highlighted these risks, forecasting a smaller market than consensus and potential headwinds from pricing pressure. These underlying concerns may amplify the impact of specific negative news events.

Despite these recent challenges, the company has had other positive developments, including the announced acquisition of Kelonia Therapeutics to expand its genetic medicine capabilities and positive trial results for its cancer therapy, Jaypirca. However, for the current trading period, the negative news regarding market access for its obesity franchise and lingering regulatory uncertainty appear to have taken precedence in driving the stock's performance.

Technical Analysis of Eli Lilly and Co (LLY)

Technically, Eli Lilly and Co (LLY) shows a MACD (12,26,9) value of [-15.02], indicating a neutral signal. The RSI at 44.98 suggests neutral condition and the Williams %R at -64.05 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Eli Lilly and Co (LLY)

Eli Lilly and Co (LLY) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is $65.18B, ranking 4 in the industry. The net profit is $20.64B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1201.91, a high of $1500.00, and a low of $850.00.

More details about Eli Lilly and Co (LLY)

Company Specific Risks:

- The company's stock maintains a premium valuation with an elevated P/E ratio, indicating high market expectations that leave limited margin for error if future growth or pipeline outcomes do not meet projections.

- Eli Lilly faces intensifying competition and potential pricing pressure within the GLP-1 market, with anticipated "low-to-mid teens drag" on 2026 top-line growth due to factors such as "most favored nation pricing" and TrumpRx platform discounts.

- A recent study highlighted that Eli Lilly's tirzepatide (Mounjaro/Zepbound) is associated with a greater loss of lean body mass compared to Novo Nordisk's semaglutide, which could negatively influence patient and physician preference.

- Heavy capital expenditure requirements for expanding manufacturing capacity to meet high demand for GLP-1 products pose execution risks and could pressure profitability.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.