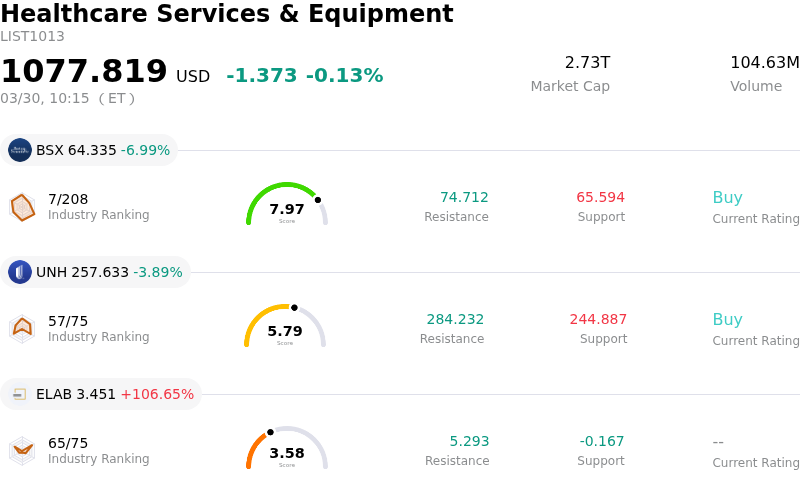

Unitedhealth Group Inc Stock (UNH) Moved Down by 3.89% on Mar 30: What Investors Need To Know

Unitedhealth Group Inc (UNH) moved down by 3.89%. The Healthcare Services & Equipment sector is down by 0.13%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Boston Scientific Corp (BSX) down 6.99%; Unitedhealth Group Inc (UNH) down 3.89%; PMGC Holdings Inc (ELAB) up 106.65%.

What is driving Unitedhealth Group Inc (UNH)’s stock price down today?

UnitedHealth Group (UNH) experienced a notable decline in its share price, influenced by a combination of increasing regulatory pressure, a weakened financial outlook for the current fiscal year, and evolving industry dynamics. The company is facing heightened scrutiny from multiple fronts, which appears to be weighing heavily on investor sentiment.

A significant factor contributing to the negative movement is the deepening Department of Justice (DOJ) probe into the relationship between UnitedHealth’s Optum health services segment and its insurance arm, including an antitrust lawsuit concerning insulin pricing. This is complemented by an investigation launched by Scott+Scott Attorneys at Law, which is scrutinizing whether certain company directors and officers breached their fiduciary duties. Furthermore, U.S. senators have renewed an inquiry into the company's practices related to nursing home transfers. Adding to the regulatory landscape, activist investors have initiated a lawsuit against UnitedHealth Group to compel annual reporting on patient care access and the impact of its mergers and acquisitions, a proposal the company had previously excluded from its proxy materials. The formation of a new Federal Trade Commission (FTC) Healthcare Task Force in March 2026, aimed at intensifying enforcement and advocacy efforts across the healthcare industry, signals a broader environment of increased regulatory risk for large healthcare entities.

Financially, UnitedHealth Group has provided guidance indicating a rare anticipated decline in revenue for 2026, falling short of analyst expectations. The company projects a loss of over 3 million members in 2026 as it plans to exit less profitable Medicare Advantage markets and shed low-margin Medicaid contracts. This outlook is further complicated by the Trump administration's proposal for a smaller-than-anticipated increase in 2027 Medicare Advantage payment rates, which could further pressure profit margins for insurers heavily reliant on this segment. Rising medical costs have also been identified as a factor compressing insurance margins, particularly within the Medicare Advantage segment. While some analysts maintain a "Moderate Buy" rating for the stock, there have been adjustments to price targets and at least one "sell" rating issued in early March. Moreover, Zacks anticipates a decline in earnings per share for the upcoming quarter compared to the prior year.

Amidst these challenges, there have been efforts by UnitedHealthcare to roll out "Avery," a generative AI companion designed to simplify member navigation and improve operational efficiency. However, the ongoing and accumulating legal and regulatory investigations, combined with a cautious financial forecast and sector-specific policy headwinds, appear to be overshadowing these positive technological advancements and contributing to the stock's negative performance. The broader healthcare industry is also facing pressures, including changes in Medicare Advantage plan availability for millions of beneficiaries and government efforts to slow reimbursement growth in the program.

Technical Analysis of Unitedhealth Group Inc (UNH)

Technically, Unitedhealth Group Inc (UNH) shows a MACD (12,26,9) value of [-5.32], indicating a sell signal. The RSI at 30.80 suggests neutral condition and the Williams %R at -90.75 suggests oversold condition. Please monitor closely.

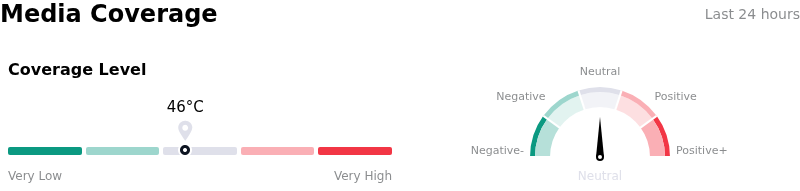

Media Coverage of Unitedhealth Group Inc (UNH)

In terms of media coverage, Unitedhealth Group Inc (UNH) shows a coverage score of 46, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Unitedhealth Group Inc (UNH)

Unitedhealth Group Inc (UNH) is in the Healthcare Services & Equipment industry. Its latest annual revenue is $447.93B, ranking 1 in the industry. The net profit is $12.06B, ranking 1 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $363.47, a high of $457.00, and a low of $255.00.

More details about Unitedhealth Group Inc (UNH)

Company Specific Risks:

- UnitedHealth Group faces a new lawsuit filed by activist investors seeking to compel the company to disclose the impact of its vertical integration strategy on patient care access and pricing, despite the SEC backing the company's exclusion of the proposal.

- A federal judge has ordered UnitedHealth Group to provide discovery details regarding its algorithmic tool used in a class-action lawsuit alleging AI-driven denials of post-acute care coverage.

- The company anticipates a significant decline in membership for 2026, projecting a loss of 2.3 million to 2.8 million members across its Medicare Advantage, Medicaid, and commercial plans, which is expected to result in a modest revenue decline.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.