Intel Corp Stock (INTC) Closed Up by 8.84% on Apr 1: A Full Analysis

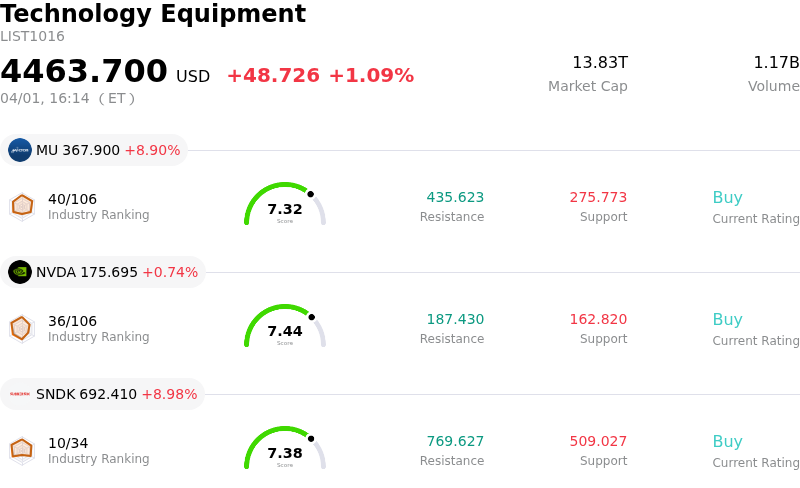

Intel Corp (INTC) closed up by 8.84%. The Technology Equipment sector is up by 1.09%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 8.90%; NVIDIA Corp (NVDA) up 0.74%; SanDisk Corporation (SNDK) up 8.98%.

What is driving Intel Corp (INTC)’s stock price up today?

Intel's stock experienced a significant upward movement on April 1, 2026, primarily driven by a strategic move to regain full ownership of a key manufacturing facility and positive sentiment surrounding its advancements in AI and chip production.

A major catalyst for the stock's rise was Intel's announcement that it will repurchase Apollo Global Management's 49% equity interest in its Fab 34 facility in Ireland for $14.2 billion. This move effectively unwinds a 2024 transaction where Intel had sold the stake to Apollo for $11.2 billion to secure capital for manufacturing expansion. Regaining full control of Fab 34, which produces chips using Intel 4 and Intel 3 process technologies, including Core Ultra processors for PCs and Xeon processors for servers, signals renewed confidence in Intel's long-term manufacturing ambitions and an improved financial position. The company plans to fund this buyback through cash on hand and approximately $6.5 billion in new debt, expecting it to boost profit and strengthen its credit profile from 2027 onward.

Investor sentiment has also been buoyed by Intel's continued advancements in AI-driven technologies and product innovation. The company's Core Ultra Series 3 processors, first launched at CES 2026, are a significant component of the AI PC platform, and Intel has highlighted the increasing demand for CPUs in agentic AI workloads. Intel's strategic positioning to meet the growing demand for AI chips for data centers and edge devices, coupled with ongoing supply-demand imbalances in the semiconductor industry, allows the company to implement price increases, supporting its turnaround strategy.

Furthermore, the broader semiconductor industry is experiencing strong growth, particularly in 300mm fab equipment spending, driven by surging AI chip demand and commitments to semiconductor self-sufficiency. Projections indicate double-digit growth in global 300mm fab equipment spending for 2026 and 2027, with advanced node technology being essential for AI applications. This positive industry backdrop provides a supportive environment for Intel's manufacturing expansion and strategic initiatives.

While some analyst ratings on Intel remain cautious, with a consensus "Hold" rating from various analysts, the recent positive developments suggest a shift in the company's narrative from "survival" to "execution" under its current CEO. The company is set to report its first-quarter 2026 financial results on April 23, which will offer further insights into its performance and outlook.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of [-0.38], indicating a sell signal. The RSI at 48.24 suggests neutral condition and the Williams %R at -59.02 suggests oversold condition. Please monitor closely.

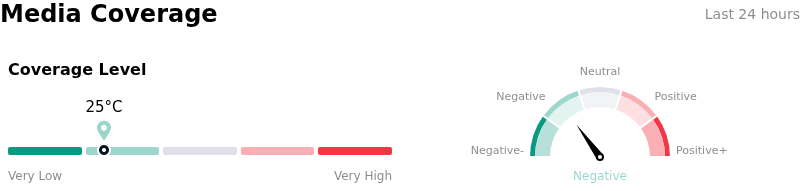

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 25, indicating a low level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 109 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $46.07, a high of $71.50, and a low of $20.40.

More details about Intel Corp (INTC)

Company Specific Risks:

- Intel has been explicitly named by Iran's Islamic Revolutionary Guard Corps (IRGC) as a "legitimate military target," with threats of attacks on its facilities reportedly set to commence as early as April 1st, introducing significant geopolitical and operational risks.

- The company's near-term financial guidance for Q1 2026 projects zero non-GAAP earnings per share and revenue between $11.7 billion and $12.7 billion, indicating immediate financial pressure and ongoing supply chain limitations.

- Intel's Foundry Services (IFS) segment faces severe yield issues with its crucial 18A process node, which is hindering high-volume production and is expected to delay profitability until at least 2027 due to minimal external customer commitments.

- The company continues to experience intense competitive pressure from rivals such as NVIDIA and AMD, leading to sustained market share erosion in critical growth areas, including AI accelerators and data center CPUs.

Recommended Articles