Lam Research Corp Stock (LRCX) Moved Down by 3.19% on Mar 20: What Signal Does It Send?

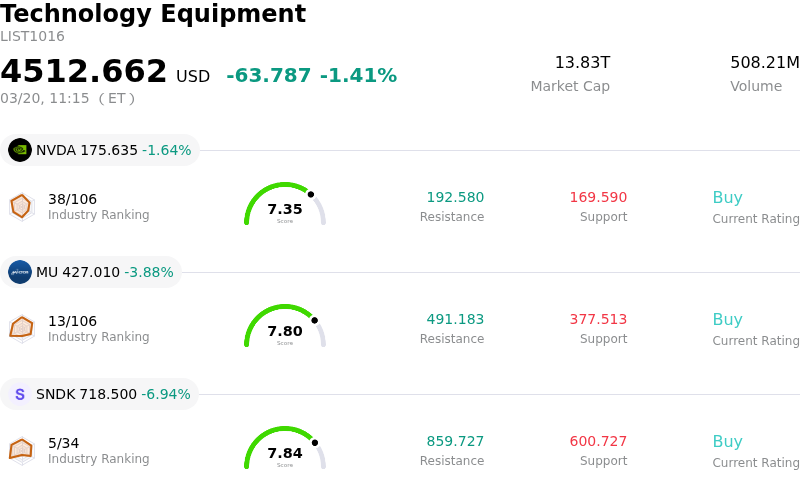

Lam Research Corp (LRCX) moved down by 3.19%. The Technology Equipment sector is down by 1.41%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 1.64%; Micron Technology Inc (MU) down 3.88%; SanDisk Corporation (SNDK) down 6.94%.

What is driving Lam Research Corp (LRCX)’s stock price down today?

The share price of Lam Research Corporation experienced downward pressure today, influenced by a combination of macroeconomic headwinds and company-specific concerns. A significant contributing factor is the broader macroeconomic environment, notably the Federal Reserve's recent decision to maintain interest rates while simultaneously revising its 2026 inflation projections upward. This suggests persistent inflationary pressures, which could imply fewer or later interest rate cuts than some market participants had anticipated, fostering a cautious, risk-averse sentiment that typically impacts growth-oriented technology stocks. Furthermore, ongoing geopolitical uncertainties, particularly in the Middle East, have contributed to elevated energy prices, further complicating the inflation outlook and adding to overall market jitters.

Company-specific factors also played a role in the stock's movement. There has been notable insider selling activity in recent weeks, with both the Chief Financial Officer and a director selling shares in early March. Such transactions can be interpreted by the market as a lack of confidence from management in the company's near-term prospects, potentially dampening investor sentiment. Additionally, concerns persist regarding Lam Research's revenue exposure to the Chinese market and the potential for margin compression. The company faces ongoing risks from U.S. export controls and escalating geopolitical tensions, which have led to a projected decline in revenue contribution from China.

Despite these pressures, the underlying fundamentals of Lam Research remain robust, and the broader semiconductor industry continues to benefit from strong demand driven by artificial intelligence. The company previously reported solid earnings, surpassing analyst estimates, and provided positive guidance for the current quarter. Many analysts maintain positive ratings and price targets, acknowledging the industry's significant growth trajectory. However, "bear" arguments have highlighted potential risks such as customer capital expenditure reductions and a less favorable customer mix, which appear to be weighing more heavily on the stock in the current trading environment.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [-1.36], indicating a neutral signal. The RSI at 56.34 suggests neutral condition and the Williams %R at -2.80 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $270.39, a high of $325.00, and a low of $116.32.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Significant insider selling by the Chief Financial Officer and a director within the last 72 hours indicates a cautious outlook from management and has generated market concern regarding future performance.

- Ongoing scrutiny from the US House Select Committee on the CCP regarding sales practices in China, combined with projected declines in revenue contribution from China due to export controls and escalating geopolitical risks, poses a material threat given China's substantial revenue share.

- A negative outlook is anticipated due to declining gross margins, attributed to an unfavorable customer mix, demand volatility from leading-edge clients, and planned capital expenditure reductions by Intel.

- Analyst commentary highlights the stock's stretched valuation, trading at peak cycle price-to-earnings ratios, which makes it susceptible to profit-taking and sharper reactions to negative news.