TradingKey - When planning for retirement, have you accounted for this “invisible bill”?

According to Fidelity’s 2025 Retirement Health Care Cost Report, a 65-year-old retiring in 2025 can expect to spend an average of $172,500 on health care expenses throughout retirement. If you have chronic health conditions or require long-term dental or vision care—services typically excluded from standard Medicare coverage—that figure could climb significantly higher.

Compounding the challenge, Aon’s 2025 Global Medical Trends Report forecasts that global health care inflation will average 10.0% in 2025, with North America (U.S. and Canada) projected at 8.8%. If this rate holds steady over the next 30 years, $100,000 saved today for future medical needs would have the purchasing power of just $6,600 by the time you retire.

Meanwhile, Vanguard’s latest data reveals that the median 401(k) balance for Americans aged 45–54 is only $67,796—far short of what most envision for a comfortable retirement.

Shams Talib, head of workplace consulting at Fidelity, puts it plainly:

“Year after year, so many Americans underestimate how much they’ll need to save to cover health care costs in retirement,” said Shams Talib, head of Fidelity Workplace Consulting. “We recognize the impact health care costs can have on retirement savings. With the right tools and guidance, pre-retirees and retirees alike can take greater control of their financial futures by beginning the planning process as soon as possible.”

Caught between unpredictable medical expenses and a glaring retirement savings gap, many find themselves in a financial bind: afraid to spend, yet unable to save enough.

Amid this dilemma, one financial tool stands out for its rare dual power: the Health Savings Account (HSA). Far more than just a medical reimbursement account—or even a typical retirement vehicle—the HSA is a tax-advantaged powerhouse that uniquely bridges health care planning and long-term wealth building.

(Source: Shutterstock)

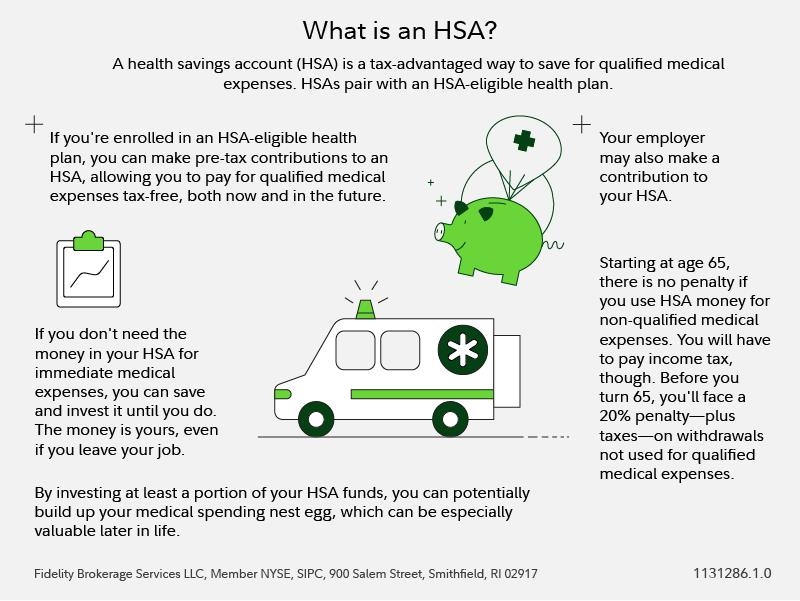

What Is an HSA?

A Health Savings Account (HSA) is a special type of savings account that helps you save for medical expenses if you are enrolled in a High-Deductible Health Plan (HDHP). As a tax-advantaged account, HSA funds are exempt from federal income tax. This means you pay no federal income tax when you contribute money to your HSA, when your HSA balance grows, or when you use HSA funds to pay for qualified out-of-pocket medical expenses (such as doctor visits, prescription medications, and other eligible costs).

It is a smart way to save for future health care needs while enjoying significant tax benefits. You can also earn interest or invest the funds, and any unused balance rolls over year after year, helping you build savings for future health care expenses.

(Source: Fidelity)

Why Do You Need a Health Savings Account (HSA)?

The appeal of a Health Savings Account (HSA) lies in its unique integration of health insurance, investing, savings, and tax savings—all in one. It not only helps you manage current medical expenses but also provides long-term support for your future health care and retirement needs.

The HSA’s most distinctive advantage is its rare “triple tax-free” benefit:

- Tax-free contributions: Funds you deposit into your HSA can be deducted from your taxable income (i.e., pre-tax contributions), directly reducing your taxable income for the year.

