Marvell Technology Inc Stock (MRVL) Moved Up by 3.23% on Apr 21: What Signal Does It Send?

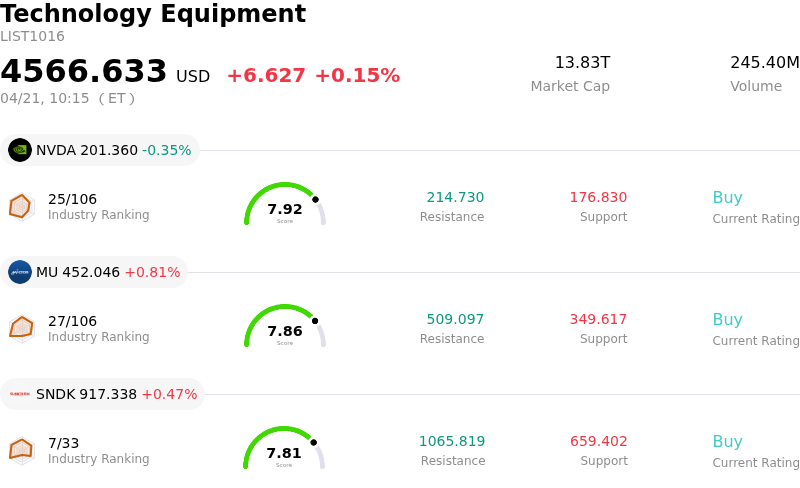

Marvell Technology Inc (MRVL) moved up by 3.23%. The Technology Equipment sector is up by 0.15%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 0.35%; Micron Technology Inc (MU) up 0.81%; SanDisk Corporation (SNDK) up 0.47%.

What is driving Marvell Technology Inc (MRVL)’s stock price up today?

Marvell Technology's stock experienced significant upward movement today, extending recent gains, primarily driven by reports of potential new partnerships and strong analyst sentiment regarding its position in the artificial intelligence (AI) sector. The most impactful news revolves around Alphabet's Google reportedly being in advanced discussions with Marvell to co-develop two custom AI chips. These chips are said to include a memory processing unit to work with Google's in-house Tensor Processing Unit (TPU) and a new TPU specifically designed for AI inference tasks, which would significantly deepen Marvell's role within the global AI supply chain and diversify its hyperscale customer base.

This potential collaboration with Google follows a previous significant development earlier in March when Nvidia announced a $2 billion investment in Marvell to jointly develop silicon photonics and AI infrastructure. The market perceives these consecutive endorsements from major AI industry players as strong validation of Marvell's technology and strategic direction in custom silicon and data infrastructure. The news also prompted a decline in shares of Broadcom, a traditional Google TPU design partner, highlighting the competitive shift in the AI chip landscape.

The positive sentiment is further reinforced by a series of recent analyst upgrades and significantly raised price targets. RBC Capital, for instance, raised its price target from $115 to $170, citing strength in PAM-4 optical connectivity and improved visibility for Trainium chip production for Amazon Web Services (AWS). Similarly, Oppenheimer and Barclays have also increased their price targets, pointing to robust data center demand, projected substantial growth in optical networking revenue, and successful partnerships with hyperscale customers in the ASIC chip space. GF Securities upgraded Marvell to a "Buy" rating, forecasting impressive data center revenue growth for fiscal years 2027 and 2028.

Marvell's strategic acquisitions, such as Xconn Technologies in January 2026 for AI development and cloud computing services, and Celestial AI in February 2026 for high-speed optical solutions, have also bolstered its capabilities and market positioning in AI data center connectivity. These acquisitions, combined with the company's strong focus on end-to-end connectivity solutions for AI data center infrastructure, underpin the optimistic outlook from analysts and investors. The overall strong narrative around AI chip demand and Marvell's leadership in providing critical components for hyperscale data centers continues to fuel investor confidence.

Technical Analysis of Marvell Technology Inc (MRVL)

Technically, Marvell Technology Inc (MRVL) shows a MACD (12,26,9) value of [10.66], indicating a buy signal. The RSI at 85.00 suggests overbought condition and the Williams %R at -3.08 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Marvell Technology Inc (MRVL)

Marvell Technology Inc (MRVL) is in the Technology Equipment industry. Its latest annual revenue is $5.77B, ranking 22 in the industry. The net profit is $-885.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $125.72, a high of $170.00, and a low of $85.00.

More details about Marvell Technology Inc (MRVL)

Company Specific Risks:

- Benchmark downgraded Marvell to a "Hold" rating, citing a "high degree of conviction" that the company lost the custom XPU business for Amazon's upcoming Trainium 3 and 4 chipsets to a competitor, and reports also indicate a potential loss of Microsoft as an AI customer, raising concerns about future revenue streams.

- The company faces significant customer concentration risk, with over 90% of its data center revenue tied to a few major AI and cloud hyperscalers, making it highly vulnerable to shifts in client strategies or demand.

- An analyst downgrade on April 16, 2026, cited an "overly done rally" and a stretched forward Price-to-Earnings valuation of 35.01x, contributing to recent intraday declines and suggesting potential downside risk due to elevated valuation.

- Significant insider selling occurred on April 15 and 16, 2026, with the Chief Financial Officer selling 30,000 shares and the President of the Data Center Group selling 66,892 shares, which may signal a lack of confidence from key executives.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.