The “Split Reality” of U.S. Q2 GDP: 3% Growth Masked by Plunging Imports, Domestic Demand Cools

TradingKey - The U.S. economy rebounded sharply in Q2 2025, with real GDP growth clocking in at 3.0%, reversing Q1’s -0.5% contraction and far exceeding the 2.6% consensus forecast. The strong number has become a centerpiece of President Donald Trump’s economic messaging, but economists warn the headline figure is misleading — masking underlying weakness in domestic demand and a distortion caused by volatile trade flows.

On Thursday, July 30, the U.S. Bureau of Economic Analysis (BEA) released the advance Q2 GDP estimate, prompting the White House to declare victory.

In a post titled “Absolute Blockbuster”: New GDP Report Shows Explosive Growth in Trump’s Economy”, the Trump administration claimed the data proves Trump’s critics wrong, highlighting tame inflation, rising blue-collar wages, explosive job creation, and a “Made in America” boom.

Trump himself said the 3% figure was “better than expected”, while Treasury Secretary Scott Bessent called it proof of the success of the “America First” economic agenda.

ABC News noted the report showed the economy avoided a deep slowdown from tariffs, with stronger consumer spending helping to drive the rebound.

But the Data Tells a More Nuanced Story

Behind the headline strength, analysts point to two distorting anomalies that make the 3% growth number less impressive — and potentially unsustainable:

- A plunge in imports artificially boosted GDP

- Domestic private demand growth slowed to its weakest in over two years

Imports Collapse — Inflating the GDP Number

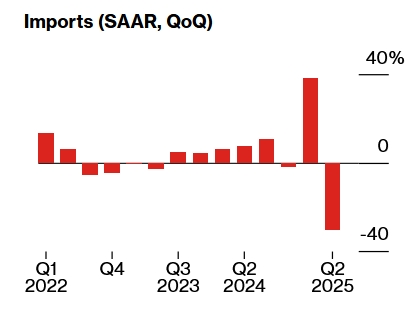

The biggest driver of Q2 GDP growth was a 30.3% collapse in real imports — a sharp reversal from Q1’s 37.9% surge.

U.S. Import Trends, Source: BEA, Bloomberg

As GDP is calculated as:GDP = Consumption + Investment + Government Spending + (Exports – Imports)

A sharp drop in imports adds to GDP, even if it reflects weaker domestic demand or supply chain disruptions, not real economic strength.

Morgan Stanley noted that this import swing contributed 4.99 percentage points to Q2 GDP — more than the entire headline growth rate.

This echoes Q1, when import surges due to pre-tariff stockpiling dragged down GDP. Now, the reverse is happening — and the same distortion is inflating the current quarter.

The Wall Street Journal pointed out that this wild import volatility reflects how Trump’s tariff policy has disrupted business decision-making, leading to boom-bust inventory cycles.

This distortion also hurt investment: after a Q1 surge, private domestic investment fell 15.6% in Q2.

Domestic Demand Is Cooling

While consumer spending — which makes up two-thirds of GDP — rose 1.4%, it was below the 1.5% forecast and remains well below the 3–4% growth seen in 2024.

More importantly, economists are focusing on final sales to domestic purchasers — a key measure of underlying demand that excludes the noise of trade swings.

- Q2 final domestic sales growth: +1.2%

- This is the weakest pace since Q4 2022

- Down from 1.9% in Q1 and 2.9% in Q4 2024

Bloomberg economist Eliza Winger noted:

“Final sales to private domestic purchasers cooled — signaling economic activity was softening even without tariff costs being fully passed through to consumers.”

Morgan Stanley warned that consumer spending has cooled, and both residential and business investment are soft. Households and firms are tightening their belts.

Despite the strong GDP print, Morgan Stanley maintains its downward economic trajectory forecast: Q4 2025 GDP +1.0%; 2026 GDP +1.1%.

BMO economist Scott Anderson said that the trend of cooling demand is very clear over the past two quarters, and growth now appears to be slipping below its longer-term potential pace.

“This will soon give the FOMC the room to start cutting interest rates again before too long, despite the threat of temporarily higher inflation from tariffs.”

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.