- Tax-free growth: If the funds in your account are invested (e.g., in stocks or mutual funds), any interest, dividends, or capital gains earned are exempt from federal income tax.

- Tax-free withdrawals for medical expenses: As long as the funds are used for qualified medical expenses, both principal and investment earnings can be withdrawn tax-free.

This combination of “tax-free contributions + tax-free growth + tax-free withdrawals for medical purposes” gives the HSA the core advantages of both a Traditional IRA and a Roth IRA—making it one of the most tax-efficient savings tools in the U.S. tax code.

(Source: Shutterstock)

Unlike Flexible Spending Accounts (FSAs), which follow a “use-it-or-lose-it” rule, HSA funds never expire. They can accumulate year after year and be held long-term. Even if you change jobs, retire, or emigrate, the account remains fully yours and is completely portable. Additionally, you can use your HSA to pay for qualified medical expenses for your spouse or dependents—even if they are not covered under your High-Deductible Health Plan (HDHP).

Although the HSA was originally designed to help HDHP enrollees manage medical costs, it can easily evolve into a powerful retirement savings vehicle. After age 65, you may use HSA funds for any purpose (not limited to medical expenses), subject only to ordinary income tax—consistent with the rules for a Traditional IRA. This means that if you pay your current medical bills with other funds and allow your HSA balance to grow through investments, that money could become a substantial “tax-free medical reserve” or “tax-deferred retirement income” decades later.

AGE | MEDICAL WITHDRAWALS | NON-MEDICAL WITHDRAWALS |

<65 | Tax-free | 20% penalty + income tax |

≥65 | Tax-free | Income tax only (like Traditional IRA) |

How to Think About HSA Asset Allocation?

Many investors treat their Health Savings Account (HSA) merely as a checking account for medical emergency funds—this significantly underestimates its long-term value.

If you plan to use your HSA funds for health care expenses in retirement—or even as supplemental retirement income—it should be strategically integrated into your overall retirement investment portfolio, just like a 401(k) or IRA.

Your HSA investment strategy should align with your spending timeline:

Still many years away from retirement or major medical expenses? Your account can afford to take on more risk, and your allocation should lean toward growth-oriented assets like stocks to maximize long-term compounding.

Approaching retirement or already have specific medical expenses planned? You should gradually reduce volatility by shifting a portion of your assets into cash or bonds to ensure a stable source for near-term spending.

Just as in traditional retirement planning with the “bucket” strategy, the HSA can adopt a similar approach:

- Bucket 1 (1–2 years of expenses): Keep in the HSA’s savings or money market account to cover near-term medical costs.

- Bucket 2 (3–10 years of expenses): Allocate to intermediate-term bonds or bond funds to balance return and stability.

- Bucket 3 (10+ years): Invest in stock index funds (e.g., VTI) or diversified equity assets to pursue long-term growth.

How Much Could Your HSA Grow?

The IRS establishes yearly HSA contribution limits, which are periodically updated to reflect inflation adjustments. In 2025, the limits are:

- Individual HDHP coverage: $4,300

- Family HDHP coverage: $8,550

- Catch-up contribution (age 55+): +$1,000

Note that these are combined contribution limits—meaning the total contributions from both you and your employer cannot exceed the limit. For example, if you have individual coverage and your employer has already contributed $1,000 to your HSA, you can contribute at most $3,300 yourself for the year.

Assume you start at age 35, contribute the full family limit annually ($8,550), and invest the funds in a portfolio with an average annual return of 7%. By age 65—when you enroll in Medicare—your account balance would exceed $283,000. If used for qualified medical expenses, this amount can be withdrawn entirely tax-free—equivalent to an invisible, tax-advantaged medical pension.

What Happens After You’re Gone?

The HSA’s triple tax-free advantage does not automatically continue after the account holder’s death.

If the beneficiary is a spouse, the account can continue to be used as an HSA, with all tax benefits intact. However, if the beneficiary is a child or any other non-spouse individual, the account terminates immediately, and the entire balance must be reported as ordinary income and taxed in full in the year of death.

In other words, if you and your spouse remain healthy throughout your lives and never use the HSA funds, this wealth—originally eligible for tax-free use—could ultimately “shrink” by nearly one-third due to inheritance rules, depending on the beneficiary’s tax rate.