SAP SE Stock (SAP) Opened Down by 4.90% on Mar 20: What Signal Does It Send?

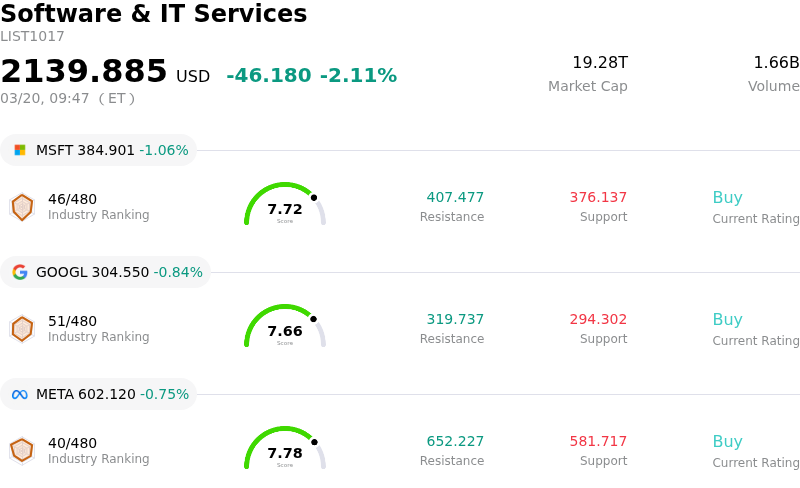

SAP SE (SAP) opened down by 4.90%. The Software & IT Services sector is down by 2.11%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) down 1.06%; Alphabet Inc Class A (GOOGL) down 0.84%; Meta Platforms Inc (META) down 0.75%.

What is driving SAP SE (SAP)’s stock price down today?

SAP's stock experienced significant downward pressure today, largely driven by revelations regarding its cloud migration strategy and ongoing concerns about its future growth trajectory. A report published yesterday, March 19, 2026, indicated that SAP's cloud migration plan is substantially behind target, falling short by an estimated €2 billion or 24% of its goal. This suggests that enterprise customers are not transitioning from on-premise software to cloud subscriptions as rapidly as the company had anticipated, posing a direct threat to its long-term financial objectives.

The shortfall in cloud adoption is evident in the higher-than-expected €10.5 billion in on-premise software support revenue for fiscal year 2025, significantly above the targeted €8.5 billion. This indicates persistent challenges in convincing legacy customers to undertake the costly and disruptive transition to S/4HANA and the cloud. Adding to these concerns, some major clients, such as Kingfisher, have reportedly opted to move their core enterprise resource planning (ERP) systems to third-party cloud providers, bypassing SAP's own migration plans. This signals a potential shift in competitive dynamics and could lead to further customer churn. Consequently, SAP appears to be pivoting its strategy to focus more on upselling its wider product portfolio, including artificial intelligence (AI) licensing, rather than solely on ERP modernization, as its migration targets are being missed.

This comes on the heels of financial data from late January, when SAP's shares plunged following its Q4 2025 earnings report and lower-than-expected 2026 guidance. At that time, the current cloud backlog growth was slightly below analyst expectations, and the 2026 cloud revenue forecast also disappointed the market, leading to a significant daily decline in the stock. The company's recent price performance shows declines over the past week, month, and year-to-date, reflecting continued investor apprehension.

Further compounding the negative sentiment is news of a formal EU antitrust investigation into SAP. This probe reportedly focuses on the company's aggressive tactics concerning customer support options, which could introduce regulatory risks and potentially impact future business practices. While analyst sentiment remains moderately positive overall, some have lowered their ratings or price targets, reflecting a cautious outlook amidst these challenges. Concerns regarding security vulnerabilities, highlighted by the March 2026 Security Patch Day identifying critical issues in key SAP components, also contribute to the perceived operational risks.

Technical Analysis of SAP SE (SAP)

Technically, SAP SE (SAP) shows a MACD (12,26,9) value of [-5.89], indicating a sell signal. The RSI at 33.84 suggests neutral condition and the Williams %R at -90.45 suggests oversold condition. Please monitor closely.

Fundamental Analysis of SAP SE (SAP)

SAP SE (SAP) is in the Software & IT Services industry. Its latest annual revenue is $41.49B, ranking 14 in the industry. The net profit is $8.07B, ranking 13 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $302.22, a high of $367.98, and a low of $178.44.

More details about SAP SE (SAP)

Company Specific Risks:

- SAP is undertaking a significant overhaul of its AI strategy, including a shift to consumption-based pricing, in response to competitive threats from generative AI providers and mixed early feedback on its own AI tools, indicating potential revenue model disruption and execution challenges.

- The company is substantially behind its cloud migration targets, missing its 2025 goal for reducing on-premise software support revenue by approximately €2 billion, with a low percentage of legacy ECC customers having started the transition to S/4HANA by the end of 2024.

- Ongoing antitrust investigations in the EU concerning SAP's ERP support practices, coupled with a pending trade secret lawsuit from o9 Solutions, pose risks of regulatory fines, legal costs, and mandatory changes to business operations.

- Negative analyst commentary and downgrades, partly stemming from the Q4 2025 cloud backlog growth missing guidance, continue to reflect investor concerns about SAP's cloud transition momentum and future financial performance.