Comcast Corp Stock (CMCSA) Moved Down by 3.41% on Mar 18: Facts Behind the Movement

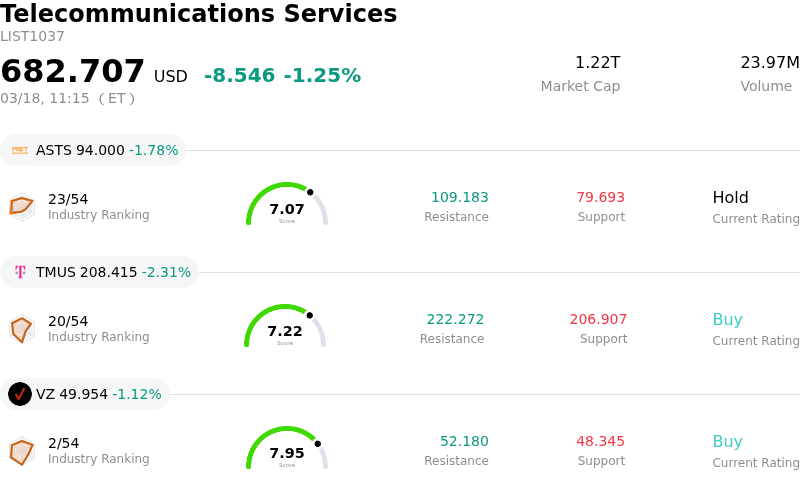

Comcast Corp (CMCSA) moved down by 3.41%. The Telecommunications Services sector is down by 1.25%. The company underperformed the industry. Top 3 stocks by turnover in the sector: AST SpaceMobile Inc (ASTS) down 1.78%; T-Mobile US Inc (TMUS) down 2.31%; Verizon Communications Inc (VZ) down 1.12%.

What is driving Comcast Corp (CMCSA)’s stock price down today?

CMCSA is experiencing downward pressure and significant intraday volatility today, primarily influenced by a confluence of recent negative analyst adjustments and underlying business segment challenges.

Several investment firms have recently revised their outlook on Comcast, with some analysts downgrading ratings and reducing price targets for the stock in late 2025 and early 2026. For example, one firm lowered its rating to "underperform" with a reduced price objective in February. Other institutions have also decreased their price targets, signaling a more cautious sentiment from the analytical community. These adjustments in analyst forecasts contribute to investor uncertainty and can trigger downward movements.

Compounding this sentiment are ongoing concerns related to Comcast's Content & Experiences segment. This division has faced financial headwinds, including decreased sales and a notable decline in Adjusted EBITDA, attributed to rising operational costs and challenging year-over-year comparisons. Furthermore, the company continues to grapple with a reduction in its domestic video subscriber base, which has led to broader pressure on overall EBITDA. These operational setbacks suggest sustained challenges, with some forecasts indicating peak difficulties by the second quarter of 2026.

Investor confidence may also be affected by negative forward-looking financial estimates. The Zacks Consensus Estimates for the full year 2026 project a decrease in earnings per share and a slight decline in revenue compared to the previous year. These anticipated decreases in key financial metrics can weigh heavily on a stock's performance. Additionally, there has been insider selling activity, with the CEO reducing shareholdings in February, which can sometimes be interpreted negatively by the market.

While some positive developments, such as a recent partnership with NVIDIA to accelerate AI applications, have been announced, their impact appears to be overshadowed by the more immediate financial and operational concerns. Institutional investor activity also presents a mixed picture; while some funds have increased their holdings, others have notably decreased or sold off portions of their stakes in Comcast. This divergence in institutional sentiment adds to the prevailing volatility.

Technical Analysis of Comcast Corp (CMCSA)

Technically, Comcast Corp (CMCSA) shows a MACD (12,26,9) value of [0.22], indicating a neutral signal. The RSI at 42.84 suggests neutral condition and the Williams %R at -96.67 suggests oversold condition. Please monitor closely.

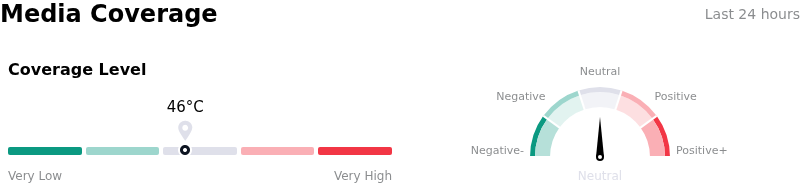

Media Coverage of Comcast Corp (CMCSA)

In terms of media coverage, Comcast Corp (CMCSA) shows a coverage score of 46, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Comcast Corp (CMCSA)

Comcast Corp (CMCSA) is in the Telecommunications Services industry. Its latest annual revenue is $123.71B, ranking 3 in the industry. The net profit is $20.00B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $33.82, a high of $53.00, and a low of $23.00.

More details about Comcast Corp (CMCSA)

Company Specific Risks:

- Persistent decline in domestic broadband and video subscriber base, reflecting intensifying competition from fixed-wireless and fiber alternatives.

- Significant year-over-year decline in the Content & Experiences segment's Adjusted EBITDA, driven by rising costs and challenging previous year comparisons, which negatively impacts overall profitability.

- Anticipated pressure on Average Revenue Per User (ARPU) and revenue in early 2026 due to a strategic decision to forgo internet price increases, aimed at customer retention in a highly competitive market.

- Slow progress in adapting business strategies to counter the growth of disruptive streaming services and alternative broadband providers, posing a risk to market share retention and long-term growth.