Marvell Technology Inc Stock (MRVL) Opened Up by 4.59% on Apr 20: Key Drivers Unveiled

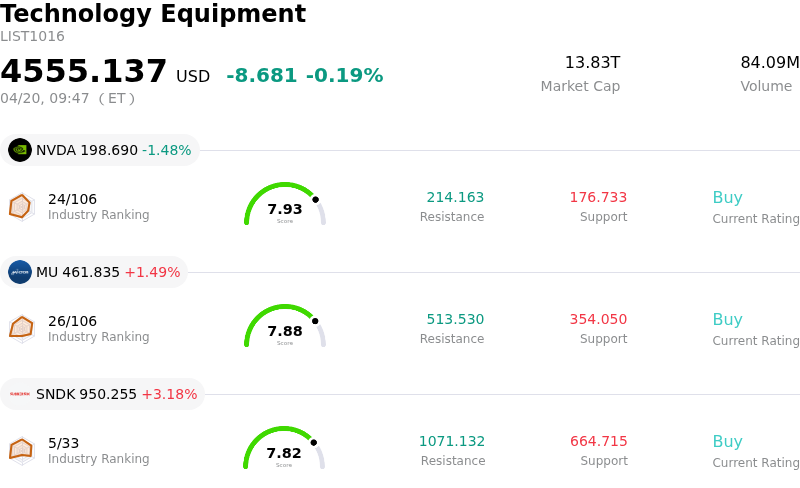

Marvell Technology Inc (MRVL) opened up by 4.59%. The Technology Equipment sector is down by 0.19%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 1.48%; Micron Technology Inc (MU) up 1.49%; SanDisk Corporation (SNDK) up 3.18%.

What is driving Marvell Technology Inc (MRVL)’s stock price up today?

Marvell Technology (MRVL) experienced significant positive intraday movement on April 20, 2026, primarily driven by major news concerning a potential partnership with Google in the artificial intelligence (AI) chip development space. The Information reported on Sunday that Marvell was in discussions with Google to co-develop two new chips designed to enhance the efficiency of AI models. These chips reportedly include a memory processing unit intended to work alongside Google's existing Tensor Processing Units (TPUs) and a new TPU specifically engineered for AI inference workloads. This development suggests Google is looking to diversify its custom silicon supply chain beyond its current partners and strengthens Marvell's position as a key player in the AI infrastructure buildout.

This reported collaboration is viewed by analysts, such as Wells Fargo, as a meaningful incremental positive for Marvell, potentially aiding in customer diversification. The semiconductor market is increasingly influenced by expectations surrounding future AI architectures, amplifying the impact of such news. Marvell's shares saw premarket gains following these reports, underscoring the market's positive reaction to its expanding role in AI.

This positive sentiment aligns with a broader trend of increased analyst optimism surrounding Marvell. Multiple firms have recently raised price targets and reiterated "Buy" ratings, citing stronger AI data-center demand and the company's accelerating optical solutions. For instance, Oppenheimer boosted its price target to $170 on April 15, 2026, and Stifel increased its target to $140 on April 16, 2026. The consensus among 32 analysts rates Marvell Technology with a "Strong Buy" as of April 19, 2026.

Furthermore, Marvell has been demonstrating strong performance within its Data Center segment, which showed sequential growth, and its Communications and Other end markets are showing signs of recovery. The company anticipates its Interconnect business will see over 50% year-over-year growth in fiscal year 2027, exceeding previous expectations. The company also reported robust financial results for the fourth quarter of fiscal 2026, with revenue and non-GAAP EPS exceeding expectations, driven largely by strong AI demand. Additionally, Marvell recently launched its Structera S 30260 CXL switch, designed to enable rack-level memory pooling, showcasing its technological advancements in high-performance computing for AI. Marvell's focus on optical interconnects and custom silicon solutions for AI data centers, alongside a significant investment from NVIDIA earlier in April 2026, further solidifies its strategic position in the rapidly evolving AI landscape.

Technical Analysis of Marvell Technology Inc (MRVL)

Technically, Marvell Technology Inc (MRVL) shows a MACD (12,26,9) value of [9.91], indicating a buy signal. The RSI at 82.31 suggests overbought condition and the Williams %R at -0.41 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Marvell Technology Inc (MRVL)

Marvell Technology Inc (MRVL) is in the Technology Equipment industry. Its latest annual revenue is $5.77B, ranking 22 in the industry. The net profit is $-885.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $125.72, a high of $170.00, and a low of $85.00.

More details about Marvell Technology Inc (MRVL)

Company Specific Risks:

- Sizable Rule 10b5-1 insider sales by the CEO, CFO, and another senior insider in early April 2026, even if pre-arranged, may indicate short-term profit-taking and could be perceived negatively by investors.

- The stock exhibits elevated valuation concerns after a significant rally (over 40% in April and 100%+ over the last 12 months), raising the risk of a potential pullback if future execution or the cadence of AI spending disappoints.

- Marvell faces considerable customer concentration risk, with more than 90% of its data center revenue dependent on a few large cloud hyperscalers, making the company vulnerable to shifts in their capital expenditure or demand.

- Competitive pressures and reports of potential loss of key hyperscale customer contracts, such as Amazon's Trainium 3 and 4 chip designs to a competitor, could hinder future XPU growth.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.